The 2016 US crop may still be somewhat of a question mark but USDA’s November numbers provided clarity on a few things—the crop got smaller in some areas as expected and the crop still got bigger overall.

The 2016 US crop may still be somewhat of a question mark but USDA’s November numbers provided clarity on a few things—the crop got smaller in some areas as expected and the crop still got bigger overall.

The North Carolina and South Carolina crops were reduced by a total of 95,000 bales. The Georgia crop is now closer to being correct after being reduced 150,000 bales and the crop could get a bit smaller in all 3 instances. But these reductions totaling almost ¼ million bales were more than offset by increases in Mississippi, Tennessee, and Texas.

US exports are projected at 12 million bales—unchanged from the October estimate. This is a good level of exports considering that China is expected to limit imports for the second consecutive year. As of Nov 10, export sales this marketing year total approximately 7.0 million 480-lb equivalent bales—58% of the USDA estimate. This compares to 47% at this time last year. Shipments total 2.55 million or 21% of the estimate. To date, the pace of shipments projects to only 9.2 million bales for the marketing year—but shipments were 17% at this time last year.

China is expected to import (from all sources) 4.5 million bales this crop year compared to 4.41 million last year. As of 11/10, US export shipments to China totaled approximately 264,400 bales. Sales totaled approximately 910,000 bales or 20% of China’s expected total imports.

This month’s USDA numbers lowered World cotton Use or demand just slightly to 111.99 million bales. In the big picture, this number itself is insignificant. But psychologically, this nervous market will pay close attention to this number. This is only .65% above last year and less than 2% growth since 2013.

One issue is the “price problem” or loss of market share to man-made fibers due to substitution at the mill. Other issues are “structural” and reflect change in consumer preference and buying patterns. Also, part of the decline may be due to cotton production viewed by some as not environmentally friendly and sustainable. Research, education, and promotion are on-going to improve cotton’s image and develop new fabrics that appeal to the consumer. These are longer-term solutions, however.

In the near term, if prices are to sustain themselves at the current level or improve, demand must show stability and growth. Otherwise, price direction will be largely dictated by the supply side—production and production shocks.

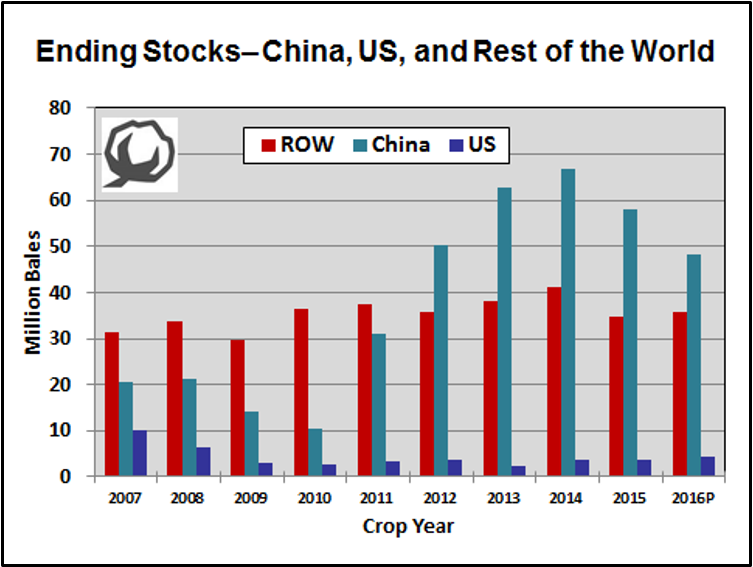

USDA’s November projections revised 2016 crop year World ending stocks up by almost 1 million bales. This was largely the result of a 300K bale increase in beginning stocks (carry-in from the 2015 crop year) and 590K increase in production. The increase in carry-in was due to revisions in production and Use from the 2015 crop year. Higher production is now projected for India along with the US—although the India increase is now questionable. The China crop stands at 21 million bales compared to 22 million last year and 30 million in 2014.

China will have another round of reserve sales in 2017. Sales exceeded 12 million bales in 2016. Sales, plus lower production, and stable/slight increase in Use is projected to trim total stocks by 10.1 million bales by end of the 2016 crop year.

China will have another round of reserve sales in 2017. Sales exceeded 12 million bales in 2016. Sales, plus lower production, and stable/slight increase in Use is projected to trim total stocks by 10.1 million bales by end of the 2016 crop year.

Questions are whether or not reserve sales and pace of sales will match that of this year and whether or not, as sales dig deeper into the stockpile, fiber quality will become a factor.

[important]March 17 futures advanced sharply this week, based on cold weather forecast here in the US, and on reports that both the China and India crops may be lowered. Prices are back above 70 cents—giving growers a good pricing opportunity. Opinion is already circulating that US acreage will be up for 2017. December 17 futures are also slightly above 70 cents—representing an early risk-management opportunity on at least a small portion of expected production. [/important]

Don Shurley – donshur@uga.edu

demayo@ufl.edu - 850-482-9620

Follow me on Twitter

@UFCowman

- 2024 Average Farmland Rental Rates and Worker Wages Summary - December 20, 2024

- 40th Annual Beef Cattle Conference & Trade Show – February 12 - December 20, 2024

- Friday Feature:Carol of the Carillon Bells at UF - December 20, 2024