Don Shurley, UGA Professor Emeritus of Cotton Economics

Prices have rebounded from the low of 72 cents back on October 31. December futures are now back over 80 cents—prompting optimism that better times could be on the way.

=

The area around 90 cents is likely a level that will be tested and must be negotiated before prices can go higher. This most recent rally has already come close to that on several occasions. December is up and just over 88 cents today.

Opportunity to continue to improve depends, as we have said in this space many times, on demand, related US export sales and shipments, and the eventual size of the US crop.

This weeks USDA crop production and monthly supply and demand estimates raised the US crop and lowered Use. A summary of the main numbers includes:

- The US crop was raised 220,000 bales. Yield was lowered 3% in Texas but raised in 10 states.

– - Projected US exports for the 2022 crop year were unchanged from the October estimate.

– - World production was trimmed 1.62 million bales—most notably in Australia and Pakistan. No change in expected in the China crop.

– - World use/demand was trimmed 650,000 bales from the October estimate—accounted for most by reductions for Pakistan and Bangladesh. No change for China.

–

Barring any major weather event and despite some industry observations and opinion, the likelihood that the US crop will get smaller now seems greatly diminished. In fact, the crop could get a bit larger.

So, any further price improvement will increasingly depend on demand and factors or other signals related to economic stability and growth such as the value of the dollar, inflation rate, interest rates, US stock market performance, etc. Price will also depend on what is happening in foreign markets, as this will impact demand for US exports.

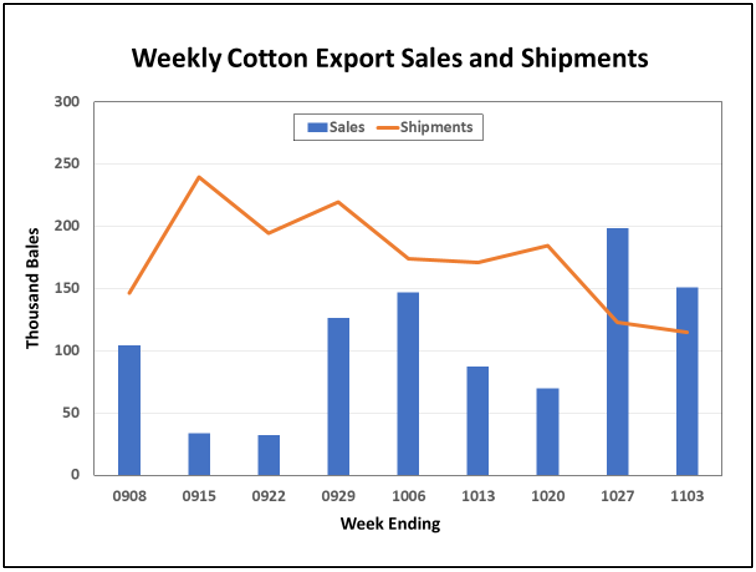

Shipments have trended down for most of the 2022 crop marketing year so far. Sales have improved but still at a relatively weak level. It’s early, but good weekly sales and shipments are one important barometer that will help guide and confirm price direction.

–

Any “good” or “happy about it” pricing opportunities for remaining uncommitted crop may be limited. Barring any major improvement in demand and economics, the upside to $0.95 or $1.00 seems limited—not impossible at all, but certainly not the path of least resistance right now. Further downside risk is possible, if the US crop gets bigger and/or demand signals do not improve.

–

- Cotton Marketing News:Acreage Numbers are a Surprise – What Now? - July 11, 2025

- Gulf Coast Cattlemen’s Conference – August 8 - July 11, 2025

- Cotton Marketing News:USDA June Numbers—Neutral, Not Good but Not Bad - June 20, 2025