by Carrie Stevenson | Oct 21, 2020

Even healthy live oaks need maintenance and occasional trimming to stay safe. Photo credit: Carrie Stevenson, UF IFAS Extension

After storms, Extension agents are routinely asked about whose responsibility it is to maintain a tree along a property line. This becomes particularly important in a situation where a property owner’s tree or branch falls and causes damage to their neighbor’s home or possessions.

To clarify this often contentious issue, reference to legal experts is necessary. In a series of publications called “The Handbook of Florida Fence and Property Law,” two attorneys and a University of Florida law student explain several statutes that give us direction. The section on “Trees and Landowner Responsibility” goes into further detail and cites case-law, but for ease of reading it is summarized below.

Situation 1: Removing a healthy tree on a shared property line.

If two neighbors share a tree on their property line and one of them wants to remove it, the adjoining landowner must give their permission. Removing trees can impact property value, heating/cooling bills, or aesthetic value. Without a neighbor’s consent, the landowner cutting down a tree can be legally liable for damages.

Hurricanes can have serious impacts on trees in their path. Photo credit: Carrie Stevenson, UF IFAS Extension

Situation 2: Responsibility for overhanging branches and roots.

A big storm hits your neighborhood, with tons of rain, wind, and lightning. You wake up in the morning and see that a large branch fell from your neighbor’s tree and crushed your kids’ basketball goal. If branches from the neighbor’s tree were otherwise healthy, they are not responsible for any damages resulting from the tree. If it was dead, however, and their negligence contributed to the branch falling, they will be responsible for damages.

Keep in mind that if the neighbor’s tree/branches/roots are in good health but interfering with something in your yard, you may trim them at your own expense. The same goes for your tree hanging in their yard, so while it’s not required, it’s always good to have a conversation first to let them know your plans.

After Hurricane Ivan, this tree’s root system completely uprooted and destroyed and adjacent fence. Photo credit: Beth Bolles, UF IFAS Extension

Situation 3: Hurricane Sally blew your neighbor’s tree over and into your yard.

Just like the situation with branches and roots, the same principle goes for an entire tree falling on adjoining property—if the tree was alive, it’s the responsibility of the person whose yard it fell in. If it was dead when it fell, it’s the responsibility of the tree’s owner to pay for damages.

In a complicated situation involving property damage, the saying, “good fences make good neighbors” only goes so far. Be sure to note the health of your trees throughout the year and trim back dead or dying branches. If you see serious decay or have concerns about a tree’s health, contact your county Extension office or a certified arborist. Finally, if the circumstances aren’t easily determined, be sure to contact a licensed attorney and/or your insurance company for direction.

by Larry Williams | Jun 23, 2020

The 2020 Atlantic Hurricane Season got off to an early start with some tropical storm activity before the season’s official June 1 start date. We live in a high wind climate. Even our thunderstorms can produce fifty-plus mile per hour winds.

Storm damaged sweetgum tree. Photo credit: Larry Williams

Preventive tree maintenance is key to preparing for storms and high winds.

Falling trees and flying landscape debris during a storm can cause damage. Evaluate your landscape for potential tree hazards. Pruning or removing trees once a hurricane watch has been announced is risky and tree trimming debris left along the street is hazardous.

Now is a good time to remove dead or dying trees, prune decayed or dead branches and stake newly planted trees. Also inspect your trees for signs of disease or insect infestation that may further weaken them.

Professional help sometimes is your best option when dealing with larger jobs. Property damage could be reduced by having a professional arborist evaluate unhealthy, injured or questionable trees to assess risk and treat problems.

Hiring a certified arborist can be a worthwhile investment. To find a certified arborist in your area, contact the International Society of Arboriculture (ISA) at 888-472-8733 or at www.isa-arbor.com. You also may contact the Florida ISA Chapter at 941-342-0153 or at www.floridaisa.org.

Consider removing trees that have low wind resistance, are at the end of their life span or that have the potential to endanger lives or property.

Some tree species with the lowest wind resistance include pecan, tulip poplar, cherry laurel, Bradford pear, southern red oak, laurel oak, water oak, Chinese tallow, Chinese elm, southern red cedar, Leyland cypress, sand pine and spruce pine.

Broken pine from hurricane. Photo credit: Larry Williams

Pine species vary in their wind resistance, usually with longleaf and slash pines showing better survival rates than loblolly and sand pine. However, when pines become large, they may cause a lot of damage if located close to homes or other valuable structures. As a result, large pines are classified as having medium to poor wind-resistance. For this reason, it’s best to plant pines away from structures in more open areas.

Before and after a storm, tree removal requires considerable skill. A felled tree can cause damage to the home and/or property. Before having any tree work done, always make sure you are dealing with a tree service that is licensed, insured and experienced.

More information on tree storm damage prevention and treatment is available online at http://hort.ifas.ufl.edu/woody/stormy.shtml or from the UF/IFAS Extension Office in your County.

by Beth Bolles | Oct 29, 2018

As Hurricane Michael was barreling through the Panhandle region, wasp populations were at their highest of the year. Winds and flooding destroyed many of the nests of paper wasps, hornets, and yellow jackets and now wasps may be aggressive as they defend themselves or remnants of their nests. All are capable of multiple stings that are very painful. It is very likely that you will encounter stinging wasps as they scavenge for food and water, as well as seek shelter among debris and exposed trash.

Many people are stung by paper wasps after storms. They are not attracted to traps.

Here are a few pointers to help deal with stinging wasps.

- Try not to swat at wasps flying around or landing on you. You may be less likely to receive a sting if you can flick them off.

- Some wasps are attracted to the sap from broken or recently cut trees. Look before you reach. Wear gloves and other protective clothing when moving debris in case you disturb foraging or nesting activities.

- Wasps are also attracted to sugars and water. Try your best to keep food and drink cans covered. Completely close garbage containers or bags that contain food debris.

- Repellents are not effective against wasps. There are pesticides labeled to spray on smaller paper wasp nests if you find one in a spot close to people’s activity. These are usually aerosol pyrethroids or pyrethrins. Make sure you read the label carefully and use the product as directed.

- Do not use non labeled products like gasoline to manage wasps. This is not only illegal but can be dangerous to yourself and the environment.

- There are traps for yellowjackets that you may purchase or make. These only manage those wasps flying around, not any remaining in a ground nest.

Here is a Do It Yourself Yellowjacket trap from UF IFAS Extension.

- Cut the top 1/3 off your 2 liter bottle so that you have 2 pieces.

- Add a bait (fermenting fruit or beer) to the bottom of the plastic bottle.

- Invert the top portion of the bottle into the base, forming a funnel.

- Hang or place traps so they are about 4 to 5 feet above the ground. For safety, place them away from people.

A homemade trap to catch yellowjackets. Photo by Alison Zulyniak

by Larry Williams | Sep 3, 2015

Tropical storm season officially ends November 30. I’m not predicting a storm but even with our average winds during a typical thunderstorm, you’d be wise to prepare.

Falling trees and flying landscape debris during a storm can cause damage. Evaluate your landscape for potential tree hazards. Pruning or removing trees once a hurricane watch has been announced is risky and tree trimming debris left along the street is hazardous.

Photo credit: Larry Williams, UF/IFAS.

Now is a good time to remove dead or dying trees and to prune decayed or dead branches Also inspect trees for signs of disease or insect infestation that may further weaken them.

Professional help sometimes is your best option when dealing with larger jobs. Property damage could be reduced by having a professional arborist evaluate unhealthy, injured or questionable trees to assess risk and treat problems. Hiring a certified arborist can be a worthwhile investment. To find a certified arborist in your area contact the International Society of Arboriculture (ISA) at 217-355-9411 or at www.isa-arbor.com. You also may contact the Florida Chapter of ISA at 941-342-0153 or at www.floridaisa.org.

Consider removing trees that have low wind resistance, are at the end of their life span or that have potential to endanger lives or property. For example, laurel oaks are relatively short-lived, usually showing considerable dieback as they reach 50 years. They tend to lose their strength and stability faster than most other oaks and have low wind resistance. Consider removing a big, old laurel oak within falling distance of your home before the next storm.

Tree species with the lowest wind resistance include pecan, tulip poplar, cherry laurel, Bradford pear, southern red oak, laurel oak, water oak, Chinese tallow, Chinese elm, southern red cedar, Leyland cypress, sand pine and spruce pine.

Pine species vary in their wind resistance, usually with longleaf and slash pines showing better survival rates than loblolly and sand pine. However, when pines become large, they may cause damage if located close to homes or other valuable structures.

by Carrie Stevenson | Jun 23, 2014

Since the heavy flooding in late April of this year, many property owners have expressed concern to me and their local government officials about their neighborhood’s vulnerability to flooding. Homes and landscapes are most people’s largest investment, and the damage caused by a major storm can be financially and emotionally devastating.

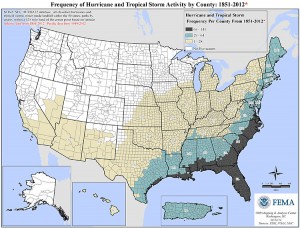

This map shows Florida’s extreme vulnerability to hurricanes and tropical storms, compared with the rest of the country. Graphics courtesy FEMA

To say that Florida is prone to flood is an understatement, at best. Between 1851 and 2012, every county in our state endured between 65 and 141 tropical storms and hurricanes. Many counties average one named storm every 1.1 years. While other states have coastal regions vulnerable to hurricanes, the entire state of Florida lies within FEMA’s highest designation of storm frequency. With hurricane season just beginning and record-breaking flood events in April, it is wise to consider flood insurance. Regular homeowners’ insurance policies do not cover damage related to flooding. Many homeowners go without flood insurance because their home is “high and dry” or “not in a flood zone.” It can be argued, however, that as a Floridian, particularly one in a region of the state with the highest annual average rainfall, you’re in a flood zone—it’s just a matter of whether you’re high or low risk. And, as we’ve seen recently, even those who thought they were low risk could be vulnerable.

Flood insurance is often very inexpensive for those outside of officially designated Special Flood Hazard Areas (think waterfront homes, low-lying property, creek floodplains, and barrier islands). Rates can be as low as $130/year for basic coverage in a low-risk area. It’s simple to get a ballpark figure for potential flood insurance costs by entering your address into a one-step “risk profile” online. According to the National Flood Insurance Program’s (NFIP) website, a quarter of NFIP flood insurance claims and third of Federal Disaster Assistance each year goes to residents outside a mapped high-risk flood zone . When the expenses related to flooding, including removal of flooring, walls, furniture, and damage to plumbing and wiring, are taken into consideration, flood insurance can be a smart investment.

Intense flooding can strike in unexpected locations during heavy rainstorms and tropical storms. This Pensacola street had never experienced serious flood damage prior to April 2014, so most residents did not have flood insurance. Photo credit: Carrie Stevenson

Timing is important, too, because a 30-day waiting period is often required before flood insurance coverage kicks in. If you are also looking at additional windstorm insurance, be aware that policies will not be sold if a storm is in the Gulf. It is important to act sooner than later, but if you start now you can have flood and windstorm coverage in place before August and September. Our most severe storms historically occur during these months, after the Gulf has had all summer to warm up.

To purchase flood insurance, contact your local agent, find an agent online at www.floodsmart.gov, or call 1-888-379-9531. Be sure to ask exactly what is covered and under what circumstances, as there are many particularities to flood insurance. For up-to-date information on recent changes to the NFIP, please visit Coastal Planning Specialist Thomas Ruppert’s webpage.

Disclosure: The University of Florida/IFAS Extension program cannot make specific recommendations on insurance agents or providers. Please make the best decision for your home and family to prepare for storms and flooding.