Many years ago, a young man didn’t take his schooling serious enough and ended up spending some time at lovely Fort Polk, Louisiana. That young man was me and that was my wake-up call. It forever changed my life.

Many years ago, a young man didn’t take his schooling serious enough and ended up spending some time at lovely Fort Polk, Louisiana. That young man was me and that was my wake-up call. It forever changed my life.

I believe the cotton market might be getting a wake-up call right now. We’ve been hinting that sooner or later the market might finally adjust to the different dynamics of the 2017 crop. The past week has certainly not been kind to cotton prices.

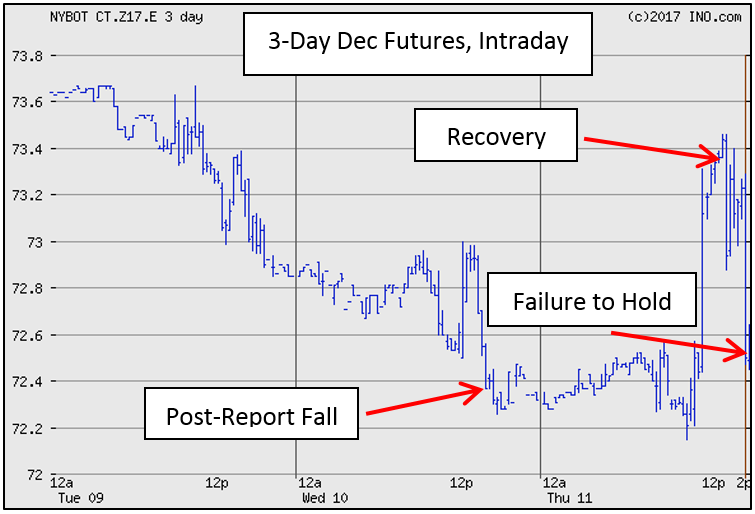

Beginning last Friday, May 5th, new crop December futures prices declined 4 consecutive days—dropping a total of 242 points before finally eeking out a small gain on Thursday.

USDA released its May crop production and supply/demand estimates at noon on Wednesday. After the report, Dec futures declined from near 73 cents to close at 72.33 cents—down 71 points for the day. Prices recovered on Thursday to almost 73 ½, but could not hold and ended the day with just a slight gain. This is not an encouraging sign.

But, there is a level of “support” at 72 cents. Thus far, that floor has held and hopefully it will continue to do so. It’s important to remember that the “dynamics” that will shape the 2017 cotton market are fluid and highly uncertain. As evidence, USDA projects the 2017 crop US average price to be 54 to 74 cents.

Wednesday’s report provided the first estimates for the 2017 crop. The crop is estimated at 19.2 million bales—up just over 2 million bales from the 2016 crop. Not really surprising here, given the expected 21% increase in acres planted. 19 million bales is about the number most folks have been anticipating as a starting point.

Projected exports for the 2016 crop year were raised from 14 to 14 ½ million bales. Worth noting, exports for the 2017 crop year are projected at 14 million bales—a respectable level, but below the 2016 crop year. The larger crop and reduced exports will raise US ending stocks to a projected 5 million bales—1.8 million bales more than this past season.

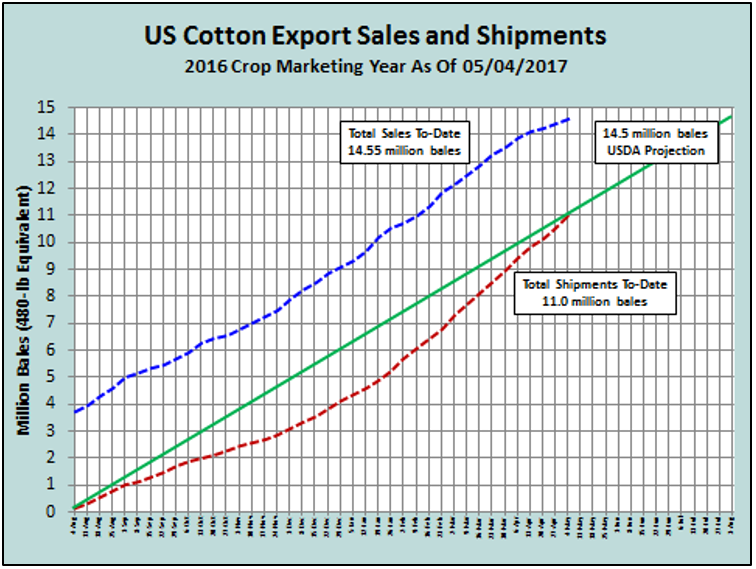

We’ve said here all along that with a bigger crop comes the burden of needing higher usage to keep prices at a high/respectable level. It is possible that before it’s all over, 2016 crop year exports could push even higher than 14 ½ million bales. This will reduce the carry-in to the 2017 crop year and help support prices. As of May 4th, export sales already total over 14½ million bales with 12 weeks remaining in the marketing year. The pace of sales has slowed, but that’s to be expected. Actual shipments total 11 million bales—76% of the new USDA projection, and on pace to meet or exceed the projection.

As of May 4th, export sales already total over 14½ million bales with 12 weeks remaining in the marketing year. The pace of sales has slowed, but that’s to be expected. Actual shipments total 11 million bales—76% of the new USDA projection, and on pace to meet or exceed the projection.

Elsewhere in Wednesday’s report, there are uncertain dynamics in play—projected World use/demand for the 2016 crop year was revised up 600,000 bales; the India crop was lowered ½ million bales; China mill use was raised ¾ million bales; China imports raised 300K bales; and 2016 crop year projected ending for China lowered almost ½ million bales.

All in all, these are certainly not bearish numbers. Any “downers” in the report, if any, would seem to be associated with the upcoming 2017 crop year:

- World production is projected to increase 7.34 million bales; with the largest increases in US, India, China, and Turkey.

- World use/demand is projected to increase 2.55 million bales; China up ½ million bales, Vietnam up 600K bales, Bangledesh up 400K bales.

- The increase in production will outpace the increase in demand by almost 5 million bales—but, Use/demand will still be ½ million bales more than production.

- This compares to 7.3 million bales more demand than production this season.

- China is forecast to import 5 million bales compared to 4.8 million this year and 4.4 million for 2015-16.

- China’s ending stocks are forecast to decline by 9 million bales. Stocks are projected to decline 9 ½ million bales this season.

It’s difficult to see much “bearishness” in these numbers. Yes, production is expected to increase, but Use is also expected to increase. Production and Use will be in much closer balance, but stocks are projected to continue to dwindle down. The US crop, if realized as projected, will be big with no increase in exports expected—so US stocks will increase. This could put a little pressure on prices.

Moving forward, the market will begin to focus on the US crop plantings and condition; signs that Use/demand is or is not showing, continuing signs of recovery; and foreign production—expected higher production this year in the key countries noted.

Is this our wake-up call? The action of the past 2 days would suggest so—but I also see some positives in the outlook. USDA’s suggested possible price range of 54 to 74 cents says anything is still possible. I’ll feel better if the support at 72 cents holds.

demayo@ufl.edu - 850-482-9620

Follow me on Twitter

@UFCowman

- May 2025 Weather Summary and Summer Outlook - June 20, 2025

- Friday Feature:The History of Angus Cattle - June 20, 2025

- Friday Feature:High Quality Legume Hay Production – Virtual Tour of Conrad Farms - June 6, 2025