Don Shurley, UGA Emeritus Cotton Economist

Don Shurley, UGA Emeritus Cotton Economist

Last week, I visited an “apple house” in north Georgia. On this day, there were 3 or 4 bus loads of kids there also—touring the orchards, petting animals, and eating all sorts of yummy stuff. In the store, you could buy apples by type already bagged for you, or you could select and mix the types and size you wanted. Also last week, USDA released its October crop production and supply and demand estimates. It’s kind of’ like the apples—you can pick and choose—you’ll find some numbers you may think are good and some you may think are not.

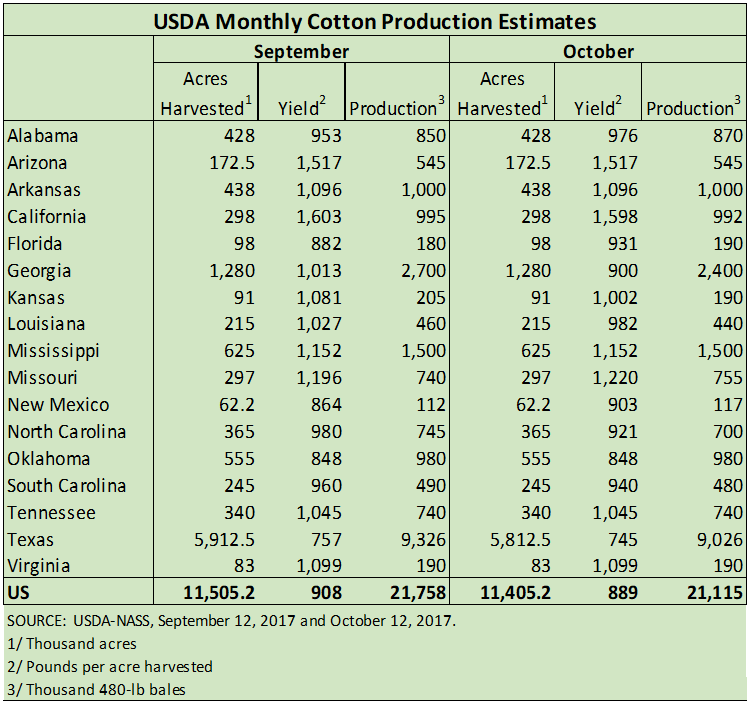

The October numbers were much anticipated because these were the first released by USDA to include the impacts of hurricanes Harvey and Irma. The September report pegged the crop at 21.76 million bales—a number the market did not like and prices dropped. Last week’s latest estimates now puts the crop at 21.12 million bales—down 643,000 bales or 3% from the September estimate. Opinions are mixed, but I believe a 643,000 bale decline is probably on the light side of what many expected. Post-Harvey estimates of loss in Texas were 200,000 to 400,000 bales or more and estimates floating around Georgia were losses of 10 to 25% due to Irma. Of course, whatever the losses were are still unknown, and losses can be offset in part by improvements in the crop elsewhere. Of the 643,000 bale decrease, 300,000 of that was in Texas and another 300,000 in Georgia. Compared to the September numbers, the crop was reduced in 7 states and increased in 4 states. In addition to Texas and Georgia, decreases were made for California, Kansas, Louisiana, North Carolina, and South Carolina.

Of the 643,000 bale decrease, 300,000 of that was in Texas and another 300,000 in Georgia. Compared to the September numbers, the crop was reduced in 7 states and increased in 4 states. In addition to Texas and Georgia, decreases were made for California, Kansas, Louisiana, North Carolina, and South Carolina.

The Georgia yield was dropped from 1,013 lbs/acre to 900 lbs. This was the second consecutive month that yield has been revised downward for Georgia.

Acres to be harvested in Texas were reduced 100,000 acres, and average yield was reduced from 757 to 745 lbs/acre. There has been some talk of damaged and/or lost modules due to hurricane Harvey. That has certainly been the case and the discussion is whether or not the NASS survey data picked that up. Theoretically, survey respondents could have factored such losses into their yield estimate, but I’m told current thought is that is not likely the case. The final yield and impact on yield will have to be determined based on ginning data. I’m told that the harvested acres change came from updated FSA failed acres data. The acreage estimate should not have been affected by lost modules, since that cotton was harvested.

In summary, the crop is now 3% smaller than pre-Harvey and Irma. But the crop is still uncertain and we’ll continue to eye further reports. The Texas crop has been behind normal in development, but has closed the gap just a bit. As of October 15, the crop is 73% open compared to 80% average for that date—7 percentage point behind normal compared to 11 points behind normal as of Oct 8. The crop is 30% harvested compared to 22% average.

Elsewhere, looking at the October supply and demand estimates:

- US exports for the 2017 crop marketing year were lowered 400K bales—reflecting our smaller crop and higher projections for exports from India, Brazil, and Australia.

- Exports for India were raised 400K bales, Brazil 250K bales, and Australia 300K bales.

- World Use/demand was raised 260K bales. Use/demand continues to show improvement. If realized, this would be a 3.8% increase from last season, 6.1% higher than 2 years ago.

- Of this 260K bale increase in Use, 250K of it is accounted for by increase for Vietnam.

- China was unchanged from the September numbers.

The direction of prices is becoming a little concerning. There seems to be support in the 67 to 68 cent area. Prices (Dec futures) dropped on Thursday last week, following the report, but then recovered most of that on Friday. That’s was a good sign. But as shown here, the trend of lower highs over the past month or more could be a caution flag.

Given the present supply and demand factors as we know them, and the uncertainty of the US crop, a range of 67 to 71 cents seems likely in the near term.

Price direction will likely key on further/future reports on both the size and quality of the US crop (particularly the conditions and progress of the Texas Panhandle crop), the pace of export sales and shipments, and still some questions and uncertainties about foreign production.

A price range of 67 to 71 cents seems likely, but the aforementioned “trend of lower highs” is somewhat concerning. We’re still in a mostly sideways pattern, but if the US crop stays in the 21 million bale area or larger, that may add some downward pressure on prices—testing the support at 67. As long as the verdict is out about the US crop, 67 to 68 should hold.

—

—

—

demayo@ufl.edu - 850-482-9620

Follow me on Twitter

@UFCowman