by Suzanne Holloway | Nov 21, 2025

Debt is money you owe to a person or business. While debt often carries a negative connotation, responsible borrowing and repayment can improve your credit history.

Debt & Credit

Debt becomes a problem when you can’t repay what you owe. Missed minimum payments, carrying high credit card balances, or skipping payments can all damage your credit. For more information about credit and credit history, you can read this previous blog.

Budgeting & Mindful Spending

Being thoughtful about spending and borrowing can help you avoid unnecessary debt and improve your financial well-being. Financial well-being means having control over your money and the ability to make choices that reflect your goals and values. It starts with planning, spending less than you earn, and setting aside savings each month, usually with the help of a budget.

Mindful spending is about making intentional choices, aligning your purchases with your personal goals instead of spending out of habit. This awareness can reveal habits that you may want to adjust to save more. Practicing mindful spending not only helps you spot areas to cut back but also reduces financial stress. When you have a plan and track your money, you gain more control, security, and peace of mind. To learn more about budgeting, click here.

Getting Out of Debt

© zimmytws / Adobe Stock

The first step to getting out of debt is creating a realistic budget. You might also look for ways to increase your income, such as finding a higher-paying job, taking on a side gig, or selling unused items. If you’re struggling to keep up, reach out to your creditors to discuss a new payment plan.

Debt Collection

A debt collector is an individual or company, like a collection agency or a law firm, that collects debts on behalf of others or for themselves after purchasing past-due accounts. If you’re contacted by a debt collector, speak with them at least once to gather information and confirm whether the debt is truly yours—but avoid sharing sensitive details unless you’re sure of their legitimacy, as scammers often pose as collectors. By law, debt collectors must tell you the exact amount you owe, the creditor’s name, how to obtain details about the original creditor, and what to do if you believe the debt isn’t yours.

Debt collectors have a limited time to sue you for unpaid debts—this “statute of limitations” starts after your first missed payment. Once expired, the debt becomes “time-barred,” and collectors can no longer sue or threaten to sue for payment. However, in some states, making a payment or acknowledging the debt can restart the statute of limitations, so proceed carefully.

If you would like a debt collector to stop contacting you immediately, send a letter by certified mail and ask for a return receipt. If a collector threatens you, hang up and report them to the Federal Trade Commission (FTC).

Debt Elimination Tools & Resources

A reputable credit counseling organization can help by offering expert advice on managing money and debts, developing a budget and a realistic debt repayment plan, and providing free educational materials and workshops. Most reputable counseling organizations are non-profits or universities, such as UF/IFAS Extension, that offer services in person, online, or by phone for little to no fee. Other available resources, such as mobile apps and online tools, include:

An Equal Opportunity Institution.

by Samantha Kennedy | Oct 24, 2025

Taking the time to identify and plug spending leaks can help reduce stress and improve overall financial health. (Photo source: Adobe Stock)

When it comes to managing money, most people focus on the big-ticket items: rent or mortgage, car payments, or student loans. But it is often the small, unnoticed expenses – known as spending leaks – that can really make a big impact on overall financial health. These leaks may seem harmless on their own, but over time, they can add up to hundreds or even thousands of dollars lost each year.

What Are Spending Leaks?

Spending leaks are recurring or impulsive purchases that do not add significant value to your life but slowly drain your budget. Think of them as the financial equivalent of a dripping faucet – barely noticeable at first, but potentially becoming a flood over time. Common culprits include daily coffee runs, unused subscriptions (magazines, streaming services, etc.), frequent takeout, ATM fees, and impulse buys.

Costly Coffee

One of the most cited examples of a spending leak is the daily coffee habit. Spending $6-8 a day on specialty drinks may not seem like much, but over a year, that could add up to nearly $3,000. Brewing coffee at home or switching to a more affordable option can plug this leak without sacrificing your morning ritual.

Surplus Subscriptions

Streaming services, fitness apps, cloud storage, and digital magazines: many people are subscribed to more services than they actually use. According to a survey by Variety magazine, Americans spend an average of $69 a month on subscriptions, and many of those subscribers often lose track of all they are paying for. The same thing goes for magazine subscriptions. It is so easy to let those build up. Reviewing subscriptions quarterly and canceling unused ones can free up significant cash.

Expensive Eats

Grabbing lunch at work or ordering dinner a few times a week might feel like a convenience, but it is a major leak. Preparing meals at home – even just a few more times a week than you currently do – can save hundreds of dollars a month. Even with the higher cost of groceries, meal prepping and planning ahead can make home cooking more manageable and cost-effective. Frequent use of meal delivery apps is also an easy way to spend more than necessary on meals.

Convenience Costs

Using out-of-network ATMs or paying for convenience fees when paying bills online can seem minor, but they add up. Opt for fee-free banking options whenever possible, and plan ahead to avoid unnecessary charges. Even small fees of $2–$5 per transaction can total over $100 annually. Overspending can also lead to expensive late fees, overlimit fees, and overdraft fees.

Bargain Buys

Retailers are masters at encouraging unnecessary purchases – whether it is a tempting display at checkout or a flash sale online. One way to combat this is by implementing a 24-hour rule: wait a day before making any non-essential purchase. This simple habit can help you avoid buyer’s remorse and keep your budget intact. Even if something seems like a bargain, it is still a waste of money if it is something you do not need.

Spending leaks are sneaky, but they are also fixable. By identifying and addressing these small, recurring expenses, you can take control of your finances without making drastic lifestyle changes. A few mindful adjustments can lead to big savings—and a healthier financial future.

For more information about this and other money management topics, please call your local Family & Consumer Sciences (FCS) agent. You can find your nearest Florida FCS agent here.

An Equal Opportunity Institution.

by Suzanne Holloway | Sep 5, 2025

Money management refers to the process of overseeing and planning all aspects of your finances, including budgeting, saving, and investing. Effective money management helps you understand your current financial situation, set goals for the future, and make informed decisions to support your financial and overall well-being.

What’s a Budget?

Many people view budgeting, or “living on a budget,” as restrictive, but in reality, it is simply a tool that summarizes your income and expenses over a set period—often a month—to help you prioritize spending and achieve your goals. To start, calculate your total income from paychecks and any other sources (for example, child support, gifts, or public assistance). Then, list all your fixed costs (e.g., rent, insurance, property taxes, and occasional fees) and flexible expenses (e.g., groceries, transportation, and entertainment). By managing your flexible expenses wisely, you can ensure you have enough to cover your fixed obligations and also make progress toward your financial goals. Subtract total expenses from your income. If the result is negative, you are spending more than you earn and may need to adjust your budget. At the start of each budgeting period, set your plan, and at the end, review your spending and adjust as needed for the next period.

Budgeting Strategies

A budget isn’t one-size-fits-all, because everyone’s income, expenses, and priorities are different. Budgets should be tailored to your unique situation, which is why there are various strategies to choose from. Some of the most common strategies include the 50/30/20, Pay Yourself First, Zero-based, and Envelope budgets.

The 50/30/20 method divides your income into three categories: 50% for needs like housing, insurance, and groceries—things you can’t do without; 30% for wants such as dining out, subscriptions, or vacations; and 20% for savings to support future goals like building an emergency fund, buying a home, or saving for retirement. Debt reduction, such as paying minimum and additional payments for loans and credits, is placed in both the needs and savings categories.

© Andrey Popov / Adobe Stock

Pay Yourself First sets savings as the first expense by setting aside a fixed amount or percentage of your income as soon as you are paid. Start by focusing on building your emergency fund until it covers three to six months of essential living expenses. Once that’s accomplished, you can direct savings toward other financial goals. Setting up separate accounts or vaults for each goal can make it easier to track your progress and stay organized.

Zero-Based Budget ensures that every dollar you earn is assigned a specific purpose—whether for expenses and savings—so that your income minus your expenses always equals zero.

Envelope Budget, sometimes called “cash stuffing,” involves dividing your funds into envelopes (physical or digital), each representing a spending category. When the money in an envelope runs out, you stop spending in that category until the next budgeting period.

Budgeting Tools & Resources

There are many budgeting resources available, including apps, online tools, and printable worksheets. While some are free, many charge a fee to use or require payment to unlock additional features such as detailed reports, automatic account syncing, or advanced goal-tracking tools. Popular free mobile applications include:

*basic version; paid premium features available

Common paid apps:

Some banks and credit unions also offer built-in budgeting tools—check if there are any fees. Free printable worksheets from organizations like the Federal Trade Commission’s budget worksheet and the UF/IFAS Extension Money Management Calendar are also available. Furthermore, some prefer to create their budgets or use templates in Google Sheets or Microsoft Excel.

Explore different tools and mobile application options. Consider your financial goals, resources, and preferred budgeting strategy before making a decision, especially if you are considering a paid service.

Additional Resources

50/30/20 Calculator (OPERS)

An Equal Opportunity Institution.

by Sharlee Whiddon | Feb 27, 2025

Managing debt effectively involves setting clear, achievable goals and creating a structured plan. A good approach is using the SMART framework—ensuring that your debt repayment strategy is Specific, Measurable, Achievable, Relevant, and Time-bound. Here’s how you can apply SMART strategies:

Be Specific! Define the exact amount of debt you want to pay off. Instead of a vague goal like “reduce debt,” specify “pay off $5,000 in credit card debt.” List Your debts! Break down which debts need to be paid first, whether they are credit cards, loans, or other liabilities.

Make it Measurable! Identify a way to track your progress. Regularly check how much debt you’ve repaid. For example, you could track your debt in monthly statements or use budgeting apps. Also, set milestones. Break your larger goal into smaller, measurable targets – for example, paying off $1,000 of a $5,000 debt each month.

Is it Achievable? Set a realistic repayment plan. Consider your current financial situation—how much you can afford to pay each month. Make sure your goal is within reach given your income and expenses. Consider interest rates and prioritize high-interest debts first, such as credit cards, to reduce the overall amount paid in interest over time.

How Relevant is this? The debt repayment should tie into your broader financial goals, whether it’s improving your credit score, saving for a down payment, or achieving financial independence. Understand why paying off your debt is important to you. Whether it’s peace of mind, improving your financial health, or reducing stress, make sure your goal is personally meaningful.

It’s got to be Time-bound! Assign a target date for paying off your debt. For example, “Pay off $5,000 by the end of 2025.” Check in monthly or quarterly to ensure you’re on track and adjust as needed. This will help you stay focused on meeting your deadline.

By following these SMART principles, you’ll have a clearer, actionable plan that can help you stay on track with your debt management.

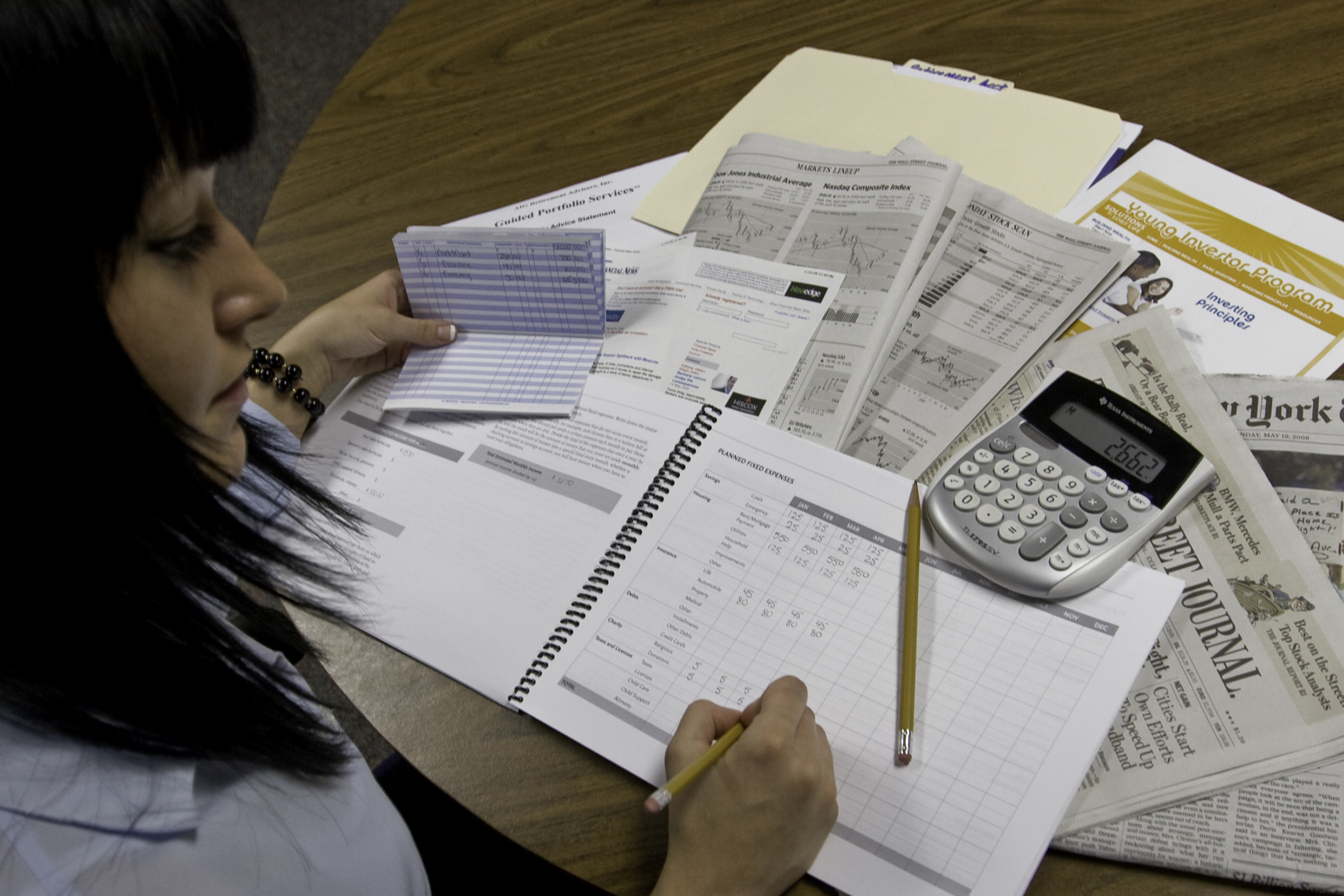

Using IFAS-generated budgeting tools, young people can learn to manage their money and begin saving and investing in the future. (UF/IFAS Photo: Tyler Jones. IFAS Extension calendar 2009)

Once you have taken the steps to build your SMART debt management plan, consider using the debt snowball or debt avalanche methods to aid in reaching your goal. These methods are popular strategies for debt repayment. Debt snowball involves paying off the smallest debt first, while Avalanche focuses on paying off the highest-interest debt first.

Find an accountability person that you can share your goal with and who will support you as you work to meet your goals. Planning regular check-ins with this person to monitor progress helps maintain positive energy and will lead to success.

It is a good idea to work on building a small emergency fund while paying off debt to avoid falling back into debt in case of unexpected expenses. Once you have eliminated your debt, grow your emergency fund even more.

It is important to celebrate your success of managing and erasing your debt. Just be sure the celebration doesn’t lead to finding yourself in debt again! A celebration might be a call to a friend or family member to share the great news or helping someone else use the SMART principles to set a goal they have.

For more information on managing your debt, contact your local UF IFAS County Extension Office.

Source: Forbes –The Ultimate Guide to S.M.A.R.T. Goals – Forbes Advisor

An Equal Opportunity Institution.

by Laurie Osgood | Apr 1, 2021

April is designated as National Financial Literacy Month to increase awareness about financial literacy, especially with the Coronavirus (COVID-19) causing economic worry for families across the United States. When it comes to financial literacy, knowledge is power!

April is designated as National Financial Literacy Month to increase awareness about financial literacy, especially with the Coronavirus (COVID-19) causing economic worry for families across the United States. When it comes to financial literacy, knowledge is power!

Consumer debt has become a major challenge for families. If you owe money to multiple creditors, managing this debt can be overwhelming. Many Americans have more debt than they can afford to pay. Developing strategies for overcoming this challenge is essential. These strategies should include building financial knowledge, developing a budget, and setting savings goals to improve your financial outlook.

Financial literacy means understanding how to save, borrow, invest, and care for your money, leading to greater financial well-being. Research has shown that our physical health and well-being are directly linked to our financial health and well-being.

Florida Saves is a statewide initiative that helps inspire Florida families to set savings goals, lower debt, and build personal wealth. The Florida Saves pledge, located on the Florida Saves website, can help us establish personal financial goals. With this pledge, you’re making a commitment to work toward a savings goal, such as college tuition, an emergency fund, or down payment on your first home. Visit the Florida Saves Initiative website to learn more about financial literacy.

Whatever your savings goals are, becoming financially literate can help you achieve those goals. For more information about financial literacy and management, please contact your local UF/IFAS Extension Agent.

Extension classes are open to everyone regardless of race, creed, color, religion, age, disability, sex, sexual orientation, marital status, national origin, political opinions, or affiliations.