by Heidi Copeland | Apr 30, 2019

The Consumer Financial Protection Bureau, (CFPB) has defined financial capacity as a the combination of attitude, knowledge, skills, and self-efficacy needed to make and exercise money management decisions that best fit the circumstances of one’s life, within an enabling environment that includes, but is not limited to, access to appropriate financial services.

Many of the attitudes, knowledge and skills needed to build financial capacity can be learned. People learn behavior through a variety of contexts. Children, in particular, learn through practices modeled by a parent or caregiver. In fact, research shows that parents and caregivers have the most influence on their children’s financial capability.

If you are like most parents, you probably recognize this—and you are interested in setting your kids on a good path toward financial well-being. However, many parents also say they do not always have time, tools, or personal confidence to start talking about money thinking their children will learn about it in school, later on, when they are old enough to understand.

This is most unfortunate. According to the Council for Economic Education 2018 Survey of the States, only 17 States require high school students to take a course in personal finance. So, if a parent isn’t teaching their children basic money/financial skills who is? Economical and financial literacy is a foundational element to achieving financial health and financial well-being. It is never too early (or too late) to start building this.

Talking to children about money, even in EARLY CHILDHOOD, helps children build the skills they need later in life. Early childhood education experts like to call this scaffolding. You are setting the framework…the support…the platform, encouraging financial capability milestones from early childhood into young adulthood. Children can learn the behaviors, knowledge, skills, and personal characteristics that support financial health and well-being.

Books can help start these critical early conversation. The CFPB has made it EASY! Parents can be their child’s first financial capability teacher! The University of Wisconsin-Extension Family Living Programs and the University of Wisconsin-Madison Center for Financial Security have selected books for the CFPB Money as you Grow Book Club. This program uses easy to read and understand children’s books to discuss money concepts. These books include many favorites:

- A Bargain for Frances, by Russell Hoban

- A Chair for My Mother, by Vera Williams

- Alexander, Who Used to Be Rich Last Sunday, by Judith Viorst

- Count on Pablo, by Barbara deRubertis

- Cuenta con Pablo, by Barbara deRubertis

- Curious George Saves His Pennies, by Margaret and H.AS. Rey

- Just Shopping With Mom, by Mercer Mayer

- Lemonade in Winter, by Emily Jenkins

- My Rows and Piles of Coins, by Tololwa M. Mollel

- Ox-Cart Man, by Donald Hall

- Sheep in a Shop, by Nancy Shaw

- The Berenstain Bears & Mama’s New Job, by Stan & Jan Berenstain

- The Berenstain Bears’ Trouble With Money by Stan and Jan Berenstain

- The Purse, by Kathy Caple

- The Rag Coat, by Lauren Mills

- Those Shoes, by Maribeth Boelts

- Tia Isa Wants a Car, by Meg Medina

- Tia Isa Quiere un Carro, by Meg Medina

Fortunately, many of the building blocks for good financial decision making – like self-regulation, patience, planning, and problem-solving – do not require a lot of financial know-how.

Reading books with children is a creative way to learn about the many sides of money management. Pick up a few of the titles at your local library and influence your children’s financial capability. Building good habits leads to a life of good financial health and well-being.

Example of key ideas from reading books:

| PLANNING |

How Children Show It |

| Making Decisions |

Can look at a few choices and select on what will bring the best results. |

| Setting Goals |

Can follow a multi–step plan. |

| Prioritizing |

Can prioritize choices when they want two or more things at once. |

| Solving problems

|

Can describe problems and come up with a few idea to make things better. |

| MONEY |

|

| Earning |

Can identify the different jobs people in the family and in the community do to earn money and keep it safe. |

| Spending |

Make spending choices with their own money – real or play. |

| Saving |

Keeps money in a safe place and keeps track of amount saved for future spending. |

| Sharing and borrowing |

Can explain the difference between lending and giving something away. |

| ME |

|

| Self-control |

Can talk about times when they were able to wait and how they were able to do it. |

| Follow-through |

Can identify who they can turn to for help reaching a goal, or what tools or tricks might help them stick with a plan. |

| Staying true to yourself |

Name one special thing they like about themselves and their loved ones. |

| Flexibility |

Can talk about a time when their plans did not turn out how they wanted and what they did instead. |

Resource: https://www.consumerfinance.gov/consumer-tools/money-as-you-grow/

by Kendra Hughson | Apr 10, 2019

Just like your home, finances need regular “cleaning” and maintenance. Plan time this spring to focus on financial tasks. A little time spent getting organized and reviewing your financial habits helps keep your financial goals on track.

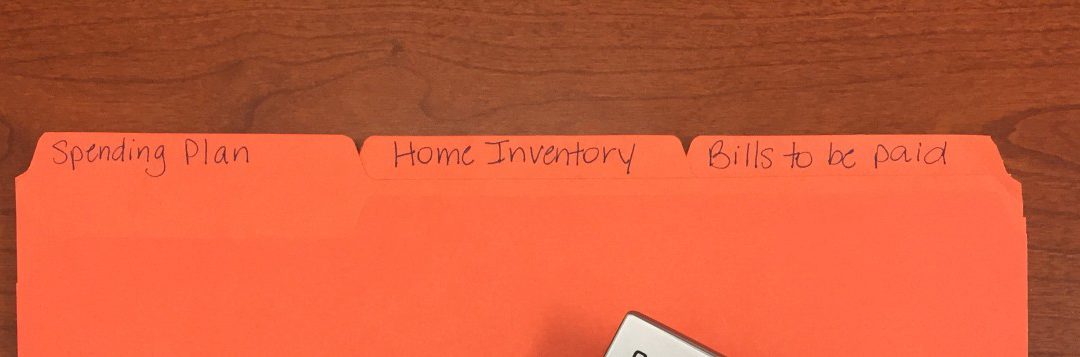

Spring clean your finances by getting organized. Photo Credit: Kendra Zamojski

Get Organized

A good spring cleaning starts with getting organized. Sort through important papers. Decide what you need to keep and what can be shredded or tossed. File your important papers. If you don’t have a home filing system, now is a great time to set one up. With an organized filing system, you can locate important documents quickly and easily when needed. Use UF/IFAS Extension’s Financial Recordkeeping resource to know what to keep and what to toss.

Track Your Spending

Update your spending plan by reviewing your financial goals. Check your financial progress by tracking your spending. Where is your money going? Is your money going toward your goals? Get the whole family involved in recording expenditures for a month. Track expenses by writing down every expenditure on a piece of paper. Alternatively, find a box and place all your receipts in it, being sure to include any money spent even if you didn’t receive a receipt. At the end of the month, review your spending record and look for places where you can cut back. UF/IFAS Extension’s Building a Spending Plan: All Six Steps is a great tool to create or update your spending plan.

Review Your Credit Report

A good credit history saves money through lower interest rates and makes it easier to get credit when needed. Annually, review your credit report from each of the three major credit bureaus. By law, consumers are entitled to one free copy of their credit report every 12 months from Equifax, Experian, and TransUnion. Get free copies of your credit reports at www.annualcreditreport.com. Consider rotating through the three bureaus every few months so you can check your credit report throughout the year. Review your credit report for errors and fraudulent activity. Also, review any negative information that could impact your credit and credit score.

Credit scores are based on the information contained in your credit report. You can obtain your credit score from www.myfico.com for a fee. Many credit card companies offer free FICO scores through their online billing websites. Companies like Credit Karma and Credit Sesame offer free credit score estimates but these sites also include advertisements for financial and other products. Check out UF/IFAS Extension’s You and Your Credit Series.

Make your finances a part of your springtime cleaning routine. A little time spent getting organized and reviewing your spending plan and credit reports will go a long way toward keeping you on track toward your financial goals.

by Judy Corbus | Mar 22, 2019

Unexpected expenses? Be prepared with a “rainy day” fund. Photo credit: UF/IFAS Northwest District

It began as a normal six-month dental check-up – no pain, no problems. After the X-rays, cleaning, and exam, my dentist informed me the X-ray showed an abscess above a back molar. The next thing I knew, I was headed to the endodontist for a root canal then back to my dentist for a permanent filling – wow! Who saw that coming? That was a classic “Life happens” moment!

We all face those unexpected events – a flat tire, a faulty alternator, an appliance on the fritz, a medical emergency. The question is, do we have the funds available to cover it? An emergency, or “rainy day,” fund helps us to handle those surprise expenses more easily, reducing our need to borrow to pay for them.

How much should we have in our emergency fund? A minimum of $1000 is a good starting point – that typically will cover most emergencies. A fully funded emergency reserve is three to six months of expenses; some financial advisors recommend eight to 12 months of expenses. If you are the sole breadwinner in your household, funding it to six months or beyond gives you a greater cushion. What is significant about these numbers? If you were unable to work due to a job loss, layoff/furlough, illness, or a family emergency, you would have funds available to tide you over until you could get back on your feet. Having funds to keep you afloat for a few months removes a lot of pressure and may allow you to explore your options without feeling like you need to take the first job offer that comes along because you “need the money.”

How do you fund your emergency fund? Look at your finances and, if you aren’t already in the habit of doing so, set aside a portion of your paycheck for savings right off the top – pay yourself first! Even if it’s just a few dollars per paycheck, those dollars will add up. If you receive a pay raise, save the difference between the new amount and your pre-raise salary. Your income tax refund is another great way to jump start your emergency fund – use Form 8888 Allocation of Refund to direct deposit your refund into one or more accounts.

It is a fact of life that life happens – be prepared with an emergency fund!

For more information on saving for emergencies, please see UF/IFAS FCS 7014 Money and Marriage: Saving for Future Use.

by Heidi Copeland | Feb 8, 2019

The Internal Revenue Service has announced that they began taking and processing tax returns beginning January 28, 2019 and refunds to taxpayers will be issued as scheduled.

Nevertheless, many software companies and tax professionals are accepting income tax return information now and promising instant refunds. KNOW that money being promised comes with a charge. As they say, there is NO free lunch, especially around tax time.

For taxpayers who usually file early in the year and have all of the needed documentation there is no need to wait to file. Taxpayers should file when they are ready to submit a complete and accurate tax return. The IRS strongly encourages people to file their tax returns electronically to minimize errors and for faster refunds.

The filing deadline to submit 2018 tax returns is Monday, April 15, 2019 for most taxpayers. Because of the Patriots’ Day holiday on April 15 in Maine and Massachusetts and the Emancipation Day holiday on April 16 in the District of Columbia, taxpayers who live in Maine or Massachusetts have until April 17, 2019 to file their returns.

Also, because of the change required by Congress in the Protecting Americans from Tax Hikes (PATH) Act, the IRS is required to hold refunds claiming the Earned Income Tax Credit (EITC) and the Additional Child Tax Credit (ACTC) until February 15, 2018. The IRS wants taxpayers to be aware it will take several days for these refunds to be released and processed through financial institutions. Factoring in weekends and the President’s Day holiday, the IRS cautions that many affected taxpayers may not have actual access to their income tax refunds until the end of February 2019. The IRS must hold the entire refund — even the portion not associated with the EITC and ACTC.

It is amazing to know that the IRS issues more than 9 out of 10 refunds in less than 21 days. Choosing e-file and direct deposit for refunds remains the fastest and safest way to file an accurate income tax return and receive a refund. However, it is possible your tax return may require additional review and take longer. Where’s My Refund? has the most up to date information available about your refund. The tool is updated no more than once a day so you do not need to check more often.

Your refund should only be deposited directly into accounts that are in your own name; your spouse’s name or both if it is a joint account. No more than three electronic refunds can be deposited into a single financial account or pre-paid debit card. Taxpayers who exceed the limit will receive an IRS notice and a paper refund.

Whether you file electronically or on paper, direct deposit gives you safe access to your refund faster than a paper check.

IRS

Money

Adapted from: https://www.irs.gov/help/ita

by Laurie Osgood | Feb 6, 2019

Regular vehicle maintenance can help you avoid expensive repairs. Photo credit: UF/IFAS Northwest District

A car is one of the biggest investments we will make. With proper car maintenance, you can increase safety, improve performance, and save money in the long run. According to AAA, big improvements in powertrain technology, lubricant, and rust prevention have led to improvements in automobile reliability, longevity, and durability. With proper care, almost any car can make it well past the 100,000-mile mark.

TIPS FOR PROLONGING THE LIFE OF YOUR CAR

• Do some research and purchase a safe, reliable vehicle

• Stick to the recommended car maintenance schedule

• Buy high quality parts: engine oil, battery, tires, etc.

• Keep your car clean, inside and out

• Know what to look for if your car is beginning to show signs of trouble

WARNING SIGNS THAT YOUR CAR MAY BE HEADED FOR TROUBLE

You know your car, and, therefore, you are the best judge of when it’s acting differently. There are signs your car may exhibit that will warn you of a potential problem. It could be a light, a sound, or an unusual smell. Consumer Reports recommends at the first sign of trouble, you should take your car to a reliable mechanic.

WARNING LIGHTS

Lights that appear on your dashboard are connected to sensors that monitor everything your car does. If your car senses that something isn’t quite right, the computer will use these lights to tell you what it is. If any of these lights appear, your mechanic will be able to hook up your vehicle to a diagnostic scan tool to identify the trouble and find out exactly what’s prompting the light to turn on.

Pay attention to these warning lights, as they could indicate a problem with your vehicle:

• Check Engine

• Check Oil/Oil Level Low

• Oil Pressure Low

UNUSUAL SOUNDS

You know your car and the sounds it normally makes, but new or different sounds can be a sign of trouble. These sounds can be a clue to what’s going on under the hood. GEICO Insurance offers a list of these sounds and their possible causes.

Sounds and Possible Causes

- A sound like a coin rattling inside a tin can: Could be a loose lug nut inside the hub cap.

- Brakes squealing or grinding: Your brake pads or shoes might need to be replaced. Pads may be worn, and the sound is metal on metal.

- A snapping, popping, or clicking sound when you turn a corner: One or both of the constant velocity (CV) joints on your front axle could need to be replaced.

- A rhythmic squeak that speeds up as you accelerate: This could indicate a problem with the universal joints (U-joints) in the driveshaft.

- A howling, whining, or even “singing” sound: Bearings, which are small metal balls that help parts rotate smoothly, may not be properly working.

- A rhythmic clunking, tapping, or banging from under the hood: This could indicate a problem with valves, pistons, or connecting rods. Rough, bumpy motions could be caused by faulty spark plugs, clogged fuel lines, or a bad fuel filter.

- A squealing sound from under the hood at start-up or when accelerating: This sound could be caused by worn or loose accessory belts for the power steering pump, air conditioner compressor, alternator, or the serpentine belt.

FOUL SMELLS

Toxic gases such as carbon monoxide are contained in a car’s exhaust system. If you smell a foul or strong smell while inside your car, this may be a sign of a serious problem. You should have it checked by a mechanic as soon as possible. If oil or coolant is leaking, this may mean hazardous exhaust gases are entering the interior of your car.

The smell of rubber burning could be a signal that your car’s drive belts or accessory belts underneath the hood are damaged, worn, or loose. These belts will need to be replaced as soon as possible to prevent more problems.

SMOKE

Smoke can come from the front or back of your car. Smoke coming from beneath the car’s hood most likely means your engine is overheating, and you should bring it to a mechanic right away. The color of the smoke coming out of your exhaust pipe can give you a clue about what may be going on inside your engine.

Blue Smoke: This could mean oil is escaping from somewhere within the engine and is being burned along with the gasoline. If you see blue smoke, your mechanic should look for damaged or worn seals in the engine.

White Smoke: May mean antifreeze or water condensation may have mixed in with the gasoline. You should have it checked out as soon as possible.

Mechanics agree that preventive maintenance, including regular oil changes and belt replacement, can help to extend the life of your car. Car maintenance can be an inconvenience that requires time, planning, and effort. But, in the long run, the benefits of driving a safe car outweigh the cost and aggravation.

For more information on how to save money by properly maintaining your car, contact your local UF/IFAS Extension Office.

Sources:

AAA: https://magazine.northeast.aaa.com/daily/life/cars-trucks/benefits-maintaining-vehicle/

Consumer Reports: https://www.consumerreports.org/car-repair-maintenance/make-your-car-last-200-000-miles/

GEICO: https://www.geico.com/more/driving/auto/auto-care/car-noises/?utm_source=geico&utm_medium=email&utm_content=newsletter&utm_campaign=feb2018

by Dorothy C. Lee | Dec 3, 2018

Holiday Stress

Photo source: Dorothy Lee

Tis the Season Merry and Bright:

From Thanksgiving to New Year’s Eve there are greater incidences of stress and tension related headaches and migraines. Family stresses, long shopping lines, and unrealistic expectations are enough to trigger tension headaches even in people who are not headache prone. To avoid these aches and pains a strategic plan may be necessary.

Planning is crucial not only at the holidays but throughout the year. Having a plan and being organized makes everything easier and more manageable. The key is to start early and don’t wait until December. This is where Christmas in July becomes useful thinking.

The following are some tips to help avoid stress during the holiday season. Make a schedule that includes all tasks you have to complete, how long you think each task will take, and when each task needs to be completed. This is why Santa makes a list and checks it twice.

- Start shopping early to reduce time wasted in long lines with early-bird hour sales

- To avoid long period of times wrapping, shop in stores where gift wrap is free

- Shop on-line while drinking your coffee in your pajamas

- Track your purchases in a notebook or in note section of your cell phone

- Prioritize your social events and don’t spread yourself too thin

- Use your computer for online postal mailing to avoid lines at the post office

- Instead of mailing gifts, order gifts on-line, and have gifts directly sent to gift recipient

- Practice relaxation and stretching to reduce stress

- Establish a spending limit and stick to it

Be realistic about how much you can do as nobody likes a cranky Santa. By following these tips, you will be as jolly as old Saint Nick.

Enjoy the holiday season with family and friends as it is the greatest gift you can give yourself. And remember, laugher is the best medicine for stress!

Happy Holidays!