Don Shurley, UGA Professor Emeritus of Cotton Economics

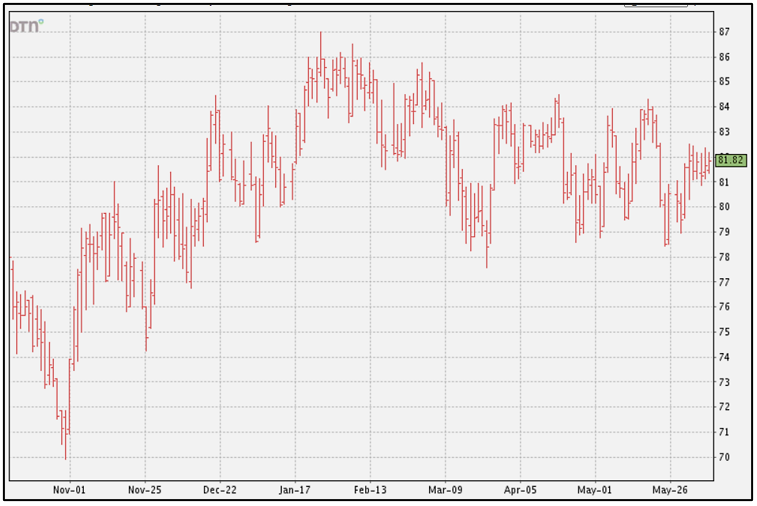

December futures have declined to the 79 cents area three times in the past several months, beginning back in March. It’s worrisome when this happens but each time prices have recovered.

Most recently this happened in late May just a couple of weeks ago, but prices found support and have now rallied back to the 81 to 82 cents area.

–

Having bottomed out there multiple times now, actually dating back to last January, there should be good support around 79. But likewise, prices have shown no willingness yet to move beyond the 84 cents area. This (79 to 84 cents) is not a price level that inspires most growers to do much in the way of marketing and price risk management decisions.

USDA reporting has just recently begun. The condition of the crop seemingly has improved. Areas of the southwest have gotten rainfall. For the week ending June 4, the US crop was 51% good to excellent—up slightly from the prior week. The Texas crop was 20% poor or very poor—down slightly from the prior week.

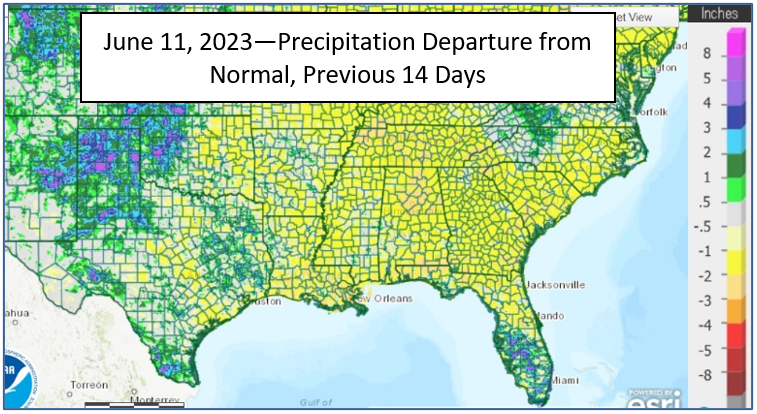

As of June 11, rainfall for the previous 14 days in some areas of Texas including West Texas was well above normal. Most of the rest of the cotton belt was below normal.

So, US crop uncertainty seems to be declining. US supply tensions may be easing. This may cause some weakness for the market but the first estimate of actual acres planted will be out at the end of the month and there’s uncertainty surrounding that.

–

If the US crop shows potential to get larger, that may not have a negative impact on price—as long as signals on the demand side continue to improve. USDA’s monthly supply/demand estimates for June showed:

- The 2023 US crop was increased 1 million bales due to improved conditions and less abandonment likely.

- But projected exports for the 2023 crop year were increased ½ million bales.

- World Use/Demand for the 2023 crop year was increased 770,000 bales.

- The 2023 China crop was reduced ½ million bales and China’s imports raised ½ million bales.

US exports for the 2022 crop marketing year that ends July 31, were raised from 12.6 to 13 million bales. Projected exports were raised 400,000 bales last month and now another 400,000 this month.

With a little over 8 reporting weeks left in the 2022 crop marketing year, exports need to average roughly 319,000 bales per week to meet USDA’s latest projection of 13 million bales.

The latest weekly export report, for the week ending June 1, sales were 497,000 bales—a marketing year high. Shipments were 338,500 bales. Shipments over the past month or more had been above the pace needed to meet USDA’s previous 12.6 million bale estimate—thus the reasoning to increase to 13 million bales this month.

The price outlook will depend on a balance between the condition and expected size of the US crop and whether or not demand continues to show improvement or slips on new negative factors.

–