by external | Jun 20, 2025

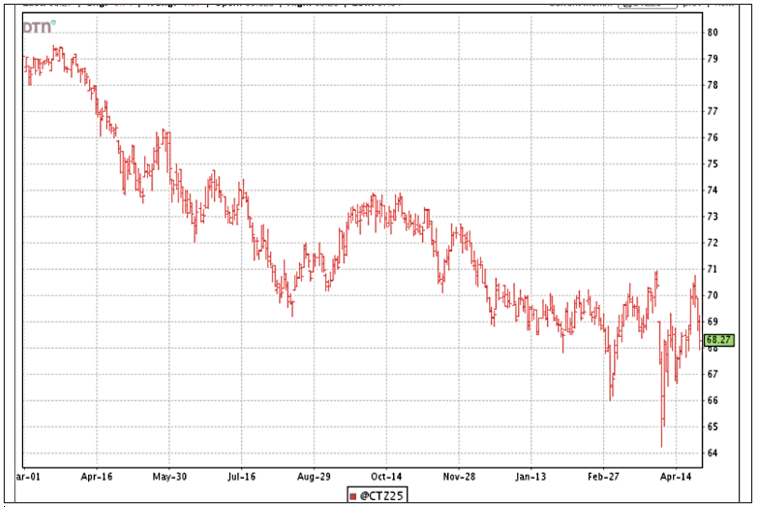

Don Shurley, UGA Emeritus Cotton Economist Last week’s USDA monthly supply/demand estimates for June do not contain enough good news to support higher prices. But also, there’s not enough negative news to call for price to move lower. So, prices (December 2025...

by Hannah Baker | Jun 6, 2025

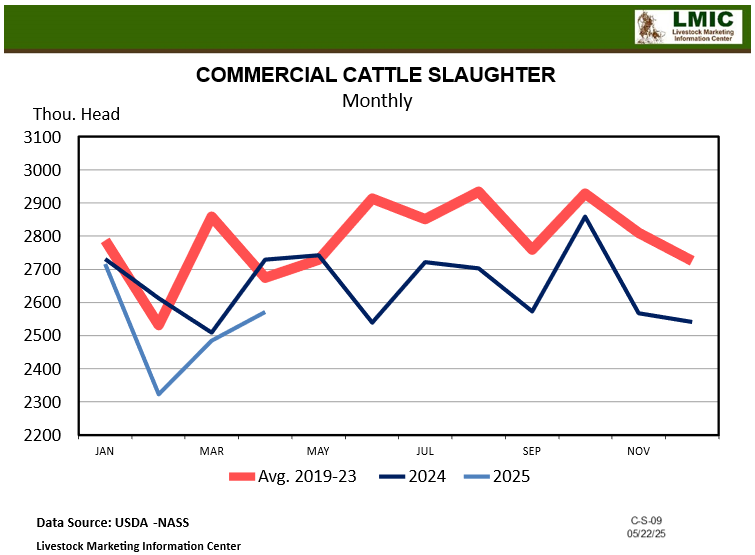

Livestock slaughter in the first quarter of 2025 (January-March) totaled at 7.38 million head, down 4% from the first quarter of 2024. Cow slaughter, beef cow slaughter, and heifer slaughter in the first quarter were all lower year-over-year. Beef cow slaughter...

by Hannah Baker | May 2, 2025

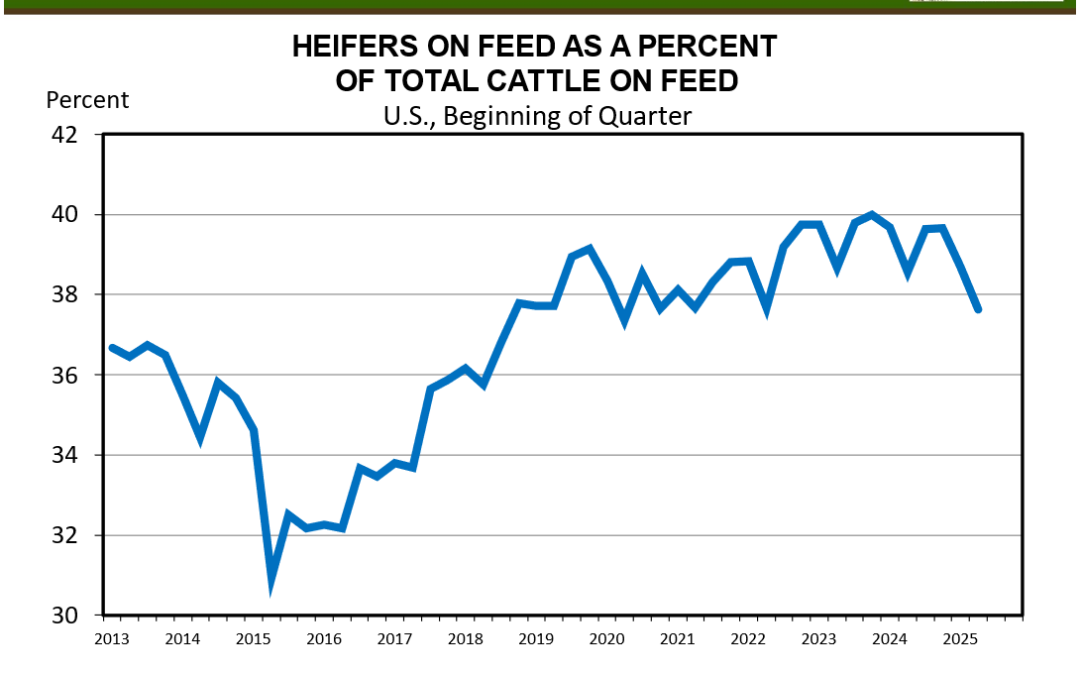

Heifers on Feed: Not as Many, but Still Too Many Every month, USDA-NASS releases the Cattle on Feed Report indicating how many cattle are on feed, how many have been placed, and how many have been marketed. The April report showed that cattle and calves on feed in...

by external | May 2, 2025

Kevin Athearn, UF/IFAS Regional Specialized Agribusiness Agent, North Florida Research and Education Center – Suwannee Valley Prices for stored peanuts remain relatively strong, but projected increases in peanut acreage this year dampen the outlook for the 2025...

by external | May 2, 2025

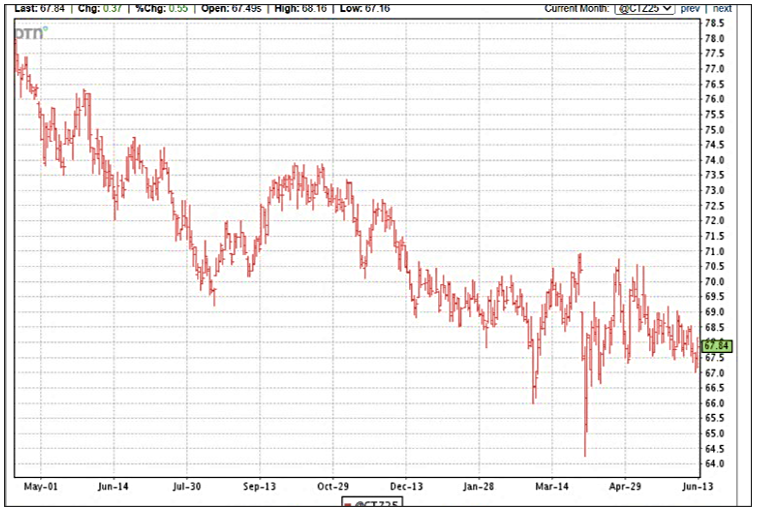

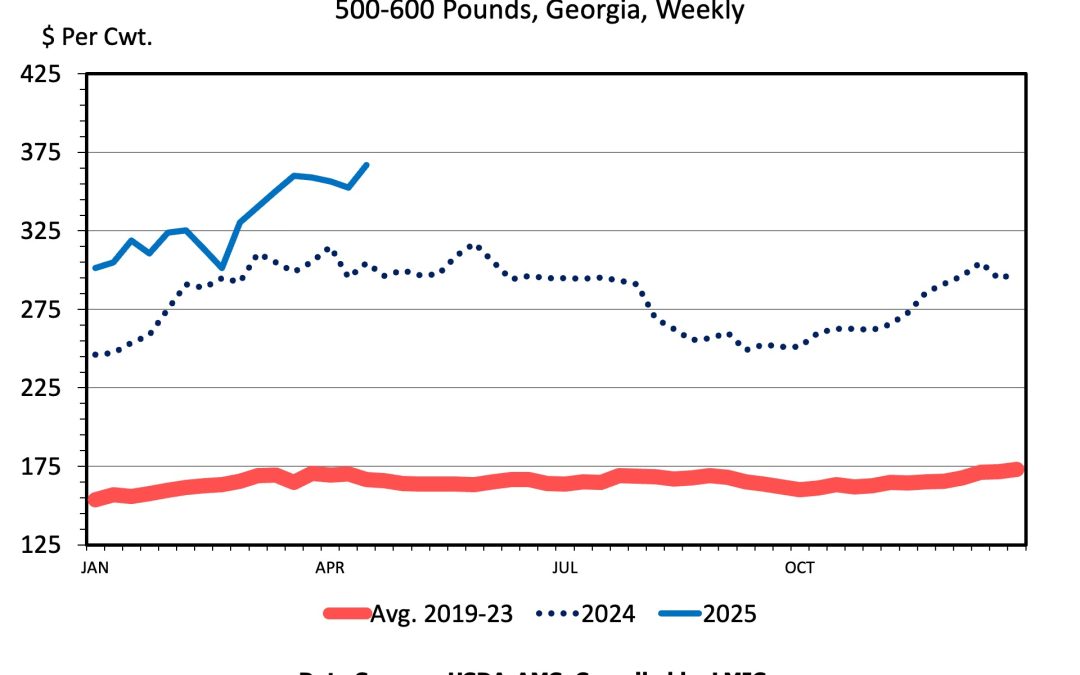

David Anderson, Texas A&M Livestock and Food Product Marketing Specialist, Southern Ag Today – April 29, 2025 The cattle market has experienced a lot of volatility in recent weeks, especially in the futures market, due to tariff announcements and recession...

by external | May 2, 2025

Don Shurley, UGA Emeritus Cotton Economist In USDA’s March 31 Prospective Plantings report, farmers said they intended to plant 9.87 million acres of cotton this year—down 12% from last year. Some industry observers expected as much as a 15% decline. I wonder now...