Don Shurley, UGA Professor Emeritus of Cotton Economics

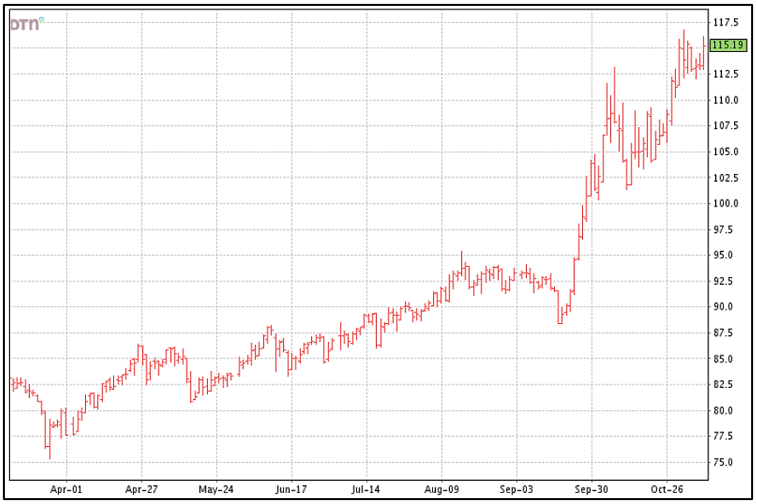

Today’s USDA reports were mostly neutral to either slightly bearish or slightly bullish depending on your viewpoint. Regardless, prices took off anyway. There are some factors in play that production and supply-demand don’t account for or fully explain.

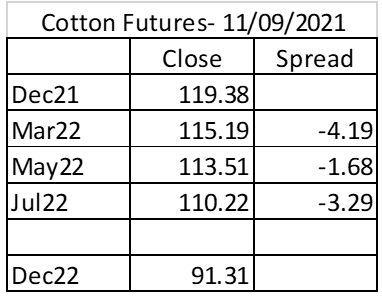

December 21 futures closed up 2.83 cents to $119.38. March 22 closed at $115.19. New crop December 22 closed at $91.32, up $0.47.

–

–

Buyer bids on recaps, if not already, are moving to basis the March futures. Notice that futures prices are currently “inverted” (the more distant month is at a discount to the nearer month) all the way out through the remainder of the 2021 crop marketing year.

Buyer bids on recaps, if not already, are moving to basis the March futures. Notice that futures prices are currently “inverted” (the more distant month is at a discount to the nearer month) all the way out through the remainder of the 2021 crop marketing year.

The implications of this are that prices will have to improve significantly and/or basis improve as well to make pricing later and/or storage a feasible option.

Basis and quality premiums have been very good for recaps. Basis on fixed forward contracts may not be as good. A producer wishing to price now to take advantage of the high market should recap or risk of the market going down until uncommitted production is in. This market appears to have limited downside risk.

Here’s a quick summary of today’s November USDA production and supply-demand numbers:

US crop raised 200,000 bales. Yield was raised from the October estimates in several states including GA, NC, TX, and VA.

US crop raised 200,000 bales. Yield was raised from the October estimates in several states including GA, NC, TX, and VA.- Projected US exports for the 2021 crop year were unchanged.

- World production was raised 1 ½ million bales

- World Use was raised 700,000 bales to 124.1 million bales. If realized, this would be the highest Use since 2006-2007

- World beginning stocks for the 2021 crop year were lowered 1 million bales, due to revisions from prior years. Projected ending stocks were lowered 200,000 bales.

Despite these numbers, there are some subtle cautionary tones:

- The increase in the US crop is a little surprising to some. Crop conditions have slipped in recent weeks. There is concern over cooler temps and crop progress. Harvest is quite a bit behind normal in AL, GA, LA, MS, SC, and VA.

- The increase in Use is accounted for by India, Pakistan, Bangladesh, and Vietnam. There is little to no corresponding increase in imports (potential exports from the US).

- China production, Use, and imports were unchanged from the October estimates.

The weekly export report will be out Friday this week. For the past 4 weeks, sales have averaged 285,600 bales per week; shipments 114,300 bales per week.

There are some concerns about demand weakening. USDA’s November numbers seem to refute that. A signal for growers to keep an eye on, in addition to the futures, is the basis offered. If growers are very active in selling, due to high prices and if buyers get flush with cotton, that may be reflected in lower futures or basis – but right now, growers and buyers are both very active.

–