Don Shurley, UGA Professor Emeritus of Cotton Economics

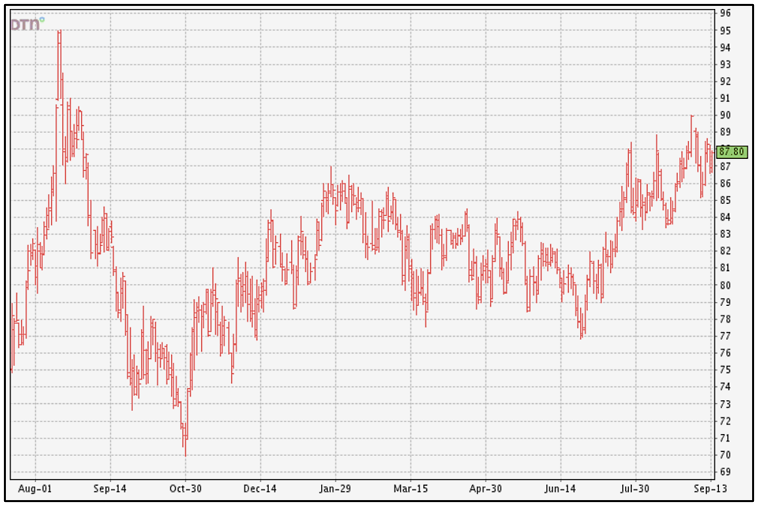

Since the low in the 77-78 cents area back in June, prices (December futures) have made three runs at the 89-90 cents area. Each time, prices retreated a bit—failing to sustain that level. I feel confident in saying that some growers took advantage of the near 90 cents and priced a portion of their expected production.

–

–

Why has the market not been able to push to 90¢ or higher and stay there? That’s a great question and I’m not 100% confident I know all the reasons why. But I think it may help to remember two rules of market behavior:

- Prices increase due to increased demand (buying) or lower supply

_ - Prices decline due to lower demand (buying) or increased supply (selling)

–

I’ve seen this if you read between the lines in some of the market news and media. Prices have increased due to the potential for a smaller crop and prices at a lower level stimulate buying. After an increase, prices weaken/decline due to producer selling at the higher level and reduced buying at the higher level.

You might be asking “Don, what the heck are you talking about?” Well, buyers seem to be confident at lower prices and producers not so much. So, buyers and speculators buy futures—demand increases. At higher prices, buyers may not be as confident about demand at that level. Some buyers and speculators will sell futures to profit off buying at lower prices. Producers will want to sell. Selling/supply increases. Right now, the market seems “comfortable” at 84 to 89¢.

This week’s (Sept 12th) monthly USDA production and supply and demand numbers provide reasons for prices to increase but also provide reasons to be cautious about it. In other words, I’m yet to see anything that can break the 84-89 tug-of-war. In summary:

- The projected US crop for 2023 was trimmed 860,000 bales or 6% from last month’s projection.

- The expected average yield was increased slightly but harvest acres were reduced 600,000 acres.

- Texas acres harvested were cut 340,000 acres but yield and production were increased. The Georgia crop was cut 250,000 bales, Oklahoma 260,000 bales, and North Carolina 110,000 bales.

- 2023 crop year carry-in stocks were raised approximately ½ million bales due to revisions made in 2021 and 2022 crop years.

- US exports projected for the 2023 crop marketing year were lowered 200,000 bales.

- World use/demand for the 2023 crop year was reduced 1.06 million bales—India down ½ million bales and Vietnam and Bangladesh combined down 400,000 bales.

- India exports were cut 200,000 bales and Brazil exports were raised just over ½ million bales.

So where does this leave us? The US crop has shrunk. World production is also reduced from last month’s projection and well below last year. Use/demand is reduced from last month’s projection but is still well above last year and 3 ½ million bales more than this year’s production.

There remains uncertainty about both the US crop and foreign crop. This month’s adjustments in the acreage numbers should now more solidify that number but there will remain uncertainty in harvest acreage and yield. I am told there are unknowns about the crops in India, China, and Australia.

This market has made runs at 90 cents. Growers want 90 cents or better. More runs at 90¢ are possible but the market has not been able to stay there. To stay there, the market will need to get over its jitters about the demand side. Right now, it’s the demand side that seems to be holding things back. Weekly export sales will be watched closely.

90¢ seems to be a reasonable marketing objective—at least for some portion of the crop. How much to price should provide enough protection from prices moving back lower but leave some to price if the market does finally move higher.

–