Don Shurley, UGA Professor Emeritus of Cotton Economics

USDA’s monthly crop production and supply and demand estimates for May, released today, show revisions for the 2021 crop and are also the first such estimates for the 2022 crop. We obviously have a long way to go but the drought situation in Texas and Oklahoma is not improving and portions of the Southeast are getting worse by the day. We need rain, bad.

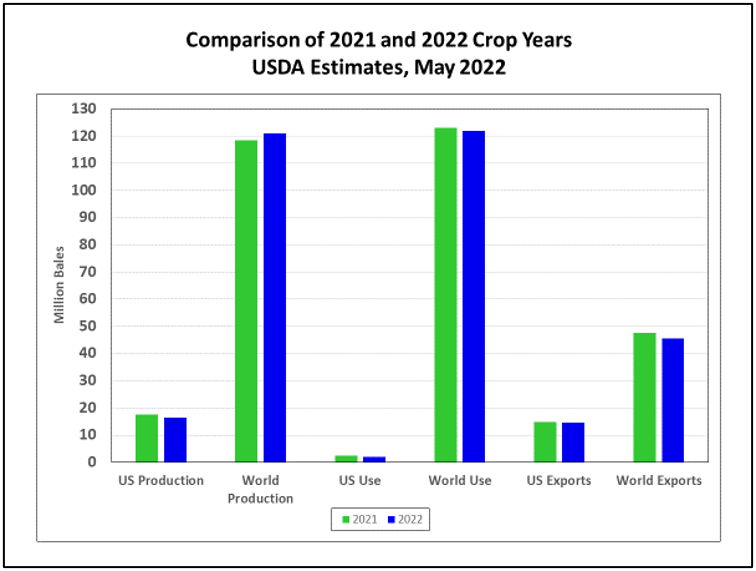

Here is a summary of today’s major US and World numbers:

US

- The 2021 US crop was reduced 100,000 bales.

- There were no changes in 2021 crop year US exports—still pegged at 14.75 million bales.

- So, ending stocks to carry in to the 2022 crop year on August 1 are reduced 100,000 bales.

- The first projection of the 2022 crop is 16.5 million bales- down approximately 1 million bales from last year.

- Exports for the 2022 crop year are projected at ¼ million bales less than this season.

- 2022 crop year ending stocks are projected to be down ½ million bales.

World

- The 2021 crop year World beginning stocks were raised by 720,000 bales (not good for price) but estimated production of the 2021 World crop was trimmed 1.75 million bales—a net reduction in available supply of just over 1 million bales.

- World use/demand for the 2021 crop year was reduced 1.13 million bales from the April estimate.

- 2022 World production projected up over 2 ½ million bales.

- World use/demand projected to continue to slip—almost 1 million bales lower than the just lowered 2021 crop year use.

–

–

I consider this a mixed outlook for the 2022 crop market. If price is to maintain its upward path, more focus will have to shift to the condition and size of the US crop. Because the demand outlook seems cautious.

US acres planted this year are estimated up 1 million acres and yield projected up 6%. But, due to drought conditions, acreage abandonment is projected at 25% compared to only 8.5% last season. Acres planted could be reduced.

US production concerns, coupled with reduced carry-in stocks, creates a tighter supply situation for 2022. This is supportive of prices but the demand/use situation appears to be weakening somewhat. Granted, the May numbers cut 2021 crop year use by only 1% and the forecast for the 2022 crop year is down less than another 1%. But taken in the context that this price buildup is largely based on demand, well, it’s a bit worrisome at least to me.

–

Growers should consider where the market is, how much of expected production you have priced, and the risk you are willing to take that prices could go even higher vs. move lower.

–