Don Shurley, UGA Professor Emeritus of Cotton Economics

Nothing is worse than to have land, money, and other resources already committed to production and watching the market (and the value of expected production) decline. Farming is a biological process and takes time and time creates risk. Resources must be committed months in advance of production and marketing.

New crop, December 2024 futures lost approximately 9 cents or 11% over a period of about 6 weeks, from early April to mid-May. That’s the difference between possibly a breakeven crop and a disastrous crop financially.

–

–

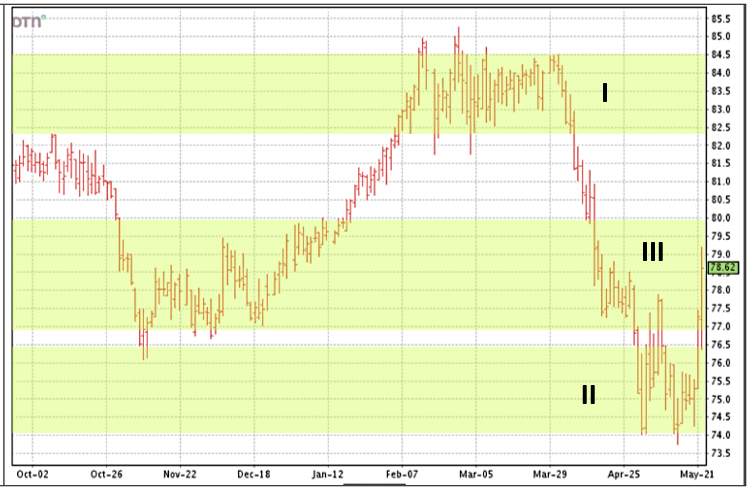

Since the most recent lows in the 74 to 75¢ area, price (December futures) has “improved” (if we dare call it that) and currently stands between 78 and 79¢—gaining 3.65¢ thus far this week. Has cotton’s downturn bottomed out? Right now, I see three “price regions” in this market:

I – Roughly 82.5 to 84.5¢. This is where we were and relatively happy before the bottom fell out. Looking and hoping for better.

II – 74 to 76.5¢. The “bottoms” of the past few weeks. We don’t want to return there.

II I- The “middle ground” of 77 to 80¢. Not where we want to be but better than where we were.

The decline we’ve witnessed in price, as I have read and try to decipher it, seems largely the result of speculative selling and profit-taking and somewhat also due to demand concerns. If this is true, to correct this, prices will eventually reach a level low enough that entices speculative buying and buying of the physical commodity.

The improvement we’ve seen in more recent days is said to be due to increased buying and exports, prospects for reduced China and Brazil production, and US weather and slow planting concerns. But this buying is generated by prices in the low 70’s, and that’s not healthy for the farmer. If we’re going to pull out of this “70’s problem”, buying (demand) must continue to improve and at even higher prices.

USDA’s monthly supply/demand estimates for May (released May 10th) were a mix of mostly not so encouraging news for cotton:

- This was the first estimate of the 2024 US crop. Production is projected at 16.0 million bales compared to 12.07 million bales last year.

– - US exports for the 2024 crop year are projected to be 13.0 million bales—up only 700,000 bales from the ’23 crop year.

– - US ending stocks are estimated to increase by 1.3 million bales.

– - World Use for the 2023 crop year was increased 540,000 bales.

– - Brazil exports for the 2023 crop year were increased and are projected to increase further for the 2024 crop year.

– - China Use/demand for the 2023 crop year was increased, and again for the upcoming 2024 crop year.

– - China’s cotton imports were increased for the 2023 crop year but reduced sharply for the upcoming 2024 crop year. This could reflect higher use of its own production and/or use of accumulated stocks.

–

The most recent export reports have been good. In the last 3 weekly reports, sales have averaged 217,000 bales and shipments have averaged 247,000 bales. China has been an active buyer.

Planting continues to be on par with average and just a little ahead of last year. But, Texas and Georgia are a little behind normal, as are Alabama, Louisiana, South Carolina, and Tennessee.

There are questions and uncertainty about planting.

- Will the decline in price over the past month or more, to the extent that they can, cause growers to change their plans on what to plant?

– - As states and areas approach their respective crop insurance coverage and planting deadlines, will planting get completed?

– - From personal observations, at least here in Georgia, we have had a lot or rain. It seems growers get 4-5 inches at a time. Fields are very wet, and it seems about the time things begin to dry out enough to get equipment in the field, it rains again. Some field areas are washed out. Will intended acres get planted? Will areas be replanted?

–