Don Shurley, UGA Professor Emeritus of Cotton Economics

Recently, I have often been asked if cotton prices are going to get better. It’s a tough question and no one knows the answer. There are positive scenarios that would push price up but the market continues to be hammered by negative forces.

For the producer, let’s think about (1) what would you consider “better” and (2) what price would be good enough to entice you to sell an additional amount of 2019 production?

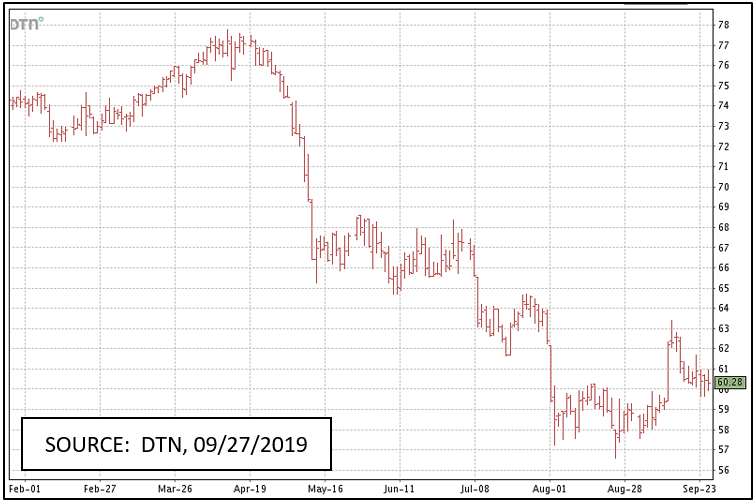

What is making this situation so frustrating is the whip-saw of daily and weekly ups and downs in this market. There is no direction and it seems the slightest bit of news, pro or con, whether truly significant or not, seems to get a reaction. It’s like the market is so sensitive and so uncertain that it reacts to almost anything. December futures are currently in the neighborhood of 60 cents. Right now, 60 to 61 cents is the barometer for this market—over 61 is considered getting “better” and moving in the right direction.

After trading below 60 cents for a month and a half, Dec futures broke out to over 62 cents on September 12, after President Trump announced that a tariff increase by the US scheduled for October 1 would be delayed until October 15. This was after China announced it would exempt tariffs on some US imports.

Both of these were positive signs in the long trade war and talks are scheduled to begin again in October. Cotton, and other markets, are clearly poised to move higher if and when significant progress can be made on the US-China trade front. Since that time, however, prices (Dec futures) have again lost ground but still stand above 60 cents. For this week, December closed at near 61 cents and up almost ½ cent for the week. Again, 60 to 61 seems to be the barometer or measuring stick for this market. An eventual trade deal with China is important. Specifically, as far as we are concerned, a deal that is positive for the US cotton producer. But there are also other factors that are important.

- A troublesome trend has developed. USDA’s September supply and demand estimates now project World cotton use for the 2019 crop marketing year to be 121.74 million bales—down 1.33 million bales from the August estimate and the 4th consecutive month that projected use/demand has been cut.

- USDA’s September numbers reduced US exports for the 2019 crop year by 700,000 bales. This could not have been unexpected. The previous export number was too high anyway given the uncertain trade environment and the weakening demand picture.

- The US crop is shrinking and will likely get smaller. The overall crop condition has worsened during this month. The US crop is now projected at 21.86 million bales—down 660,000 bales from the August estimate but still 3 ½ million bales above last year.

- The revision in exports pretty much matches the reduction in the US crop. This may suggest that the reduction in exports was more due to less available supplies than weaker demand. That would be concerning because it could suggest that further downward revision in exports is possible.

- A recent report suggests that the India crop could be up 20% this year. This compares to an 11% increase based on USDA estimates.

- Export sales over the past 4 weeks have averaged 131,000 bales per week. This week’s report was relatively good at 170,500 bales but sales during September have been below the levels in August.

A repeat of prices in the 57 to 58 cent area is possible, if the trade war continues to drag out and if demand continues to weaken. A smaller US crop may provide some support (being able to hold above 60 cents), but will not likely give prices the upward jolt we want without positive news on the trade and demand front also.

Producers need to protect against the advent of lower prices, while hoping that prices move higher. Perhaps the best way to do this is to put the cotton in Loan where a MLG can offset a drop in price. Using Call Options is also a possibility, but the premium is an additional expense. Taking any LDP/POP and holding the crop will not protect you. Taking a “provisional” or deferred price contract will not protect you, unless it also provides a minimum price.

demayo@ufl.edu - 850-482-9620

Follow me on Twitter

@UFCowman

- June 2025 Weather Summary and Three-Month Outlook - July 11, 2025

- Friday Feature:Pipeline Farming Accident - July 11, 2025

- May 2025 Weather Summary and Summer Outlook - June 20, 2025