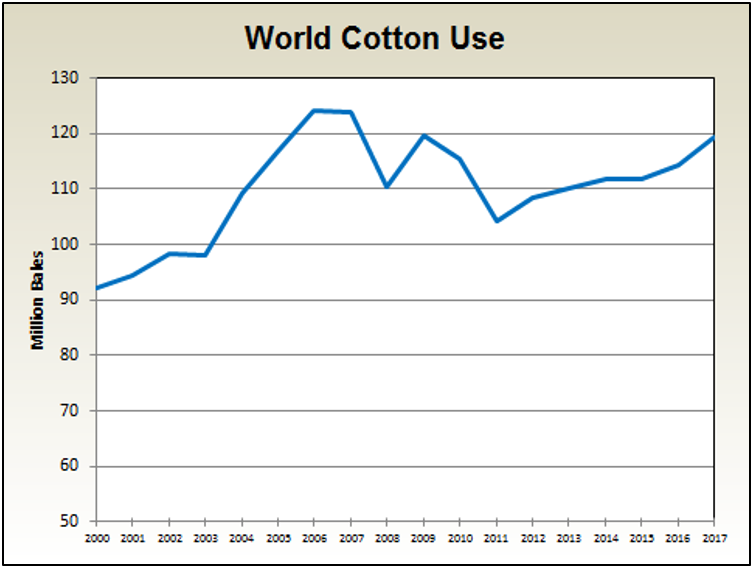

Back in May, when most of the 2017 cotton crop still remained to be planted, USDA released its first supply and demand projections for the 2017 crop marketing year. That first projection for total World use was 115.75 million bales. That was back in May. The most recent (November) projection is now 119.25 million bales—3 ½ million bales or 3% higher.

If realized, this would be a 15 million bale or 14% increase since the most recent low back in the 2011 crop marketing year. More importantly, it would represent a 5 million bale increase since just last season and an almost 8 million bale increase in just the last 2 to 3 seasons.

World cotton Use peaked at roughly 124 million bales but then declined 10 million bales or 16% to a low of 104 million bales for the 2011 crop year. Use has slowly begun to recover and if 2017/18 holds true, will be only 5 million bales below the peak. We still have a way to go but the outlook has certainly improved compared to just a few years ago.

This is significant for 2 reasons. First, demand or Use is one-half of the supply/demand equation. Increased demand sets the foundation for higher prices depending on what also happens on the supply side. Secondly, demand and demand growth ultimately determines how much cotton production (and acres planted) is needed both here in the US and abroad. In other words, if we want a vibrant, growing US cotton industry—demand is the key component.

Perhaps an overly simplistic view, but demand growth can come from 3 sources—“natural” increase due to population increase, increase due to improved market share (taking back market previously lost to substitutes like man-made fibers), and development of new products that capture lost demand or create new demand.

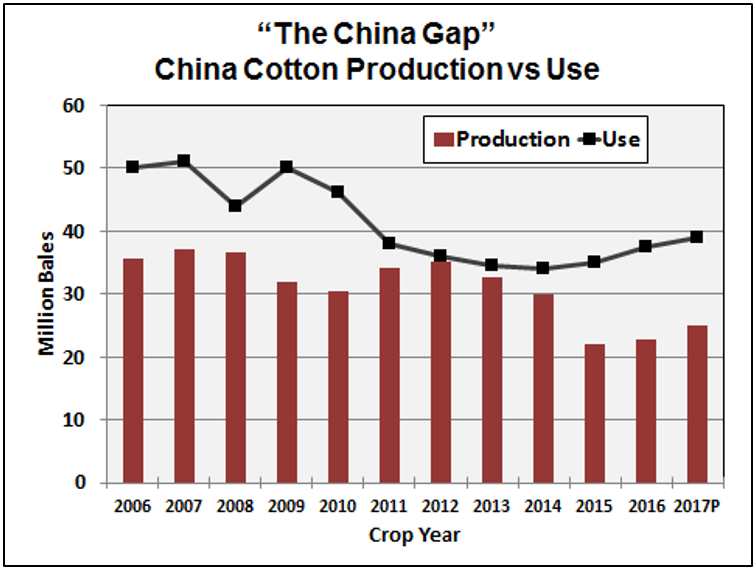

After the low in 2011/12, demand or Use began to slowly improve but then hit a plateau at about 111 to 112 million bales. China is the largest cotton user and accounts for roughly one-third of total World Use. Since the low in 2011/12, Use has now increased 15 million bales—3.5 million bales in Bangladesh, 4.4 million in Vietnam, 5.05 million in India, only 1 million bales in China, and all others 1.05 million bales. If the small increase in China surprises you, China’s Use continued to decline and/or plateau until last season while Vietnam, Bangladesh, and India were increasing and thus responsible for most of the growth.

China’s mill industry currently uses about 38 to 39 million bales of cotton per year. China produces only 24 to 25 million bales. This “China Gap” is filled by imports and utilizing stocks built up from previous years production and imports. Right now, for the past couple of years, China has reduced production and limited imports in an effort to utilize its own production and reduce its buildup of stocks. Production has increased but still below historical levels.

If China’s Use continues to rebound, this could create the need for more imports depending on their stocks situation and their own production. Exports account for almost three-fourths of the total demand for US cotton. China is one of our major markets even though they are currently limiting imports. Eventually, China is likely going to have to ramp up its imports—it’s a matter of when and by how much and the pace of it happening. This could bode well for prices.

March futures prices have been in a range of mostly 67 to 70 cents. But even within this range, prices have trended up since the most recent low and look to challenge 71 cents if the ceiling at 70 cents is broken.

Prices have improved due to the news of 119+ million bales World Use in the November USDA report, strong export sales, rumors that China may end up buying more imports than USDA is currently projecting, and weather concerns about the west Texas crop and opinion by some observers that the US crop is still ultimately going to get smaller. A move above 70 cents presents a good opportunity to make additional sales on a portion of uncommitted production.

Christmas will be upon us before you know it. As my highly respected fellow cotton market economist O.A. Cleveland says—“Give the gift of cotton”. Demand is the key to cotton’s future.

—

demayo@ufl.edu - 850-482-9620

Follow me on Twitter

@UFCowman

- June 2025 Weather Summary and Three-Month Outlook - July 11, 2025

- Friday Feature:Pipeline Farming Accident - July 11, 2025

- May 2025 Weather Summary and Summer Outlook - June 20, 2025