by Ethan Carter | Jun 20, 2025

Ethan Carter, Regional Crop IPM Extension Agent; Hardeep Singh, Cropping Systems Specialist; Michael Dukes, Director of UF/IFAS Center for Land Use Efficiency; and Lakesh Sharma, State Ag BMP Coordinator In recent years, the University of Florida has worked...

by external | Jun 20, 2025

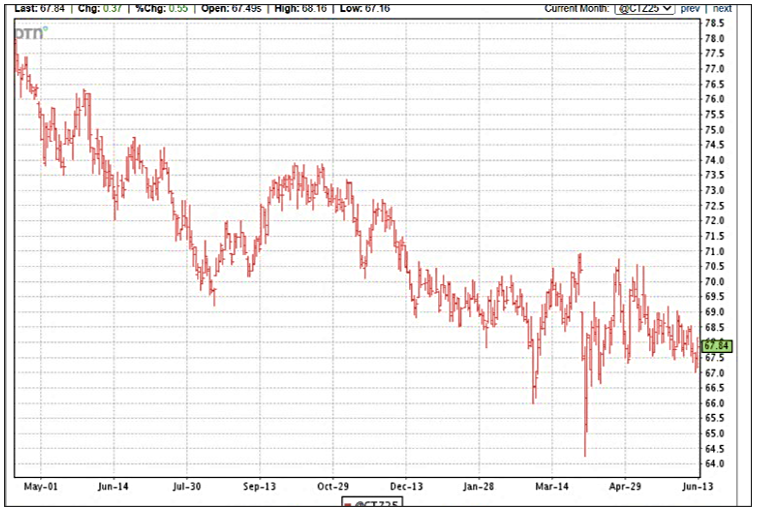

Don Shurley, UGA Emeritus Cotton Economist Last week’s USDA monthly supply/demand estimates for June do not contain enough good news to support higher prices. But also, there’s not enough negative news to call for price to move lower. So, prices (December 2025...

by Ethan Carter | Jun 20, 2025

UF/IFAS is hosting a Row Crop Field Day on July 21st at the North Florida Research and Education Center in Quincy (155 Research Road, Quincy, FL-32351). The field day will be held from 9:15 AM to 3:30 PM (8:15 AM to 2:30PM CDT) and will focus on cotton and...

by mutrimermorata | Jun 20, 2025

UF/IFAS Extension and the West Florida Research and Education Center (WFREC) invite growers, consultants, and ag industry professionals to attend the 2025 Corn & Soybean Field Day on Tuesday, July 22, from 8:00 AM to 1:00 PM CDT at the WFREC research farm in Jay,...

by Ethan Carter | Jun 20, 2025

The annual UF/IFAS Peanut Field Day will be held at the North Florida Research and Education Center in Marianna (3925 Hwy 71, Marianna, FL 32446) on Thursday, August 14, 2022. Registration and CEU sign-in starts at 7:30 AM (CDT) and the event ends with a...

by external | Jun 6, 2025

Ed Borgato, UF/IFAS Weed Scientist, West Florida Research and Education Center – Jay A suitable variety planted in the appropriate window, with fertilizer applied in the appropriate timing, at the required rate for desired yield, plus weeds, insects, and diseases...