by Ginny Hinton | Mar 24, 2016

Oliver Wendell Holmes, Jr. once said, “The greatest thing in the world is not so much where we are, but in which direction we are moving.” That saying holds true when it comes to our health and our finances.

Oliver Wendell Holmes, Jr. once said, “The greatest thing in the world is not so much where we are, but in which direction we are moving.” That saying holds true when it comes to our health and our finances.

Health and personal financial issues affect millions of Americans. We struggle with epidemic obesity rates, over 79 million Americans have “pre-diabetes”, debt and bankruptcy filings remain high and millions of Americans live on the “financial edge” with less than the recommended three months’ emergency fund set aside for the future. Problems that develop gradually soon become overwhelming.

Many of us, when faced with the need to change, see our problems as unbeatable and “freeze” instead of moving forward. It is true that there is no easy way to lose weight, gain wealth or become debt-free. Even drastic fixes like weight loss surgery or bankruptcy come with huge risks. So, what is the secret?

According to Former HHS Secretary Tommy G.Thompson, small steps are the key! Mr. Thompson stated, “Consumers don’t need to go to extremes – such as joining a gym or taking part in the latest diet plan – to make improvements to their health. But they do need to get active and eat healthier.” No step is too small to get started and you can never be too early or too late. Examples might include walking during your lunch break, cutting out 100 calories a day, saving the change you accumulate each day or tracking your spending for a month. Anything you do daily over a period of time will soon become a habit, or an “automated” behavior. When your healthy behaviors become automated – no matter how small – you’ve just taken a step toward physical and/or financial wellness.

In the end, your health is in your hands. Set realistic goals, take small steps to reach them, learn from the obstacles and believe that you can achieve. And remember, “In the end, the only people who fail are those who do not try.” – David Viscott

Adapted from Small Steps to Health and Wealth, B. O’Neill and K. Ensle, 2013.

by Kristin Jackson | Mar 17, 2015

Bindaas Madhavi. (2011) Listen to Your Kids.

Most parents would not allow their child to play in the street or to touch a hot stove because parents understand that these actions have consequences and the consequences are serious. If you don’t talk with your child about money and allow them to observe you exhibiting positive financial behaviors, this can also have serious consequences. One indicator of an individual’s financial capabilities is their credit score. A poor credit score can impact an individual’s ability to get a job, secure housing, purchase reliable transportation and access other forms of credit.

According to FINRA Investor Education Foundation State Financial Education Mandates, three years after Georgia, Idaho and Texas implemented a financial education mandate, credit scores of participants improved. In 2014, Florida also voted to adopt financial education into its social studies standards for students in grades K-12 and financial education is now a graduation requirement. While incorporating financial education into schools is an important step, parents still play an important role in financial socialization (establishing what is normal in terms of financial behaviors). In fact, research shows that time preference patterns and delay of gratification patterns are set by age five or before a child reaches kindergarten. Time preference patterns and delay of gratification patterns are often exhibited by adults through savings and budgeting. In a recent study by Cho, Gutter, Kim and Mauldin, the researchers found the effects of financial socialization had significant effect on the financial behaviors of low- to moderate-income adults aged 24-66, indicating that the time preference patterns children develop in youth could last a lifetime.

UF/IFAS Extension Northwest District Family & Consumer Sciences (FCS) Agents know that, as parents, you want to protect your child or children from things that have negative consequences whether it be an inattentive driver, a hot stove, or a poor credit score. One of the things parents can do immediately, to impact what their child is learning about money and how their child is being financially socialized, is to talk with their child about money. Some ideas to get your family conversations about money started are to discuss:

– Wants versus needs

– The grocery budget

– Household expenses

– How your child can earn/save money

If you are still a little nervous about starting the conversation as a result of concerns about your own financial capabilities, contact your local UF/IFAS Extension Office and ask about our Master Money Mentor Program or upcoming financial classes. If you can’t wait for a class, check out these additional resources:

Talking to Children about Money: http://www.ag.ndsu.edu/pubs/yf/famsci/fs1441.pdf

Are Your Children in the Middle of your Conflict or Divorce? http://goo.gl/lpXwwc

9 Important Communication Skills for Every Relationship http://edis.ifas.ufl.edu/pdffiles/FY/FY127700.pdf

Remember a family conversation about money is one conversation that is too important to wait. Make a money date with your child or children today!

References:

Cho, Gutter, Kim and Mauldin. (2012). The Effect of Socialization and Information Source on Financial Management Behaviors among Low-and Moderate-Income Adults. Family & Consumer Science Research Journal. 40(4): 417-430

Council for Economic Education. (2015). Survey of the States. Retrieved 16 March 2015 from http://www.councilforeconed.org/news-information/survey-of-the-states/

National Financial Educators Council. (2013) Financial Education Impact. Retrieved 16 March 2015 from http://www.financialeducatorscouncil.org/financial-literacy-statistics/

by Ricki McWilliams | Jan 27, 2015

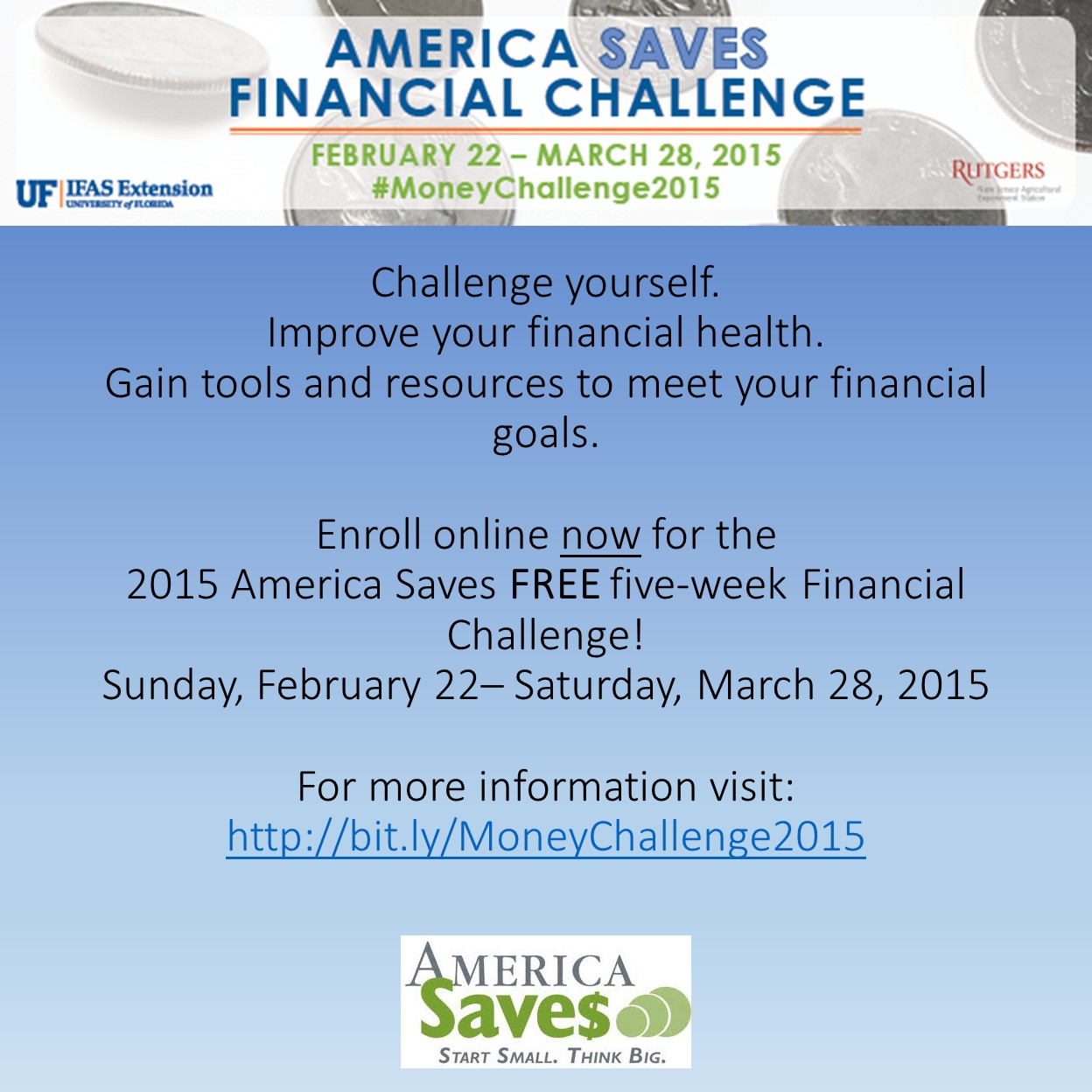

America Saves Week 2015 ~ February 23 – February 28

America Saves Week 2015 ~ February 23 – February 28

America Saves Week is coordinated by America Saves and the American Savings Education Council. Started in 2007, the Week is an annual opportunity for organizations to promote good savings behavior and for individuals to assess their own savings status. Typically, thousands of organizations participate in the Week, reaching millions of people. This campaign encourages individuals and families to save money and build personal wealth.

The 2014 Annual National Survey Assessing Household Savings (released during America Saves Week) revealed that while most Americans are meeting immediate financial needs, they are worse off than several years ago.

- Only about one-third of Americans feel prepared for their long-term financial future.

- 68 percent reported they are spending less than their income and saving the difference – down from 73 percent in 2010.

- Nearly two-thirds of respondents (64%) said they “have sufficient emergency savings to pay for unexpected expenses like car repairs or a doctor visit” – down from 71 percent in 2010.

- 76 percent said they are reducing their consumer debt or are consumer debt-free – down from 79 percent in 2010.

To learn more about America Saves Week and Pledge to Save, visit: www.AmericaSavesWeek.org

Set a Goal. Make a Plan. Save Automatically.

Get Involved! Events during America Saves Week include:

Ag Save$ Summit

February 23 – 9:00am CST/10:00am EST

Jackson County Extension Office, 2741 Pennsylvania Avenue, Marianna, FL 32448

(view registration link for additional locations)

FREE to register: bit.ly/AgSavesSummit

America Saves Financial Challenge – Online

February 22 – March 23

FREE to enroll: http://bit.ly/MoneyChallenge2015

Challenge Yourself to Save Money – America Saves Challenge Twitter Chat (#eXASchat)

February 24 – 2:00pm CST/3:00pm EST

Log in to Tchat.io at http://www.tchat.io/ and insert #eXASchat into the textbox that pops up so you can tweet easily and view the live Twitter stream

Where to Turn for Financial Advice – Webinar

February 25 – 11:00am CST/12:00pm EST

Free Registration: http://bit.ly/finpro2015

Personal Finance Questions – Realities & Myths – Webinar

February 26 – 11:00am CST/12:00pm EST

Free Registration: http://bit.ly/faq2015

by Elizabeth | Mar 31, 2014

As you are clearing out clutter, sprucing up, and getting ready for summer, you also should start your financial spring cleaning by figuring out where you stand financially. Here are a few tips to help you get started:

As you are clearing out clutter, sprucing up, and getting ready for summer, you also should start your financial spring cleaning by figuring out where you stand financially. Here are a few tips to help you get started:

1. Get organized.

Build a personal financial filing system; get out your financial paperwork and file it in order of importance. Separate bills – that way, you can track them as they come in, reducing the chance of missed or late payments.

Use a plastic tote for a filing cabinet – these keep your files dry and are easy to carry from one room to the next should you need to.

2. Create a budget.

How much money do you have? Are you spending more than you earn? If you don’t have a spending record, start one. You can still get on with your financial spring cleaning today. If you haven’t been keeping a record, just make a deliberate effort to start now. Try to note all your spending for the next month, right down to the candy bar. Then, in a month’s time, you’ll be able to see where your money is going and, hopefully, see some areas where you can cut back.

3. Pay off Debt

Now, let’s discuss what most people agonize over, but is a very important subject: debt. If you have any debt beyond a mortgage, you should try to focus on paying off this debt as quickly as possible. It’s also important to try to negotiate your interest rates down with your credit card company if you can. Although this option may not be available to everyone, especially if your credit is not good, it’s worth trying.

If you are not successful, you can use these steps to reduce debt:

- Stop using credit; charging new items increases the balances on what you already owe.

- Do not open new lines of credit.

- Request a free copy of your credit report from www.annualcreditreport.com and honestly assess the problem. Understanding your situation helps when trying to resolve debt issues. Stop denying that you have a debt problem and work on it. You can analyze your debts using Powerpay®. This website gives you a personalized report and plan to reduce your debt based on your input.

- Break your debt load into manageable chunks; define your goal and focus on reducing manageable amounts.

For more information on financial education and tools to help you get out of debt; contact your local county Family & Consumer Sciences Agent.

by Elaine Courtney | Sep 4, 2013

Credit card debt is something that hangs over many Americans. According to the Federal Reserve, in April 2013, the average credit card debt equaled $3,364 per U.S. adult. This assumes that EVERY adult has a credit card and that those cards carry debt. Of course, not all adults own a credit card. Young Americans are among those ditching their credit cards.

The only way to reduce credit card debt is to make payments each month and not add to that debt. The main way to reduce this even faster is to pay more than the minimum payment each month.

Save Nearly $4,000 by Paying More than the Minimum Balance

By only paying the minimum monthly balance, you are guaranteed to pay this debt for a longer time and pay more in total cost. For example:

|

Total Credit Card Debt

|

Monthly Payment

|

Years to Pay Off

|

Total Cost

|

|

$3,364 (at 14.96% Interest)

|

$67.28 (min. payment)

|

19 Years 5 Months

|

$7,618.63

|

|

$3,364 (at 14.96% Interest)

|

$87.28 (min. payment +$20)

|

4 Years 4 Months

|

$4,533.67

|

|

$3,364 (at 14.96% Interest)

|

$107.28 (minimum payment +$40)

|

3 Years 4 Months

|

$4,225.11

|

|

$3,364 (at 14.96% Interest)

|

$167.28 (minimum payment +$100)

|

1 Year 1 Month

|

$3,841.40

|

Similar information is available on your monthly credit card statement. It will identify how long it will take you to pay your debt if you only pay the minimum or if you pay a little extra. More info on how to read your bill is found at: http://www.federalreserve.gov/creditcard/flash/readingyourbill.pdf

You also can use an online calculator to determine costs and payoff information.

http://www.federalreserve.gov/creditcardcalculator/

Want to avoid the minimum payment trap completely? Follow these tips from financial experts:

- Know What You Owe – Make a list of all outstanding debt balances with the names of creditors, monthly payments, and APRs (interest rates).

- Run the Numbers – Use the Minimum Payment Calculator http://www.federalreserve.gov/creditcardcalculator/ and calculate the cost of making minimum and larger payments on various amounts of debt.

- Use a “power payment” to pay off your debt. Visit http://powerpay.org/

- Read the Numbers – Check your credit card statements about the cost of making minimum payments.

- Pay Cash – Instead of making new purchases with a credit card and adding them to outstanding balances, save up and pay cash (or use a debit card) to avoid interest charges.

- Set a Goal – To know how much to save, set a target date and dollar amount and work backwards. For example, $3,000 for a big screen television in a year requires weekly savings of about $58 ($3,000 ÷ 52).

In the example above, finding an extra $100 a month to apply to credit card payments reduces the time it will take you to pay off this debt from over 19 years to just over one year AND saves you nearly $4,000.

Need help finding ways to save? Take the Florida Saves pledge to make a commitment to yourself to save and to receive emails and/or text messages to keep you motivated.

Contact your local UF/IFAS County Extension office to find more ways and resources to help you manage your money. Be sure to join us for the Women & Money Program Oct. 1, 8, & 15!

Oliver Wendell Holmes, Jr. once said, “The greatest thing in the world is not so much where we are, but in which direction we are moving.” That saying holds true when it comes to our health and our finances.

Oliver Wendell Holmes, Jr. once said, “The greatest thing in the world is not so much where we are, but in which direction we are moving.” That saying holds true when it comes to our health and our finances.