Don Shurley, UGA Professor Emeritus of Cotton Economics

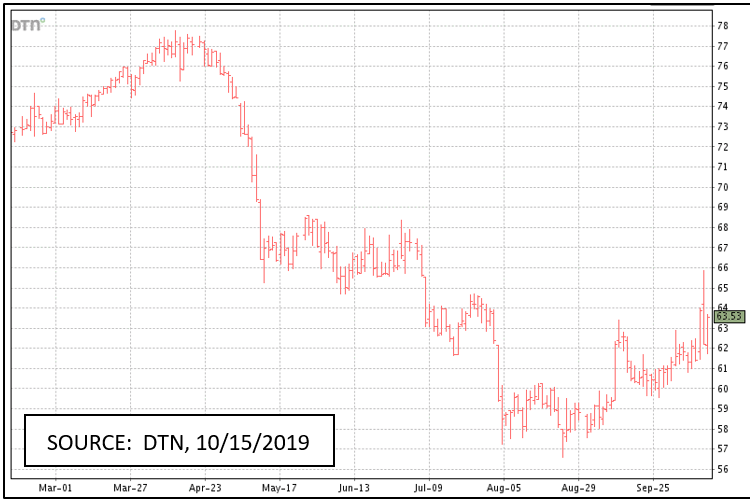

Cotton growers, in the midst of the harvest season, are waiting for prices to show some improvement before pricing any remaining portions of the crop. While the seesaw action in price continues, it increasingly appears that an uptrend (if we dare to even mention that word) has been established. If this uptrend fails (and it could), there is support established at 60 cents.

Growers need to set a few price goals/targets and then be prepared to market a portion of the remaining uncommitted crop when the target is met. This market is highly volatile and uncertain due to the still unknown results of the US-China trade talks. Setting goals/targets will take the emotion out of the equation.

Prices have trended up for several reasons including—increasing hopes on the trade front, a smaller US crop, and more stable USDA October numbers, and “corrections” from 2 previous lows. These lows occurred at the 58¢ area and at the 60¢ area.

I’m not going to take space here to attempt to chronicle the week to week adventures of the US-China trade talks. Honestly, it’s fruitless to attempt to explain and understand the process. Good news one day can and is too often contradicted a short time later, or the “good” rumor or news not followed through on.

But let me make one important observation—this market will take no sustained direction until some degree of negotiation is done and in place. Not just talk, but actions agreed to. Or let’s put it a more positive way—this market is poised to rebound once we have a more firm handle on the trade front.

Until such time, we can expect more frustrating and meaningless seesaw action. Case in point—last Friday December 19 futures closed up 2.46 cents; yesterday down 1.66 cents; today December closed at 63.53 cents—back up 1.31 cents. Last week news broke that the US and China might reach a partial deal. Today, I see headlines that the two sides are still far apart. So really, who knows for sure.

My point is this—holding cotton (too much cotton) in hopes of this fickle trade war being resolved, is likely too risky a proposition. Holding but with downside protection seems more prudent. The market has proved that it is willing to move up on positive trade news. Potential is there. But it can’t yet be sustained. Potential is what we call “pent up”.

Here’s a brief summary of USDA’s October estimates for the 2019 crop marketing year:

- The US crop was reduced slightly. Overall, the reduction was less than what some expected.

- US exports remain projected at 16.5 million bales.

- World demand/use was lowered slightly by 130,000 bales.

- The Southern Hemisphere crop (Australia and Brazil) was reduced 600,000 bales.

- China’s imports were reduced ½ million bales.

- Use was lowered for Vietnam.

Export sales for the week ending October 3rd were 204,400 bales—up approximately 14% from previous weeks, but still not a particularly strong number. Sales stand at 9.4 million bales compared to 9.7 million bales at the same time last season. Sales to China currently total 1.82 million bales—19% of total sales thus far, and also 19% share of China’s projected imports of 9.5 million bales.

Producers should carefully evaluate marketing opportunities on price increases—pricing portions of the crop on advances. Set your goals/targets and then pull the trigger when the market gets there.

demayo@ufl.edu - 850-482-9620

Follow me on Twitter

@UFCowman

- May 2025 Weather Summary and Summer Outlook - June 20, 2025

- Friday Feature:The History of Angus Cattle - June 20, 2025

- Friday Feature:High Quality Legume Hay Production – Virtual Tour of Conrad Farms - June 6, 2025