Tired of renting and thinking about buying a house? Not sure where to start? Let’s talk about some of the first steps in the path to homeownership.

Many people don’t realize that making the decision to buy a home and the process to buy one isn’t a one-size-fits-all step. There are many emotions and considerations that go into it. Here are some of the first questions to consider.

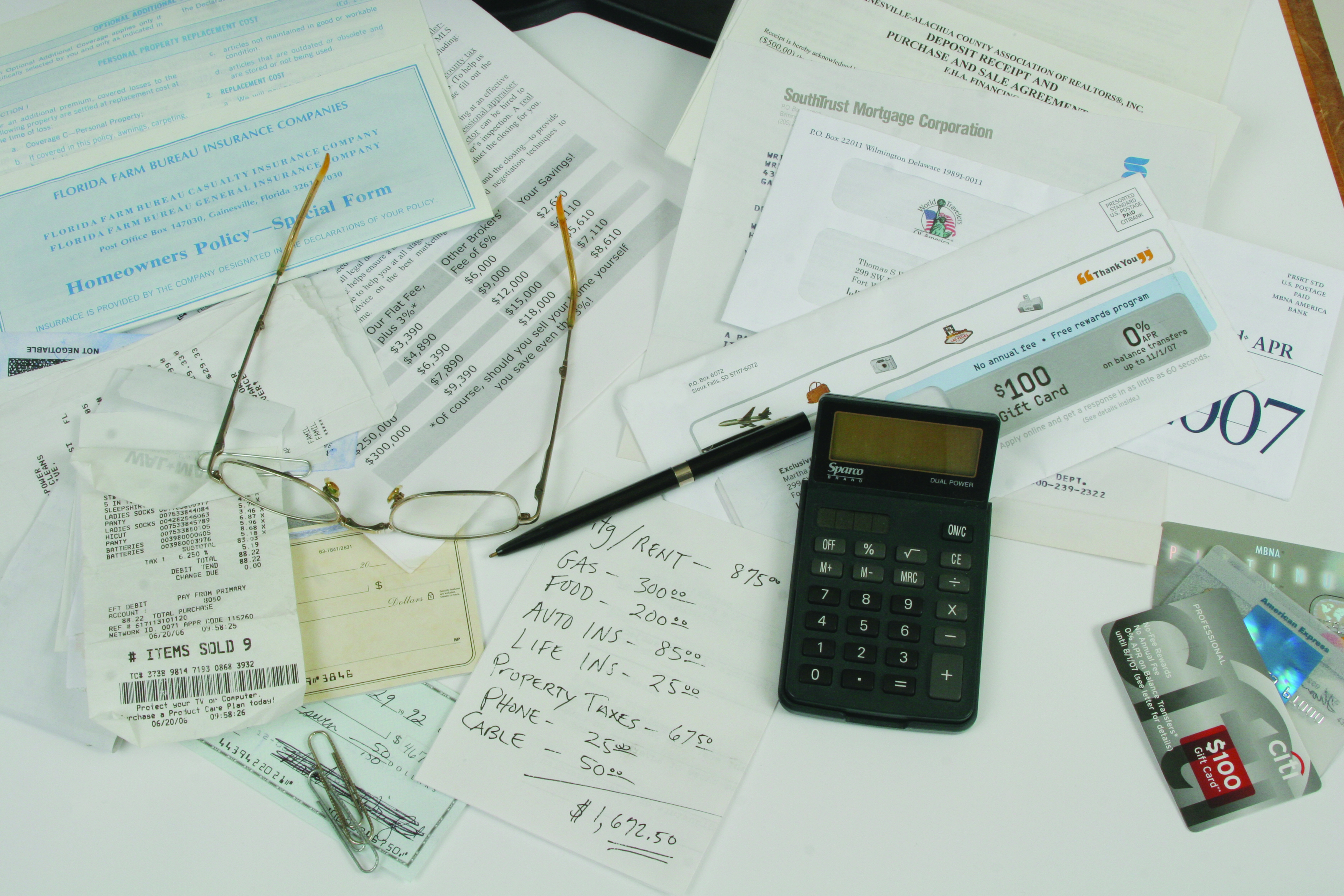

Do you have a budget or spending plan that you can live on?

Photo Credit: UF/IFAS Photo by Tyler Jones

Having a spending plan or budget that you can live on means that you’ve reviewed your income and expenses and either have a balanced budget or one with money left over. You may adjust that budget each month as expenses and/or income change but you don’t end the month in the negative. If you’re just getting started, try checking out our Money Management Calendar. It will take you through the six steps of building a spending plan and serve as a tool to help track your money each month. Knowing your financial situation before you begin the process to buy a home is important, as there are out-of-pocket costs that you’ll encounter when buying a home such as appraisal fees and closing costs, in addition to costs associated with homeownership, like maintenance, repairs, and insurance.

How does your credit report and credit score look?

Lenders use your credit score to help determine whether or not to approve you for a mortgage loan and, if approved, at what interest rate. The higher your credit score, typically, the lower your interest rate and the less you’ll pay for your home. Different loan programs may also have a minimum credit score requirement you’ll have to meet. Start by checking your credit report at the three different credit reporting agencies: Experian, Equifax, and TransUnion. Look for any errors or mistakes that could negatively impact your score. The three national credit reporting agencies permanently extended a program allowing individuals to check their credit report for FREE once a week at each agency. Visit AnnualCreditReport.com access the free copies of your credit reports. Improving your credit score can take time so starting early is helpful.

How much debt do you have?

Photo Credit: UF/IFAS Photo by Thomas Wright

Debt is another factor that lenders consider when you apply for a mortgage loan. Having too much debt can cause you to be turned down for a mortgage loan. The amount of debt you have can also significantly impact how much a lender is willing to lend you toward a home purchase. You can calculate your debt-to-income (DTI) ratio by dividing your total monthly debt payments by your total gross monthly income and multiplying it by 100 to convert it to a percentage. For total monthly debt payments, you should include any loans, credit card payments, child support, alimony, medical payments, and similar items. Do not include things like groceries, utilities, etc.

Each lender and loan program will have a different maximum limit, but many are in the range of 35-41% of your income going for debt repayment.

These are just a few of the initial questions to consider if you’re thinking about buying a home (and can be ones to think about even if you’re not!). Saving money, paying down debt, and repairing or raising your credit score all take time. Starting today can help you to be in a better position when you are ready to take the next step. If you want to learn more, UF/IFAS Extension offers classes for first-time homebuyers (returning buyers are welcome, too!) that go more in-depth for each of these questions and much more. Contact your local Extension office to find out about class schedules.

Resources:

My Florida Home Book: A Guide for First-Time Homebuyers in Florida, University of Florida/IFAS Extension

In 1795, Napoleon needed a better way to preserve large quantities of food for his troops during the Napoleonic Wars, so his government offered a reward of 12,000 francs for the invention of a new food preservation method. In 1809, Nicolas Appert won that award with his canning technique that used glass containers that were sealed then heated to a set temperature. Peter Durand created the tin canister a year later. These inventions led to the canning materials and processes that are used today to preserve food for people all over the world.

Canned food provides a convenient and often less expensive way to include fruits and vegetables in the diet of many individuals and families. Canned foods are also considered a staple in many pantries because of their shelf life. Commercially canned products may keep the food packed inside at its best quality for 1 to 5 years depending on the type of food. Most home canned foods are able to be stored for up to a year, though there are some exceptions.

Photo Credit: UF/IFAS Photo by Tyler Jones

To make the most of canned foods, keep these tips in mind.

Best by or use by dates on commercial products do not indicate safety. They are estimated dates provided by the manufacturer on how long they believe their product would be at its best quality. The exception to this is for infant formula products that are required to have a “Use-By” date and should not be used after that date.

Avoid cans or jars that are not in good condition. Look for dents, swelling or bulging, leaking, rust, cracks in jars or loose lids. If the food has a foul odor or spurts liquid when it’s opened, do not use it. Any of these could indicate the food may have been contaminated or could contain Clostridium botulinum toxins.

A woman canning in the kitchen. Photo Credits: UF/IFAS File Photo

Store canned foods in a cool, dark and dry space. This will help them to last longer and keep the food inside at its best quality. Keep canned foods in an area that is between 50-70°F.

Use canned foods to fill nutrition gaps. Add a can of vegetables to your dinner menu—a side of green beans or carrots can help balance your plate. Try using a can of fruit as a basis for a dessert. Pineapple and cottage cheese, anyone? If you’re concerned about sodium or sugar in canned foods, look for products marked as low sodium or lite for less sugar. Compare ingredient and nutrition labels of different brands or varieties of a product to find what works best for you.

Setting a New Year’s resolution is a tradition for many people. Unfortunately, breaking those resolutions also seems to be a tradition. If your New Year’s resolution is to eat healthier, here are some tips to help you to be successful.

Photo Credit: Terri Keith, UF/IFAS Extension

First, you will be more likely to follow through on your resolution by setting a SMART goal. A SMART goal is one that is Specific, Measurable, Achievable, Relevant and Timed. You can find more information on setting a SMART goal here.

Second, know that eating healthier doesn’t necessarily mean going on a diet or avoiding all the foods you enjoy. Eating healthier can start with making simple substitutions to your favorite recipes, like using whole wheat pasta instead of refined grain pasta, or swapping out sodas and energy drinks for water or other unsweetened beverages. It could mean that you make a conscious effort to enjoy the foods that aren’t as healthy for you in moderation or work on lowering the amount of sodium/salt that you eat. There are many ways to eat healthier and if you need more suggestions, you can check out this article on 5 things to avoid eating.

Whether you are starting with simple steps or looking for more in-depth information, ChooseMyPlate from the USDA can be a useful resource. There, you can find information on daily recommended values for the different food groups, what counts as a serving, along with other resources, like recipes or healthy eating on a budget. You might be surprised to find out what counts as a serving!

Third, try involving your kids or other members of your household in working together to eat healthier. There’s even a section at ChooseMyPlate that focuses on healthier eating for families. It can be harder to stick with your resolution if you are the only one working on it because your shopping list can end up including more sweetened snacks than fruits and vegetables. If you need some inspiration to get started, you can find a few videos of recipes that were adapted from ChooseMyPlate here.

Eating healthier is a terrific goal any time of the year. If this is your New Year’s resolution, follow these tips and stick with it!

Did you know that the Centers for Disease Control and Prevention (CDC) list hearing loss as the third most common chronic health condition in the U.S.? Many people do not recognize they have hearing loss, either because they do not realize it themselves or they won’t admit they have a problem. Statistics have shown that approximately 1 in 4 adults in the US between the ages of 20 and 69 who report having excellent hearing actually have measurable hearing damage.

Lower the volume on personal listening devices to protect your hearing. Photo source: Terri Keith

Most of us have heard that loud noises can damage our hearing, but do you know what is considered loud? Noises are measured in decibels (dB). Here are the measurements of some common sounds:

40 dB – Refrigerator hum

60 dB – Normal conversation

70 dB – Washing machine

80 dB – Traffic noise inside a car

80-85 dB – Gas-powered lawnmower

95 dB – Motorcycle

100 dB – Sporting event

105-110 dB – Maximum volume for personal listening devices

120 dB – Siren

140-150 dB – Firecrackers

Noises can start causing hearing damage at about 85 dB when experienced over an extended period of time. The higher the decibels, the less time it can take for hearing damage to occur. It may take about 2 hours for damage to occur at 90 dB but at 100 dB, it may only take 14 minutes. At 110 dB, hearing loss is possible in less than 2 minutes.

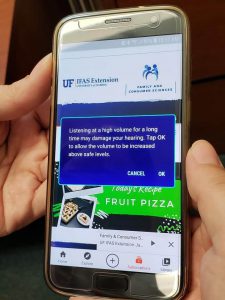

What can you do to protect your hearing? First, avoid noisy places when you can and keep the volume down when you’re watching TV or listening to music. If you can’t control the noise, try using ear plugs, protective earmuffs or noise canceling headphones. This is especially important if you’re going to be exposed to the noise over a period of time. If you’re not sure whether you should be worried about the noise level where you are, grab this smartphone app and check the decibels for yourself!

Remember that hearing loss from loud noises can be prevented. Once the damage occurs though, it’s permanent so take care of your hearing!

According to the Centers for Disease Control and Prevention (CDC), falls by older adults aged 65 and up can often result in serious injuries, decreased mobility and a loss of independence. They are common and can happen at a high cost, both financially and in terms of health and lifestyle for the person who falls. Statistics from the CDC show “each year, 3 million older people are treated in emergency departments for fall injuries” and the death rate from falls in the U.S. has been on the rise—30% from 2007 to 2016.

While many falls don’t cause injuries, some do and can leave the person with bruises, sprains, broken bones or head injuries. Even if a person falls without suffering an injury, that fall may lead to a fear of falling. Both the injuries and the fear of falling can lead a person to limit their daily activities. By being less active, the person increases their risk of falling again.

It’s not all bad news though. Many falls are preventable and several of the steps you can take for yourself or a loved one are low or no cost. Start by looking for risk factors. These are conditions that increase the chances of a fall happening. Here are some to be aware of:

Taking more than 2 medications daily.

Having a hearing and/or vision impairment.

Experiencing dizziness when getting up, changing positions, or walking.

Having trouble getting in and out of a chair, walking, picking up objects from the floor or reaching overhead without holding on to something.

Having throw rugs, cluttered walkways, uneven surfaces or slippery floors.

Navigating stairs without rails.

Having poor lighting conditions.

Wearing shoes with high heels or slippery soles.

Having fallen in the past year or being afraid of falling.

Many of these can be corrected or managed. One of the key steps to preventing falls is talking with your doctor and pharmacist. They can help with evaluating your risk and advise you on specific things you can do, especially in terms of problems with hearing, vision or medications. Staying active or following exercise routines can help with balance and strength. Here is a link to some beginner level exercises to start with if you’re not already exercising.

An elderly persons bathroom can be made safer by adding items that will help them maneuver easier. Photo Credit: UF/IFAS Marisol Amador

Do a check of your home to see if you have any of the risk factors above and correct them. Here are some other steps you can take at home:

Keeping a lamp beside the bed means you don’t have to walk through the dark at night to get to the light switch. Photo credit: Terri Keith, UF/IFAS Extension

Lower shelves 3 inches for easier access; adjust closet rods to keep clothes within reach.

Use a reacher or grabber for items that are too high. NEVER use a chair as a step stool.

Install or add more lighting in your home especially near walkways, stairs and entrances.

Keep a lamp and flashlight by your bed and night lights where needed.

Install or secure handrails on both sides of the stairs and use them every time.

Make sure walkways are clear and uncluttered. Remove or secure throw rugs, cords and hoses out of the way.

Use textured surfaces for patios, driveways and stairs. Mark any changes in floor level with reflective tape.

Be aware of your pet’s location when you stand or walk so they don’t trip you.

Install and use grab bars to help with getting in and out of the bath safely.

Use a rubber mat in your bathtub or shower.

Install a handheld showerhead and use it with a bath bench or chair when showering.

If a fall does happen, even if there were no injuries, it’s a good idea to let your doctor know about it the next time you see them. It can help alert them to new medical problems or a need to review your prescriptions. Taking these steps can help reduce the risk of a fall and stop the cycle of falling from being repeated.