Don Shurley, Cotton Economist- Retired, University of Georgia, Part-Time Professor of Marketing and Policy, Abraham Baldwin Agricultural College-Tifton, GA

USDA’s September cotton crop production and supply/demand numbers were mostly “market neutral”. Here’s a summary of some of the major factors.

- The projected 2025 US crop was increased just slightly; up 10,000 bales from the August estimate. Revised based on updated FSA certified acres data and revised yield estimates.

- Projected US exports for the 2025 crop marketing year were unchanged at 12 million bales.

- World Beginning Stocks on hand August 1 were lowered approximately 1 million bales. This was due to revisions in the 2024 crop year—World use was raised 1.2 million bales.

- But, projected 2025 World production was raised just over 1 million bales—accounted for mostly by larger expected crops in Australia, India, and China. Production was lowered for Mexico and Turkey.

- Brazil production and exports were unchanged from the August estimates.

- World projected use/demand for the 2025 crop year was increased almost 1 million bales to now 118.83 million bales—which is good……. But, this is now lower than the revised 2024 Use number.

So, it appears now (thanks to the revision up for 2024) that 2025 World use/demand is presently headed in the wrong direction. I don’t know if this “numbers jockeying” make much if any difference to the market or not. But to me, it can’t be good to see lower demand for 2025.

–

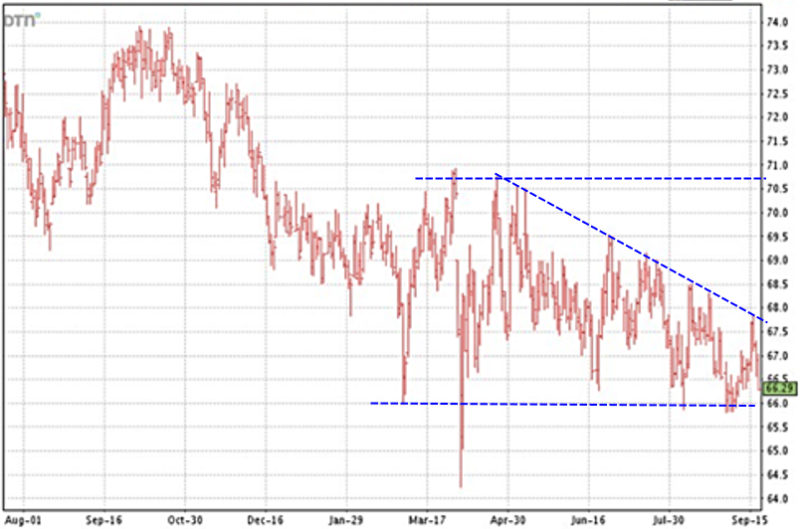

Prices (December futures) continue in the 66 to 70-71¢ range. Price has not responded to decreased U.S. acreage and production. Therefore, I can only surmise that:

- Crop condition may be compensating somewhat for reduced acres

– - The market is still uncertain about demand and the U.S. role in market share and exports. Markets do not like uncertainty and inconsistency. Apparently, improved prices (something with a 7 in the front) are not likely unless demand signals get stronger and/or the U.S. crop takes another cut (which we really don’t want).

–

But, overall crop condition is “ok” but really not doing all that well and appears to be and could be slipping. (NOTE: the latest report will be out on Monday, Sept 22). But, as of September 14, 14% of the crop was rated poor or very poor compared to 11% the prior week. Texas was 16% poor or very poor, Georgia 13%, and Tennessee 34%. At what point (in acreage and expected production and crop condition) would price care about the U.S. crop? Or does it?

It’s early but export sales so far for this 2025 crop marketing year total 4.2 million bales. This compares to 5.16 million bales last year at this time. Shipments thus far total 852,000 bales, compared to 951,000 bales last year. Shipments need to average approximately 242,000 bales per week to reach the current USDA projection of 12 million bales for the marketing year ending July 31. Thus far, and we’re just getting started, shipments have averaged approximately 138,500 bales per week.

I’m going to safely assume that a grower doesn’t want to sell now at these low prices and hopes (willing to take the risk) that price will eventually improve. But, what do you do if you want or need cashflow at harvest time but also want to postpone selling?

If this is you, I can think of 3 ways to do this:

- Store the crop in loan

– - Sell on a deferred price (on call) contract

– - Sell and buy a Call Option

–

None of these are perfect. So, you have to consider the pros and cons of each, including the risk you’re taking/not taking with each. Of course, none of this works if prices don’t improve, so you’d have to be willing to take that risk.

–

- Surprise!January WASDE Report Moves Corn and Soybeans Lower – Cotton Flat - January 16, 2026

- Don’t Ignore Cow Size When Comparing Calf Weaning Weights - January 9, 2026

- Federal Estate Tax and Gift Tax Limits Announced For 2026 - December 19, 2025