by Judy Corbus | Feb 10, 2016

As W-2 forms and other receipts start rolling in, we’re reminded that tax season is upon us once again. It’s exciting to get back some of your own hard-earned money in the form of a tax refund! Saving a portion of your tax refund can be a big step toward meeting your savings goals, so it’s no surprise that a 2015 tax season survey found that a majority of those who receive a refund planned to save it.

This tax season, reward yourself for saving some of your refund by entering for a chance to win $25,000 through SaveYourRefund. SaveYourRefund has 101 cash prizes, including 100 weekly prizes of $100 and one grand prize of $25,000. Making smart financial decisions isn’t always easy, but splitting your refund couldn’t be simpler. Follow these quick and easy steps to enter to win in 2016:

- Use Form 8888 to split your refund. Entry to win with SaveYourRefund starts with splitting your refund into savings.

- Save $50 or more of your tax refund. In order to enter, use Form 8888 to save at least $50. There are a number of accounts you can save into including a savings account, a U.S. Treasury Direct account (savings bond), and a myRA retirement account.

- Visit SaveYourRefund.com to enter. You will automatically be eligible to win one of ten $100 prizes that will be given away every week from the start of the contest until the end of tax season.

- Upload a picture here that represents your savings goal or motivation, and you’ll be entered to win the $25,000 grand prize!

Need tax assistance? Take advantage of a Volunteer Income Tax Assistance (VITA) program. VITA programs offer free tax help to those who generally make $53,000 or less, persons with disabilities, the elderly, and limited English speakers.

Get ahead of your financial goals by splitting your tax refund into savings, and reward yourself with SaveYourRefund!

Source: Tammy Greynolds, AmericaSaves.org.

by Ricki McWilliams | Jan 27, 2015

America Saves Week 2015 ~ February 23 – February 28

America Saves Week 2015 ~ February 23 – February 28

America Saves Week is coordinated by America Saves and the American Savings Education Council. Started in 2007, the Week is an annual opportunity for organizations to promote good savings behavior and for individuals to assess their own savings status. Typically, thousands of organizations participate in the Week, reaching millions of people. This campaign encourages individuals and families to save money and build personal wealth.

The 2014 Annual National Survey Assessing Household Savings (released during America Saves Week) revealed that while most Americans are meeting immediate financial needs, they are worse off than several years ago.

- Only about one-third of Americans feel prepared for their long-term financial future.

- 68 percent reported they are spending less than their income and saving the difference – down from 73 percent in 2010.

- Nearly two-thirds of respondents (64%) said they “have sufficient emergency savings to pay for unexpected expenses like car repairs or a doctor visit” – down from 71 percent in 2010.

- 76 percent said they are reducing their consumer debt or are consumer debt-free – down from 79 percent in 2010.

To learn more about America Saves Week and Pledge to Save, visit: www.AmericaSavesWeek.org

Set a Goal. Make a Plan. Save Automatically.

Get Involved! Events during America Saves Week include:

Ag Save$ Summit

February 23 – 9:00am CST/10:00am EST

Jackson County Extension Office, 2741 Pennsylvania Avenue, Marianna, FL 32448

(view registration link for additional locations)

FREE to register: bit.ly/AgSavesSummit

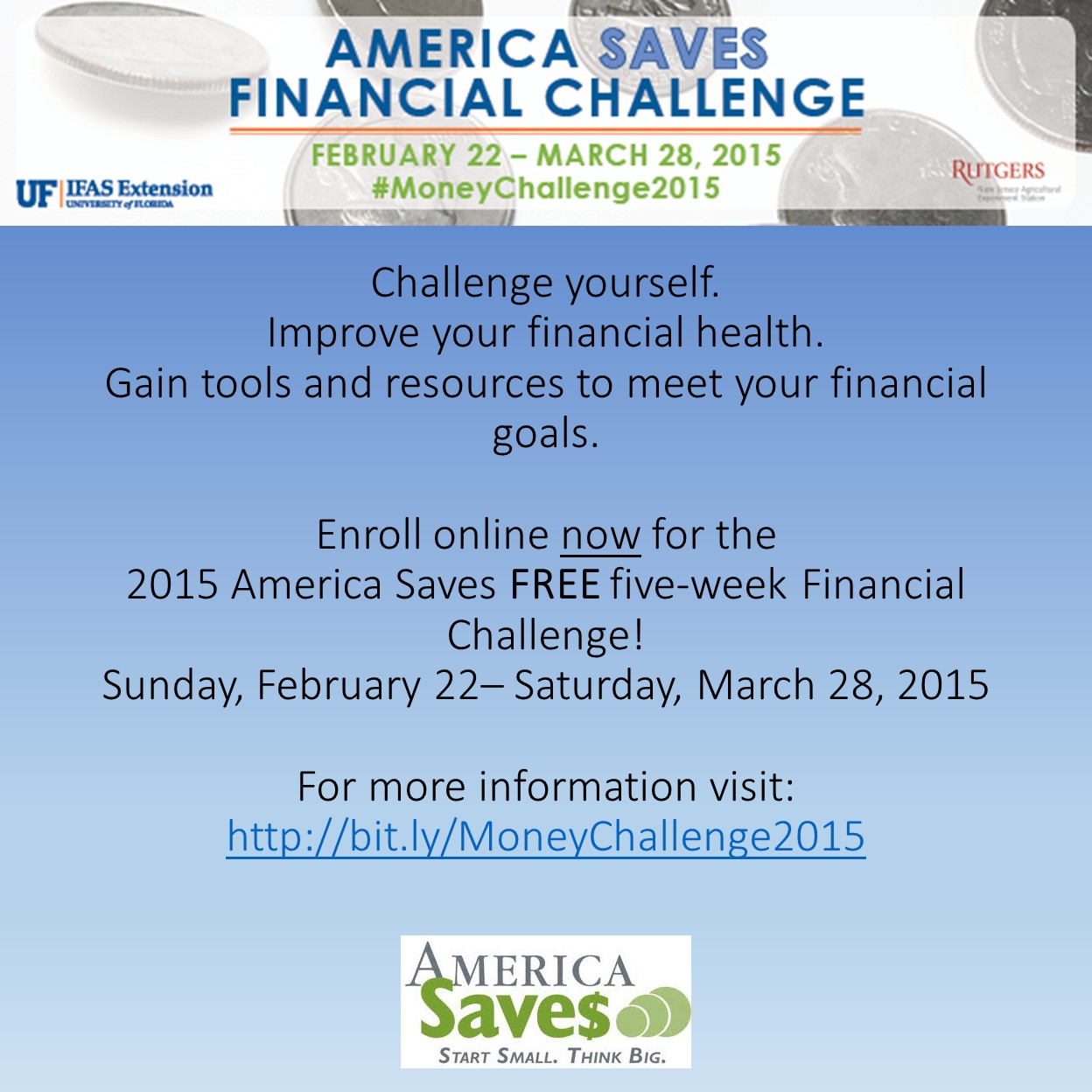

America Saves Financial Challenge – Online

February 22 – March 23

FREE to enroll: http://bit.ly/MoneyChallenge2015

Challenge Yourself to Save Money – America Saves Challenge Twitter Chat (#eXASchat)

February 24 – 2:00pm CST/3:00pm EST

Log in to Tchat.io at http://www.tchat.io/ and insert #eXASchat into the textbox that pops up so you can tweet easily and view the live Twitter stream

Where to Turn for Financial Advice – Webinar

February 25 – 11:00am CST/12:00pm EST

Free Registration: http://bit.ly/finpro2015

Personal Finance Questions – Realities & Myths – Webinar

February 26 – 11:00am CST/12:00pm EST

Free Registration: http://bit.ly/faq2015

by Kristin Jackson | Nov 22, 2014

When you go to the doctor for a physical your health care provider probably routinely records four important numbers as a base line indicator of your health. Your vital signs consist of your blood pressure, breaths per minute, pulse and temperature. There are important numbers when it comes to your financial health as well: your credit score, debt to income ratio and your savings rate.

When you go to the doctor for a physical your health care provider probably routinely records four important numbers as a base line indicator of your health. Your vital signs consist of your blood pressure, breaths per minute, pulse and temperature. There are important numbers when it comes to your financial health as well: your credit score, debt to income ratio and your savings rate.

Your Credit Score

Your credit score is used most frequently by lenders to evaluate the risk involved when loaning you money. With your consent, your credit score could also be used when considering you for employment, insurance or housing. The normal range for a credit score used by the Fair Isaac Corporation is 300-850, but the exact scoring method is determined by your lender. You can get a free copy of your credit report (the information by which your score is determined) if you are ever denied credit or by visiting https://www.annualcreditreport.com.

Your Income to Debt Ratio

Your debt to income ratio looks at the percentage of income that goes toward paying all recurring debt payments such as credit cards, car loans or even child support. You can calculate this ratio yourself by adding up all of your debts and dividing it by your income. The National Association of Credit Unions suggest that a debt ratio of 36% or less is ideal for most people.

Savings Rate

Your savings rate is the amount of personal income expressed as a percentage that you save. Your savings rate is another figure you can calculate yourself (Total dollars saved per month / total disposable income = savings rate). In, “How Much Should We Spend,” UF IFAS Extension publication FCS5229 the recommended savings rate for your general savings, your emergency fund and miscellaneous expenses is 2-20% of your income.

If you knew your numbers and they are above par then give yourself a pat on the back if you need more information that is no problem either. Contact your UF/IFAS Extension Family Consumer Science Agent (FCS) can meet with you or your small group and explain to you in more detail what each of these numbers are, where to find these numbers and provide you with the resources you need to know where you stand. You wouldn’t ignore your vital stats, so don’t neglect financial stats either. For more information contact your UF IFAS Extension office by visiting http://solutionsforyourlife.ufl.edu/map/ or contact UF IFAS Jefferson County Extension Agent, Kristin Jackson at 850-342-0187 or jefferson@ifas.ufl.edu.

Resources:

National Institutes of Health. (2014). Vital signs Retrieve 27 August from http://www.nlm.nih.gov/medlineplus/ency/article/002341.htm

Turnner, J. (2006). How Much Should I Spend? Retrieved 27 August from http://goo.gl/d29h5r

Credit Union National Association Inc.(2014). Debt to Income Ratio. Retrieved 27 August from http://hffo.cuna.org/12433/article/316/html

by Kristin Jackson | Feb 28, 2014

Normal

0

false

false

false

EN-US

X-NONE

X-NONE

/* Style Definitions */

table.MsoNormalTable

{mso-style-name:”Table Normal”;

mso-tstyle-rowband-size:0;

mso-tstyle-colband-size:0;

mso-style-noshow:yes;

mso-style-priority:99;

mso-style-parent:””;

mso-padding-alt:0in 5.4pt 0in 5.4pt;

mso-para-margin-top:0in;

mso-para-margin-right:0in;

mso-para-margin-bottom:8.0pt;

mso-para-margin-left:0in;

line-height:107%;

mso-pagination:widow-orphan;

font-size:11.0pt;

font-family:”Calibri”,”sans-serif”;

mso-ascii-font-family:Calibri;

mso-ascii-theme-font:minor-latin;

mso-hansi-font-family:Calibri;

mso-hansi-theme-font:minor-latin;}

Are you “liquid asset poor?” If a household experiences an unexpected financial strain, such as a job loss, illness, or other large expense, and does not have enough liquid assets to cover basic expenses for three months, they are considered liquid asset poor. Liquid assets consist of money held in checking or savings accounts. According to recent research conducted by the Corporation for Enterprise Development, approximately 49% of Floridians are considered liquid asset poor.

Are you “liquid asset poor?” If a household experiences an unexpected financial strain, such as a job loss, illness, or other large expense, and does not have enough liquid assets to cover basic expenses for three months, they are considered liquid asset poor. Liquid assets consist of money held in checking or savings accounts. According to recent research conducted by the Corporation for Enterprise Development, approximately 49% of Floridians are considered liquid asset poor.

Emergency funds focus on increasing liquid assets though savings. An emergency fund can allow households to adapt when unexpected financial strains occur. In the past, three to six months of income was considered to be a good emergency fund. In more recent times, the economy and unemployment have caused households to need much larger emergency funds. University of Florida professor, Dr. Michael Gutter, in “Money and Marriage: Saving for Future Use,” encourages families to consider the following factors:

- How much protection is provided by insurance

- Number of household incomes

- Household needs and fixed obligations

- Family financial support

- Retirement proximity

- Age of children

- Available credit

You can get an estimate of your household’s liquidity by completing the following steps:

1) Calculate the total amount of cash you have on hand and in your checking/savings accounts.

2) Develop a spending plan to allow you to estimate your monthly expenses.

(For help with developing a spending plan, check out Building a Spending Plan)

3) Enter your total cash and monthly expenses into the household liquidity formula:

Total Cash ÷ Monthly Expenses= Household Basic Liquidity

If the household basic liquidity is equal to or less than 1, this would be interpreted as having enough liquid resources to sustain your household’s current spending for only a month or less. If the household basic liquidity ratio is greater than one, that number is the number of months you would be able to live on your liquid assets based on your current spending. If you are not at your desired or expected number, take the pledge to start saving today at America Save$!

References:

Corporation for Enterprise Development. (2014). “Liquid Asset Poverty Rate”

Gutter, M. (2011). “Money and Marriage: Saving for Future Use”

Turner, J. (2001). “Show Me The Money: Lesson 5: Savings and Investments”