Don Shurley, Professor Emeritus of Cotton Economics

Don Shurley, Professor Emeritus of Cotton Economics

On June 14, I had the pleasure and honor to present for the University of Arkansas Extension Service as part of their Food and Agribusiness Webinar Series. Thanks to my long-time colleague and friend Dr. Bobby Coats for the invitation and opportunity. The following are a few of the slides from that presentation and the comments made.

Market Factors

There are several factors influencing cotton prices. All have been discussed and well-known within industry. Specifically, the uncertainty surrounding acreage and the condition of the US crop, questions also about foreign production, and improving demand/use and strong US exports. Let’s briefly look further at each of these and related issues.

There are several factors influencing cotton prices. All have been discussed and well-known within industry. Specifically, the uncertainty surrounding acreage and the condition of the US crop, questions also about foreign production, and improving demand/use and strong US exports. Let’s briefly look further at each of these and related issues.

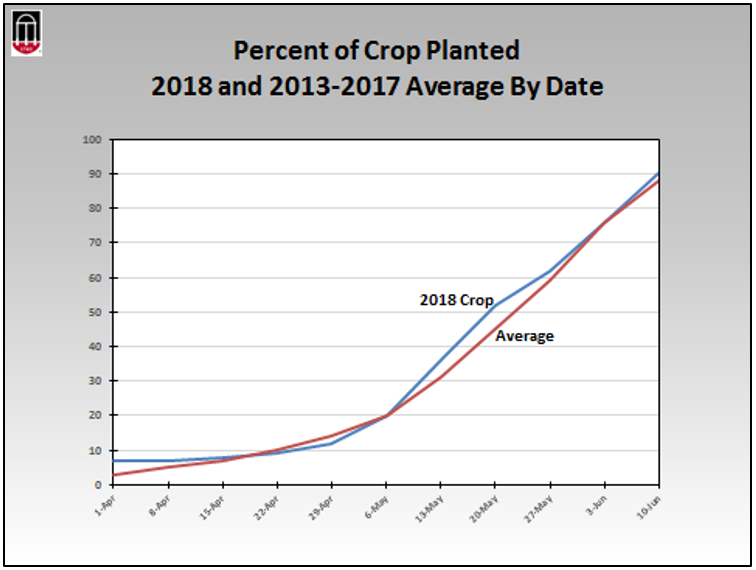

Planting

When you look at the total crop, planting progress has been on average or ahead of normal pretty much all season. But this is misleading and not a good indicator of the situation. Texas has been very dry and some of that crop was dusted in just to meet the crop insurance deadline. The Southeast was delayed due to wet conditions and, again, growers rushed to try to get the crop planted in June. Georgia has been 6 to 12 points behind normal for the past few weeks.

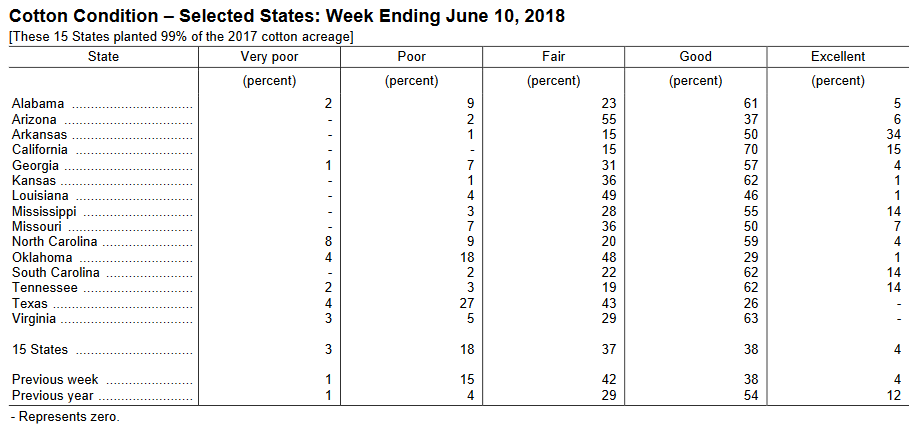

Condition

The Texas crop is 31% poor or very poor; the Oklahoma crop 22%. The Mid-South and Southeast crops are in mostly fair to good condition. When you combine the planting situation in Texas with this crop condition, it does not bode well unless things make a dramatic turn-around. This is what the market has been reacting to.

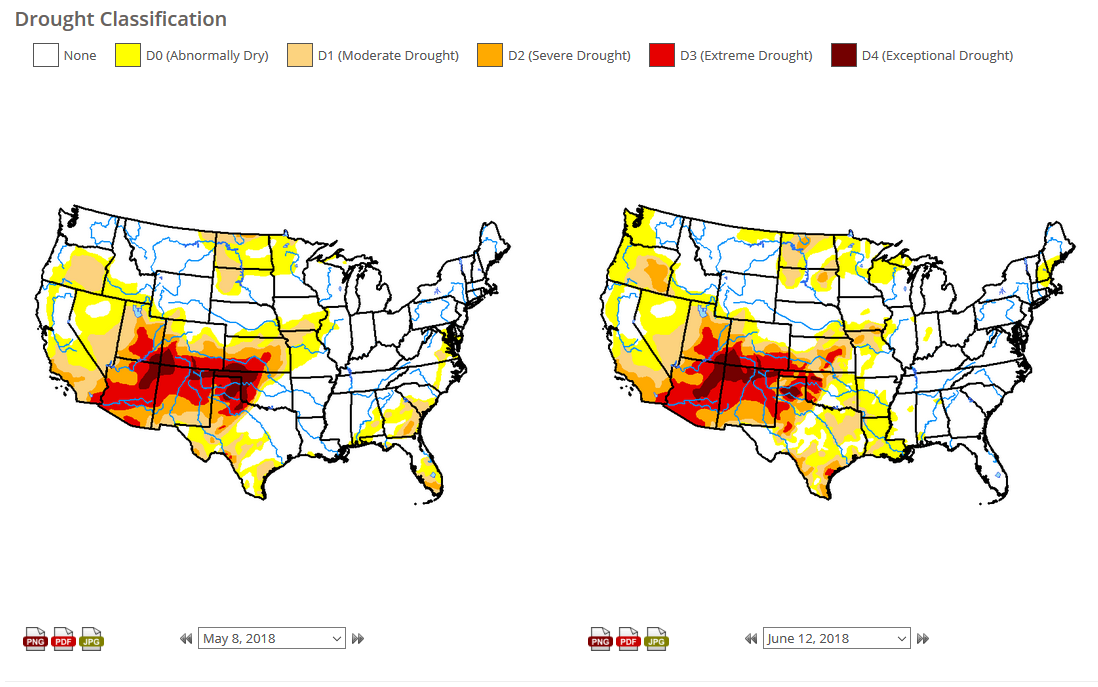

Drought maps compare last week to a month earlier. The Texas-Oklahoma situation has improved but only slightly. The Southeast has improved—but too much rain has hampered some of the crop and crop activities in Georgia.

Drought maps compare last week to a month earlier. The Texas-Oklahoma situation has improved but only slightly. The Southeast has improved—but too much rain has hampered some of the crop and crop activities in Georgia.

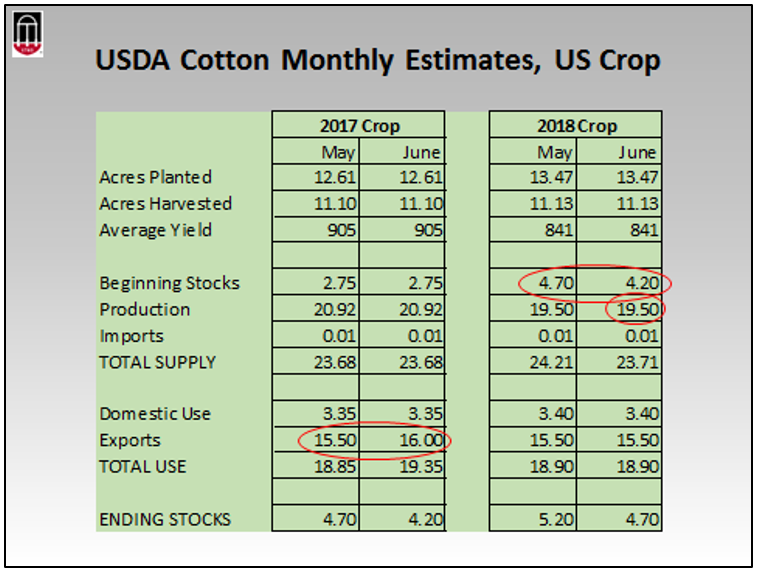

USDA Monthly Estimates—US Crop

This weeks (June 12) USDA crop production report pegs the 2018 crop at 19.5 million bales with a yield of 841 lbs—the same as the initial estimate in May. This is a bit of a surprise given the condition of the crop. We’ll discuss in a little more detail later, but exports for the 2017 crop were revised up for the second straight month, and this further reduces the carry-in to the 2018 crop year on Aug 1.

Uncertain Foreign Production

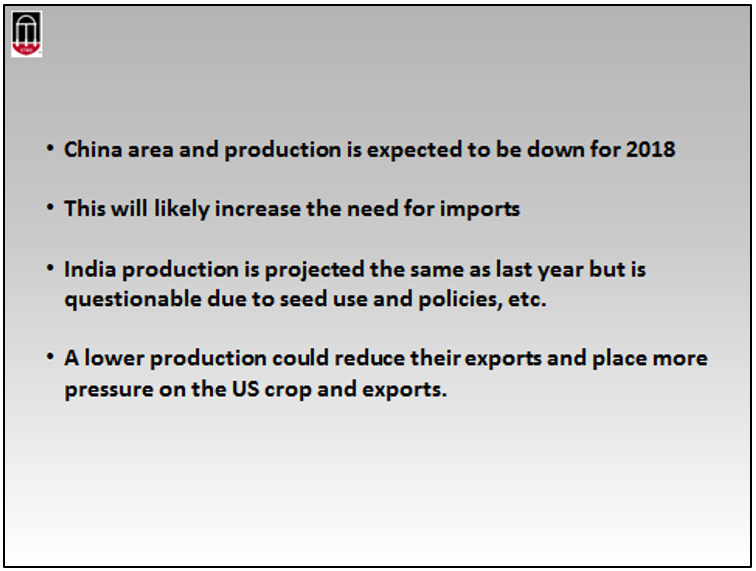

The 2018 Chinese crop is expected to be 26 ½ million bales—500,000 bales less than the May estimate and 1 million bales less than last year. Some believe the crop may be less than this. With Use doing well, this is going to increase the need for imports and/or more use of their stocks. I saw an announcement just this morning that China will increase their import quota by 800,000 tons—which if my math is correct, would be an over 3 million bale increase. The 2018 India crop is projected the same as this past year, but this too could be questionable. I read a story just this week about how Indian growers are using unapproved Monsanto seed. With World use/demand expected to grow, any hiccup in India production could reduce their exports and put more pressure on the US crop and US exports.

The 2018 India crop is projected the same as this past year, but this too could be questionable. I read a story just this week about how Indian growers are using unapproved Monsanto seed. With World use/demand expected to grow, any hiccup in India production could reduce their exports and put more pressure on the US crop and US exports.

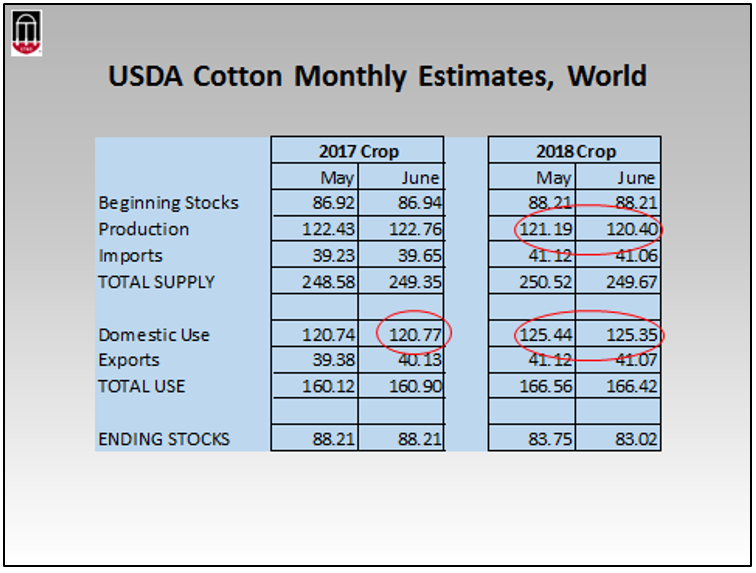

Improving Use – World Monthly Estimates

World Use for the 2018 crop year is projected at over 125 million bales. If realized, this would be a record Use and 3.8% growth from this season. Use for the 2017 crop year is now projected at almost 121 million bales—which is 5.2% above 2016.

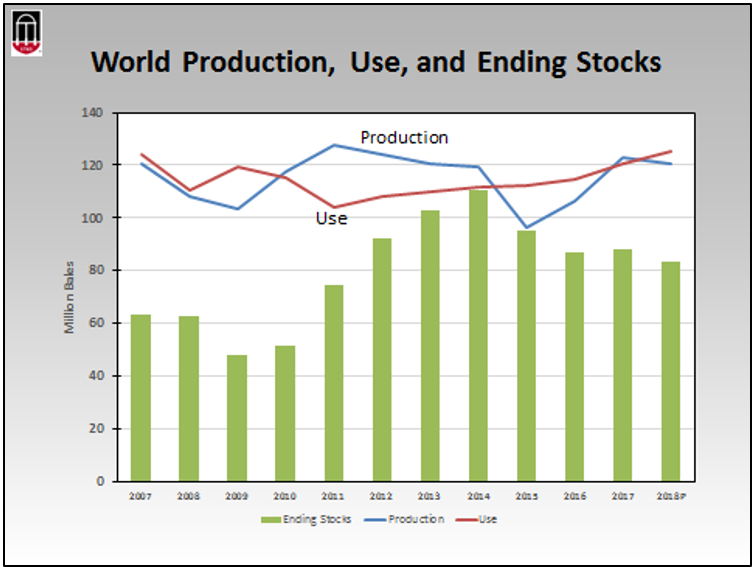

World Production, Use, and Ending Stocks

For the 2018 crop year, Use is expected to exceed production by almost 5 million bales. Stocks will continue to decline and while still higher than 10 years ago, stocks are now approaching “pre-buildup” levels. In fact, if you consider the improvement in Use, the projected stocks-to-use ratio is 66%, which would still be higher but approaching “pre buildup” years. In some respect, the level of World stocks is largely irrelevant anyway due to China’s policies—we know most of that stockpile is not currently in the “pipeline”.

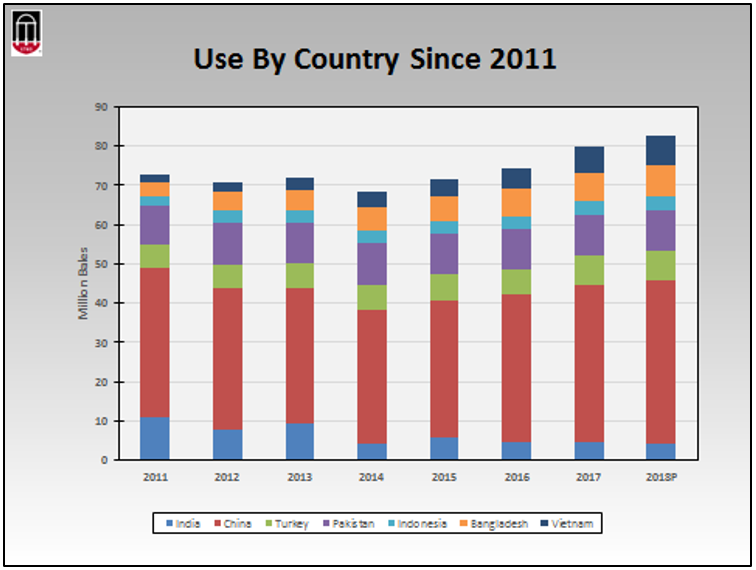

Use By Country

Since the low in 2011, the rebound in Use has been evidenced in China, but most notable in relatively new and expanding markets like Vietnam and Bangladesh. Use in India has not grown and been stable in recent years. Increased focus has been on exports, but their exports depend on production and stocks. Mills in these 7 countries account for 86% of total World use.

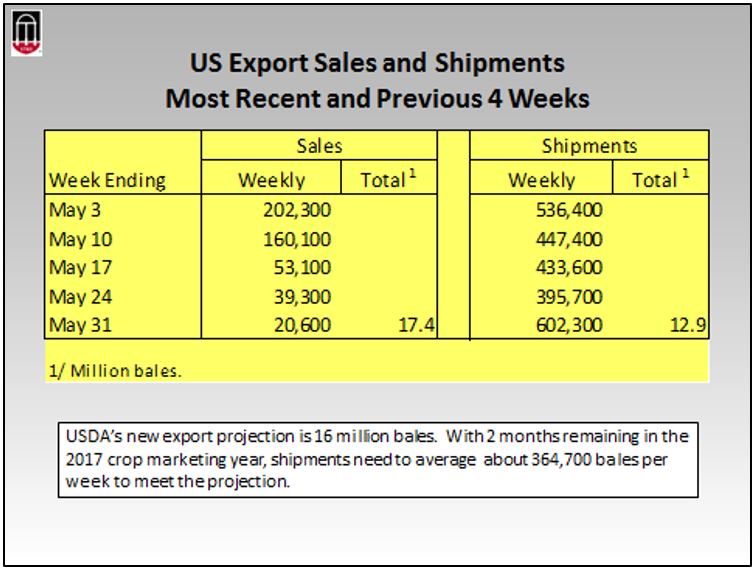

Export Sales and Shipments

Looking at the most recent weekly export report numbers, sales have fallen off and this could be due to higher prices. As of May 31st, sales totaled 17.4 million bales. Shipments have been very strong, and as of May 31 totaled 12.9 million bales. Shipments need to average about 365,000 bales per week to meet USDA’s new 16 million bale estimate. This certainly seems do-able based on recent pace.

UPDATE: For the week ending June 7, sales were 44,000 bales and shipments 483,000 bales. This brings total shipments to 13.3 million bales—83% of the projection for the marketing year.

Top Customers

As of May 31st, shipments were 80.4% of the new USDA projection. This is right in line with last season at this same time. Sales for the 2018 crop already total 4.8 million bales. Top customers (country of destination) for the 2017 crop include Vietnam, China, Turkey, Indonesia, and Pakistan. This is based on sales, not actual shipments to date.

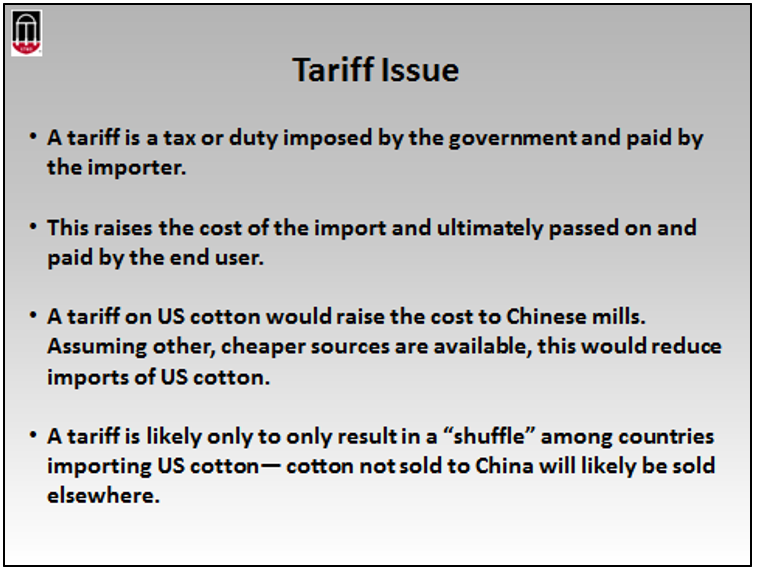

Tariff Issue

The US-China tariff situation remains uncertain. A tariff imposed on raw cotton imports would raise the cost of US cotton to Chinese mills. Should this result in less demand for US cotton, it could hurt prices in the short term, but ultimately would likely only result in increased US exports to other countries or a “shuffle” in exports.

The market certainly doesn’t seem overly concerned at the moment about the impact of any tariff. As mentioned previously, China has announced an increase in import quota.

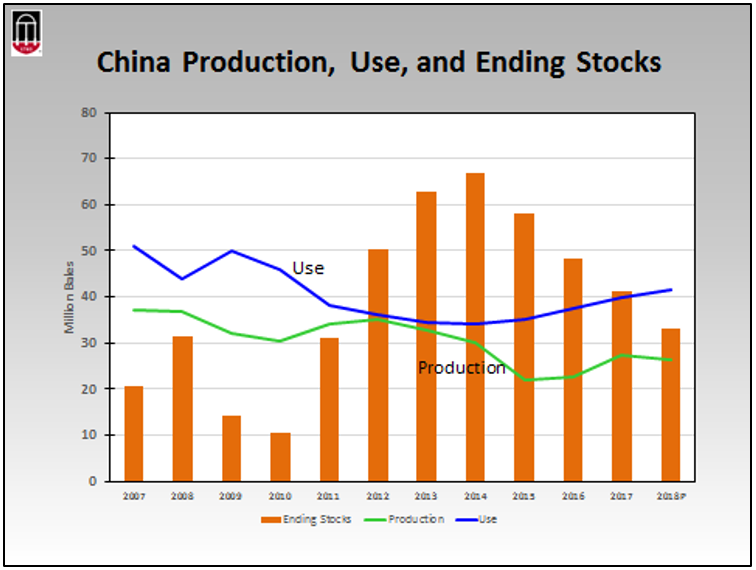

China Production, Use, and Ending Stocks

The World supply/demand picture has improved dramatically over just the past several years. This can be evidenced in-part by looking at the China situation. China has reduced its stocks by 38% since the peak in 2014-15. Stocks are projected to decline another 8 million bales for the 2018 crop marketing year.

China’s cotton production has always been less than its use. Its mills rely on imports and stocks to supply the difference. With demand/use improving in combination with lower production, this has created what I have called the “China Gap” and this difference between use and production is widening.

Outlook

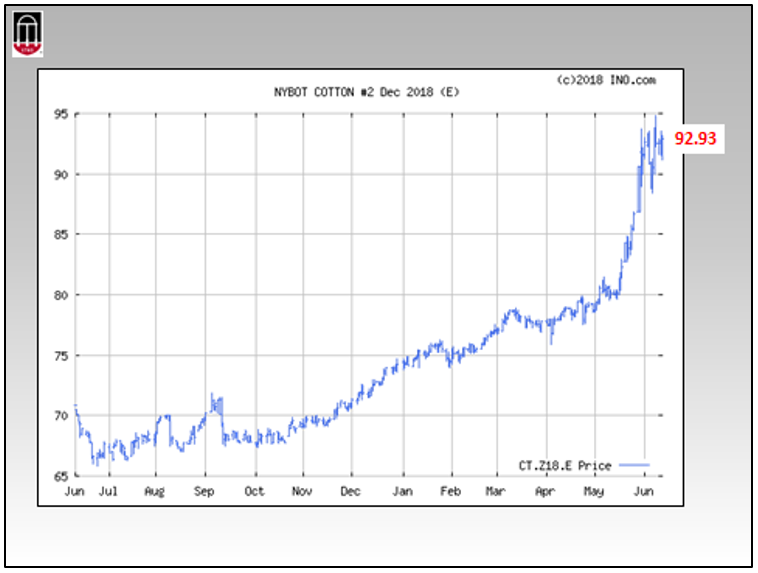

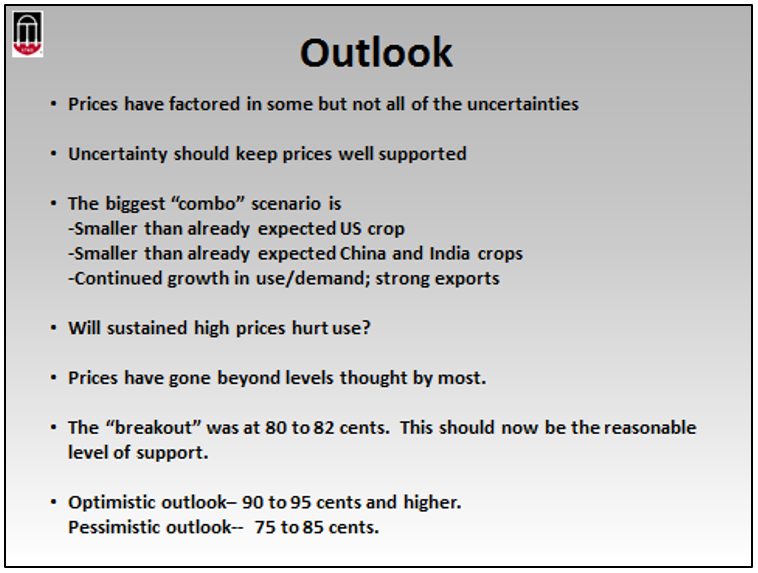

New crop December futures prices are in the low 90’s. It is the role of the futures market to take all that we know or think we know and determine what the price (of cotton, in our case) should be at some future point in time. The market at 90 cents has factored in what we have discussed. But there are still uncertainties that will be played out in the weeks and months ahead. This uncertainty should keep the market well supported.

I can draw you a number of scenarios that could play out, and each would impact price in a different way. If the US crop eventually comes in less than the current estimate, if the China and India crops are smaller than expected, and provided use/demand remains strong, this should keep prices strong.

UPDATE: On June 15, Dec futures closed below 90 cents—down over 3 cents for the day. Traders and news sources cited escalating trade tensions between the US and China as reason for the decline. Prices (Dec futures) have trended up since November. The real “break out” came at around 80 to 82 cents. This should be a good level for support. I’m not saying prices are headed south; just saying if weakness develops, around 82 should be the floor.

Prices (Dec futures) have trended up since November. The real “break out” came at around 80 to 82 cents. This should be a good level for support. I’m not saying prices are headed south; just saying if weakness develops, around 82 should be the floor.

Given all the factors we have discussed, as we move forward 90 to 95 cents or higher is my optimistic outlook; 75 to 85 cents is the pessimistic outlook.

Marketing Comments

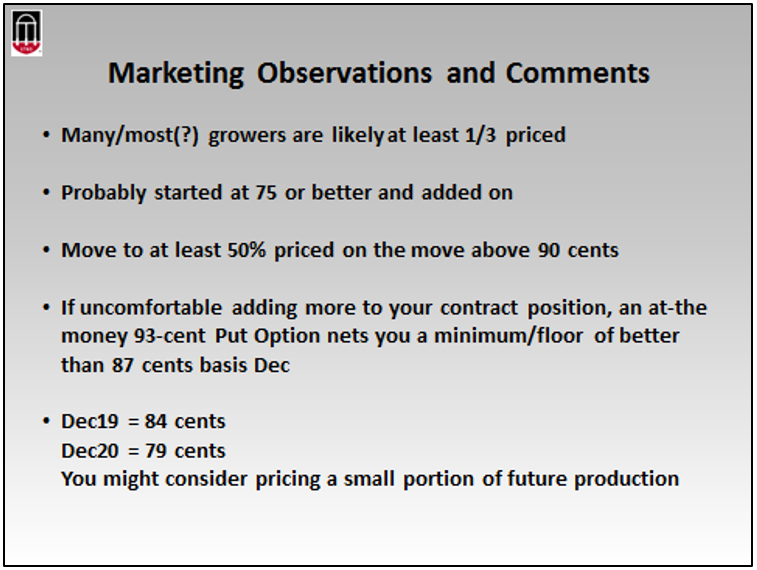

I believe many (maybe most) producers are at least one-third priced on their 2018 expected production. Their decisions likely started at around 72 to 75 cents Dec futures and have scaled up from there as prices have improved.

If not already and if I were a grower, I’d move to at least 50% maybe 60% priced on the move above 90 cents. If uncomfortable adding any more to contracts, a Put Option can net a floor of about 87 cents basis the Dec futures.

Well Known and highly respected analyst Dr. O.A. Cleveland recently had an excellent article mentioning the good pricing opportunities available on the 2019 and even 2020 crops. Excellent advice and I concur.

—

demayo@ufl.edu - 850-482-9620

Follow me on Twitter

@UFCowman

- Making the Most of High Cattle Prices – Grow More of Your Own Feed - July 18, 2025

- Friday Feature:1960 Corn Farmer - July 18, 2025

- June 2025 Weather Summary and Three-Month Outlook - July 11, 2025