Tired of renting and thinking about buying a house? Not sure where to start? Let’s talk about some of the first steps in the path to homeownership.

Many people don’t realize that making the decision to buy a home and the process to buy one isn’t a one-size-fits-all step. There are many emotions and considerations that go into it. Here are some of the first questions to consider.

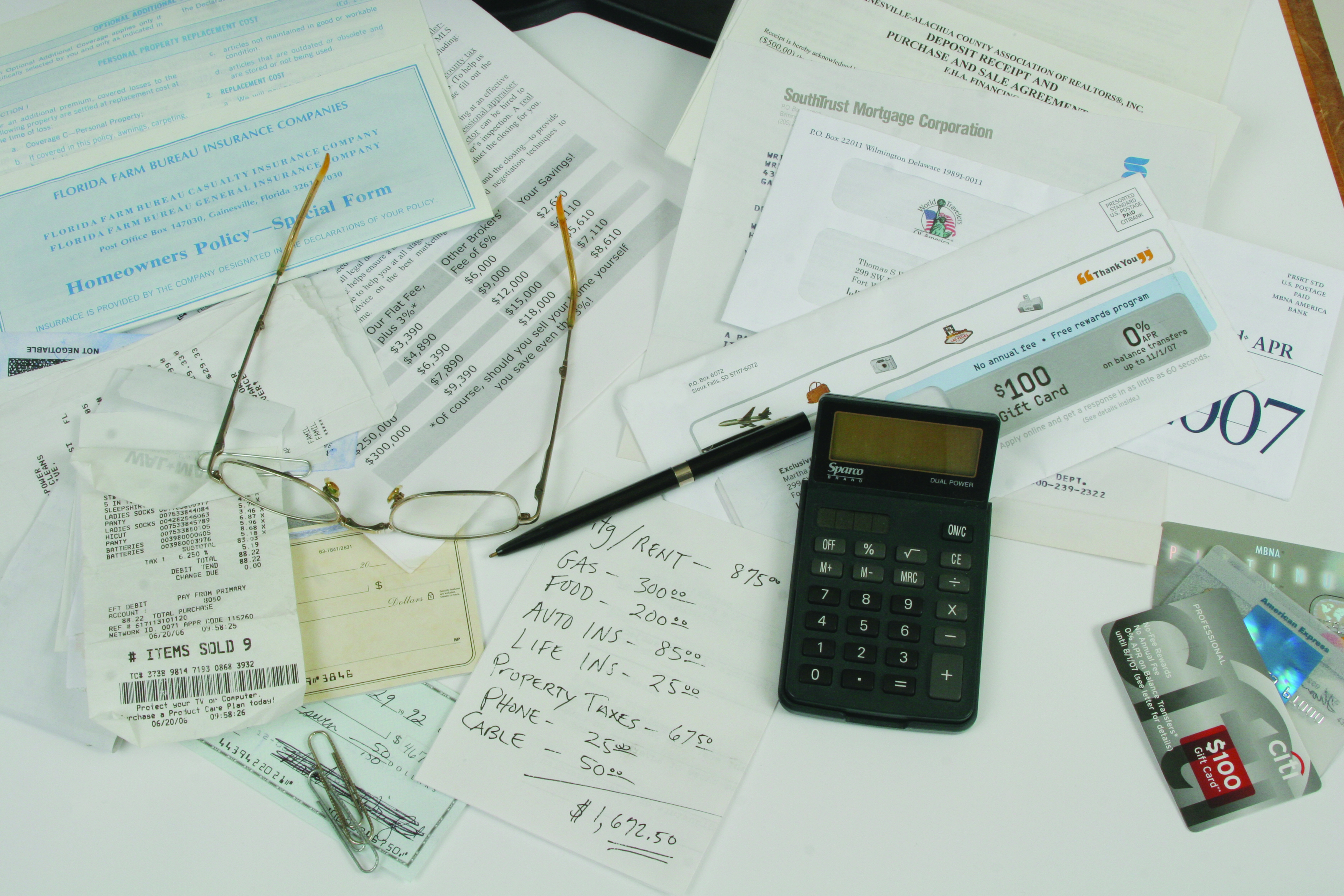

Do you have a budget or spending plan that you can live on?

Photo Credit: UF/IFAS Photo by Tyler Jones

Having a spending plan or budget that you can live on means that you’ve reviewed your income and expenses and either have a balanced budget or one with money left over. You may adjust that budget each month as expenses and/or income change but you don’t end the month in the negative. If you’re just getting started, try checking out our Money Management Calendar. It will take you through the six steps of building a spending plan and serve as a tool to help track your money each month. Knowing your financial situation before you begin the process to buy a home is important, as there are out-of-pocket costs that you’ll encounter when buying a home such as appraisal fees and closing costs, in addition to costs associated with homeownership, like maintenance, repairs, and insurance.

How does your credit report and credit score look?

Lenders use your credit score to help determine whether or not to approve you for a mortgage loan and, if approved, at what interest rate. The higher your credit score, typically, the lower your interest rate and the less you’ll pay for your home. Different loan programs may also have a minimum credit score requirement you’ll have to meet. Start by checking your credit report at the three different credit reporting agencies: Experian, Equifax, and TransUnion. Look for any errors or mistakes that could negatively impact your score. The three national credit reporting agencies permanently extended a program allowing individuals to check their credit report for FREE once a week at each agency. Visit AnnualCreditReport.com access the free copies of your credit reports. Improving your credit score can take time so starting early is helpful.

How much debt do you have?

Photo Credit: UF/IFAS Photo by Thomas Wright

Debt is another factor that lenders consider when you apply for a mortgage loan. Having too much debt can cause you to be turned down for a mortgage loan. The amount of debt you have can also significantly impact how much a lender is willing to lend you toward a home purchase. You can calculate your debt-to-income (DTI) ratio by dividing your total monthly debt payments by your total gross monthly income and multiplying it by 100 to convert it to a percentage. For total monthly debt payments, you should include any loans, credit card payments, child support, alimony, medical payments, and similar items. Do not include things like groceries, utilities, etc.

Each lender and loan program will have a different maximum limit, but many are in the range of 35-41% of your income going for debt repayment.

These are just a few of the initial questions to consider if you’re thinking about buying a home (and can be ones to think about even if you’re not!). Saving money, paying down debt, and repairing or raising your credit score all take time. Starting today can help you to be in a better position when you are ready to take the next step. If you want to learn more, UF/IFAS Extension offers classes for first-time homebuyers (returning buyers are welcome, too!) that go more in-depth for each of these questions and much more. Contact your local Extension office to find out about class schedules.

Resources:

My Florida Home Book: A Guide for First-Time Homebuyers in Florida, University of Florida/IFAS Extension

It won’t be long before you start to smell “holiday scents” and hear “holiday music” almost everywhere you go. These holiday smells and sounds are a marketing tactic. According to research conducted by Spangenberg, Gorhmann, and Sprott, when Christmas music is played in conjunction with an ambient Christmas scent being released, consumers have more favorable reactions to retailers, merchandise, and the overall shopping environment. Despite this retailing trick, consumers can avoid overspending by doing three things: make a budget, make a list, and stick to your plan.

Make a budget

Ideally, budgeting is something that is done in advance and practiced year round. If you already have a budget in place, simply begin to plan how you will spend the money you have set aside for this holiday by category. If you do not have a budget, make a decision about how much money you are willing to spend this holiday season and stick to it. Some categories you may want to include in your holiday budget: Christmas cards, postage/shipping, gift wrapping expenses, decorating, travel expenses, and items for special meals/potlucks. For a printable holiday budget template, click here or visit the University of Maryland Extension website at http://goo.gl/5957ic.

Make a list

Once you have an idea of how much money you have for each budget category, get specific. Under each category, list individuals/groups to whom you want to give cards or gifts, decorative items you wish to purchase, places you will travel to, and food items you may want to prepare that are outside of your normal grocery list. Once you have identified the specifics based on your budget, decide on the total amount you can spend on each item.

Stick to your plan

Stick to your list and do not buy things you cannot afford. The idea seems simple enough, but, ultimately, this is where some will fall short. In 2013, a study conducted by Harris Interactive found that 57% of U.S. adults with children said they would be willing to take on debt in order to make their children happy for the holidays. When you buy gifts on credit or receive refund anticipation loans, title loans, or cash advances, you are taking on debt and may be buying items you cannot afford. Items purchased on credit that cannot be paid off before interest accrues end up costing more.

Tricks are for Halloween. This holiday season, don’t get fooled into unplanned purchases by the ambient smells and sounds retailers use to entice consumers. Shop smart by making a budget, making a list, and sticking to your plan.

References:

Spangenberg, Grohmann and Sprott. (2004). It’s beginning to smell (and sound) a lot like Christmas the interactive effects of ambient scent and music in a retail setting. Journal of Business Research 58:2005 (1583-1589).

University of Maryland Extension (2013). Stop Seasonal Stress with a Holiday Spending Budget. Retrieved 31 October 2014 from http://goo.gl/5957ic

Lexington Law. (2014). With the Holiday Season Nearing, Lexington Law Examines How Important Presents Are and How Much People Spend on Them. Retrieved 31 October 2014 from http://goo.gl/i3KDXm

As you are clearing out clutter, sprucing up, and getting ready for summer, you also should start your financial spring cleaning by figuring out where you stand financially. Here are a few tips to help you get started:

1. Get organized.

Build a personal financial filing system; get out your financial paperwork and file it in order of importance. Separate bills – that way, you can track them as they come in, reducing the chance of missed or late payments.

Use a plastic tote for a filing cabinet – these keep your files dry and are easy to carry from one room to the next should you need to.

2.Create a budget.

How much money do you have? Are you spending more than you earn? If you don’t have a spending record, start one. You can still get on with your financial spring cleaning today. If you haven’t been keeping a record, just make a deliberate effort to start now. Try to note all your spending for the next month, right down to the candy bar. Then, in a month’s time, you’ll be able to see where your money is going and, hopefully, see some areas where you can cut back.

3. Pay off Debt

Now, let’s discuss what most people agonize over, but is a very important subject: debt. If you have any debt beyond a mortgage, you should try to focus on paying off this debt as quickly as possible. It’s also important to try to negotiate your interest rates down with your credit card company if you can. Although this option may not be available to everyone, especially if your credit is not good, it’s worth trying.

If you are not successful, you can use these steps to reduce debt:

Stop using credit; charging new items increases the balances on what you already owe.

Do not open new lines of credit.

Request a free copy of your credit report from www.annualcreditreport.com and honestly assess the problem. Understanding your situation helps when trying to resolve debt issues. Stop denying that you have a debt problem and work on it. You can analyze your debts using Powerpay®. This website gives you a personalized report and plan to reduce your debt based on your input.

Break your debt load into manageable chunks; define your goal and focus on reducing manageable amounts.

For more information on financial education and tools to help you get out of debt; contact your local county Family & Consumer Sciences Agent.