April was a good month for cotton prices. So far, May has not been. Prices do seem to be attempting somewhat of a recovery, however. Both old crop July futures and new crop December futures have bounced back to recover about half of the decline we’ve experienced so far this month. Both old crop and new crop currently stand in the neighborhood of 62 cents.

April was a good month for cotton prices. So far, May has not been. Prices do seem to be attempting somewhat of a recovery, however. Both old crop July futures and new crop December futures have bounced back to recover about half of the decline we’ve experienced so far this month. Both old crop and new crop currently stand in the neighborhood of 62 cents.

Prices gained 546 points (July futures) and 495 points (Dec futures) respectively for the month of April. Both July and Dec futures reached a May low of around 60 ½ cents, but have since bounced back to around 62 cents or better.

Marketing is all about picking your opportunities, or sometimes picking your poison. It appears that new crop December has perhaps established a floor at 60 cents with further support likely at 58. December looks to have resistance at 63 to 66 cents. We’ve already hit our head at 63 to 64 cents once. July also looks capped at 64 cents.

Marketing is all about picking your opportunities, or sometimes picking your poison. It appears that new crop December has perhaps established a floor at 60 cents with further support likely at 58. December looks to have resistance at 63 to 66 cents. We’ve already hit our head at 63 to 64 cents once. July also looks capped at 64 cents.

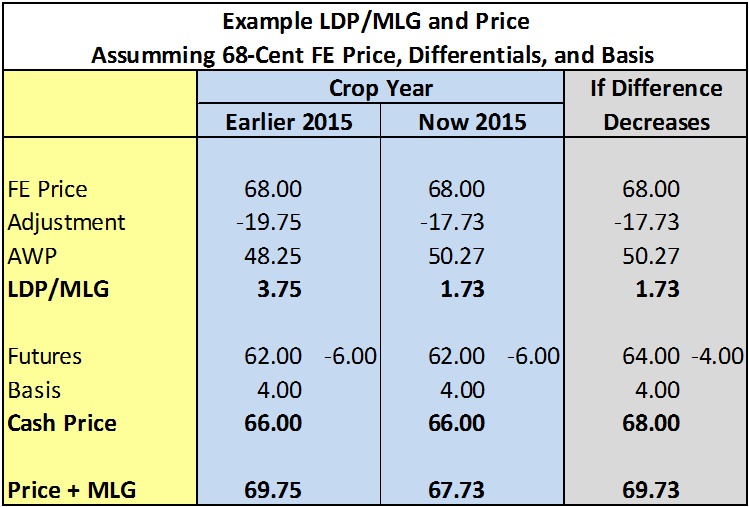

If you have old crop still in Loan, you can redeem some of that cotton, or take a merchant equity on rallies during the week while the MLG is fixed. That’s the way you have to play the game.

Unfortunately, the recent 2 cent reduction in the AWP transportation cost adjustment makes any MLG 2 cents lower than what it otherwise would be. In the grand scheme of things, some or all of this can be made up, if US cotton prices (nearby futures) increase/gain in relation to the A-Index (FE Price) and/or if Basis improves. This applies to the remaining 2015 crop and the upcoming 2016 crop. If the demand for US cotton, relative to other cotton improves, or if for any reason, the difference between the FE Price and US price narrows, or if the Basis improves, this could offset the current loss in LDP/MLG and reduction in total money received.

Moving forward, factors impacting prices will include crop conditions, and changes in US and foreign production estimates, US exports, the amount/pace of Chinese reserve sales, and World mill use.

Moving forward, factors impacting prices will include crop conditions, and changes in US and foreign production estimates, US exports, the amount/pace of Chinese reserve sales, and World mill use.

USDA’s May supply/demand and production estimates released last week contained monthly revisions of estimates for the 2015 crop, and the first projections for the 2016 crop. By now, you have likely seen the numbers so we will not plow that ground again. There are several observations worth noting, however, and let’s stick these under our hat for later reference:

- The 2016 US crop is projected to be 14.8 million bales. It won’t be. This first estimate is always based on expected acres to be planted, average yields and acreage abandonment with an adjustment based on present moisture conditions in the Southwest. Actual plantings and growing conditions will adjust this as we progress through the season. With good demand for high quality cotton, the market could go higher if crop prospects decline.

- US exports for the 2015 crop year were revised down from 9.5 to 9 million bales. 2016 crop year US exports are forecast at 10.5 million bales. This actually seems like a good level of exports, given reserve sales and a second year of reduced imports allowed by China. This forecast likely reflects larger available supply in 2016/17 and seems to suggest that exports to other countries will offset some of the reduction to China.

- US ending stocks are expected to increase; foreign and total World stocks are expected to decrease. US stocks are going in the wrong direction (increasing) while World stocks are going in the right direction (shrinking).

- World mill use is expected to increase, although slightly—1.75 million bales or 1.6%. Largest increases are expected in China, Vietnam, Bangladesh, and Pakistan. I am reminded that the 2015 crop World demand was once projected at over 115 million bales. The current estimate is barely 109 million bales. Keep an eye on the trend in these estimates as we progress through the season. Is demand strengthening or weakening?

- For the 2016 crop year, China’s cotton production is forecast down 1.3 million bales from last season. Production is expected up in the US, India, Turkey, and Pakistan. Production is expected down in China and Brazil.

- China’s stocks are expected to decline 6.6 million bales. Overall, World stocks are expected to decline by 6.36 million bales by the end of the 2016 crop year. If realized, China’s stocks will have declined 16½% since the beginning of the 2015 crop year. While still a massive amount and while the process is proving painful, stocks are moving in the right direction.

In last week’s USDA’s May supply/demand report, a little bit of information may have gone unnoticed. The expected US average price for the 2016 crop is projected to be 47 to 67 cents per lb. If we take the midpoint at 57, that would be roughly the same as for last year’s crop. It also tells us there is a supply/demand scenario that could take us much lower than where this market is now; but likewise a scenario that could lead to better prices.

In last week’s USDA’s May supply/demand report, a little bit of information may have gone unnoticed. The expected US average price for the 2016 crop is projected to be 47 to 67 cents per lb. If we take the midpoint at 57, that would be roughly the same as for last year’s crop. It also tells us there is a supply/demand scenario that could take us much lower than where this market is now; but likewise a scenario that could lead to better prices.

Prices for remaining 2015 crop year and for the 2016 crop will be affected by China’s government reserve sales. On May 3, China began sales from its government reserves. This series of sales will continue through August with total sales not to exceed 9.2 million bales. Daily sales are not to exceed 138,000 bales.

For the period May 3 through May 12, sales totaled roughly 1.1 million bales or 12 percent of the 9.2 million bale total for May 3 through August 31. These 1.1 million bales sold were 770,000 bales of imported cotton and 334,000 bales of China cotton.

Sales from government reserves are believed to be for China’s domestic mill use only. Exports are not expected, but cannot be ruled out. China has said that from September through February, it plans to purchase/import cotton for the purpose of improving the fiber quality of its reserve.

Thus far, the cotton market seems to have taken the sales pretty much in stride; but, it’s too early to yet know how prices will play out. China’s reserve sales are only one factor in the mix of things that will determine how prices fare in 2016 and for the 2017 crop as well.

With regard to China and these sales, several factors are worth watching. Will the pace of sales remain steady and near the daily and weekly allowable amounts, or will sales diminish over time? This will, in part, depend on the quality of the available cotton and the pricing. If quality is an issue, it will show up and sales will lag behind. This may improve the outlook for US exports. Will the quality and competitive pricing of sales result in increased use of cotton in Chinese mills? More importantly, if cotton use begins to improve, will that ultimately mean more US cotton exports? What will be the level of China’s stocks next year this time and even in 2018? The clock is ticking and these stocks are only getting older.

William Don Shurley, University of Georgia

229-386-3512 / donshur@uga.edu

demayo@ufl.edu - 850-482-9620

Follow me on Twitter

@UFCowman