Don Shurley, UGA Professor Emeritus of Cotton Economics

The coronavirus is the big factor in the news lately. It’s hard to separate fact from rumor, or know how much to believe what you hear in the news. I believe what we hear is a mix of the facts seasoned with emotion and fear.

Markets have reacted to the situation and cotton is no exception. Fear or facts, there is an economic slowdown in China, here in the US, and globally. China’s economy is already being impacted, as plants and other facilities are closing.

–

–

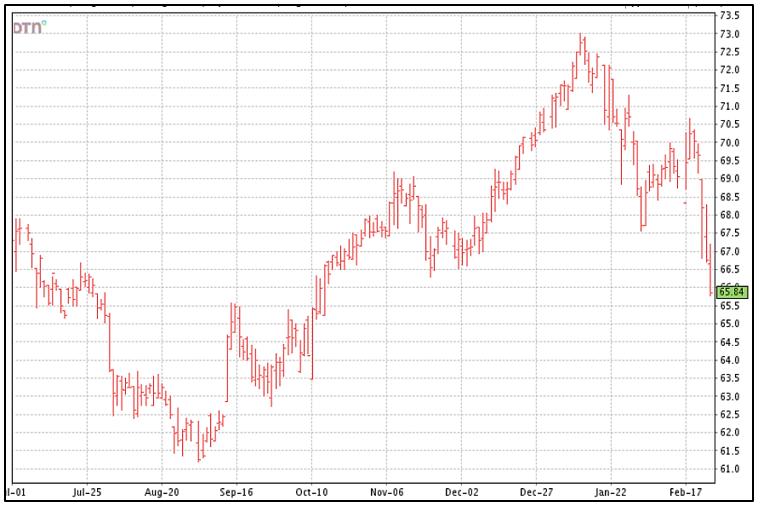

The cotton market earlier declined on news of the virus, then improved on news that China was getting a handle on managing the situation, but now has declined sharply on news of the situation worsening and the subsequent economic slowdown. Old crop May futures has lost 3.53 cents thus far this week, and currently stands at roughly 65 ½ ¢. New crop December futures has lost 3.81 cents this week, and currently stands below 66 cents.

At less than 70 cents, cotton will lose even more ground to corn and soybeans. The National Cotton Council’s survey-based estimate of planting for 2020 is 12.98 million acres. If realized, this would be 5.5% lower than last year. Based on recent year’s average abandonment and yields, this would peg the 2020 crop in the neighborhood of 20 million bales, compared to last year’s crop of 20.1 million bales. Cotton below 70 cents will likely cause an even larger reduction in acres, although I expect acreage in Texas and Georgia to be more stable compared to other parts of the country. USDA’s first planting estimate will come out March 31.

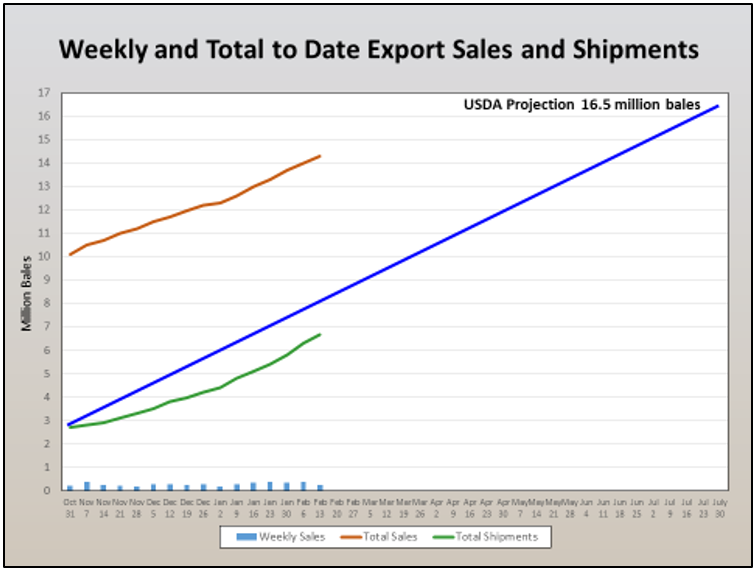

Buying activity pulls prices up—whether it be from users or speculators. Export sales and shipments have both been strong over the past month or more—although for the week ending February 13, sales were the lowest level in 5 weeks.

It remains to be seen if and when there will be purchases from the Phase 1 agreement with China. Overall, sales and shipments have been good, but sales to China have been slow and essentially non-existent over the past month. This is likely a slowdown due to the coronavirus.

–

–

Sales, as of February 13, were 14.3 million bales. Shipments were 6.7 million bales—40% of USDA’s projected total for the marketing year. This compares to 37% at this time last year. Despite the pace of sales and shipments, it’s hard to conceive meeting USDA’s 16.5 million bales projection without sales to China picking up.

USDA’s February supply/demand numbers were not good for price direction. World production was raised 850K bales, and demand/Use was revised down another 1.21 million bales—1 million bales in China alone.

The path to higher prices is a positive resolution to the coronavirus situation, stronger exports to China, and improved World demand/Use. If prices don’t move back above 70 cents by planting time, less US acreage and then weather and crop conditions will also factor in.

Producers should eye opportunities at 72 to 73 cents.

–